Chapter 2.2: Integrated strategic planning

Context

A long-term strategic plan—A must-do for an organization

- A 10-year strategic plan records the decisions the organization has made with respect to its strategy for the future.

- It sets forth the organization's mission, vision, values and objectives, and states how the organization will achieve them.

- It summarizes the environmental and resource assumptions underlying the strategic choices and identifies the risks associated with the choices.

- The strategic plan should contain the rationales, analyses and background information supporting those decisions.

- The strategic plan should help the organization to remain focused on long-term strategic priorities, in light of at times frequently changing shorter-term priorities.

Strategic planning describes how an organization intends to operate in order to fulfill its missionEndnote 1 and mandate, today, and into the future.

Planning strategically helps statistical organizations deliver on their core functions, which are to provide

- information that is relevant to the current, highest-priority information needs

- information that is of high quality

- information that is produced at the lowest possible cost.

The economy and society that statistical organizations aim to measure are changing at an unprecedented pace. Consequently, in order to remain relevant, the strategic planning process must make provisions for the development of new statistical programs and the decommissioning of others so that they are able to respond to the highest-priority information needs.

Before determining how to organize and implement a national statistical system or create a national statistical office (NSO), it is important to have a well-established strategy. In many countries, this takes the form of a national strategy for the development of statistics. Other countries have their own versions of a strategy. In Canada, the strategy is established on the basis of annual official reports to Parliament called Report on Plans and Priorities and the agency's Corporate Business Plan. These official documents provide information about Statistics Canada's strategic orientations and directions. In order for the agency to organize its operations in an efficient and consistent way, it has developed an Integrated Strategic Planning Process (ISPP).

The ISPP is a key mechanism used at Statistics Canada to maintain quality and relevance. In order for the agency's planning to be effective, the horizons of the planning process cover a ten-year time period and include all factors that influence success. The agency must ensure that, in a steady state, sufficient funds are available annually for the routine maintenance and periodic redesign of all corporate processes, systems, applications and infrastructure, as well as for the implementation of new classifications and standards and for survey redesigns. This ensures the continuity and quality—and, to some degree, the relevance—of the current statistical program.

The philosophy that underlies Statistics Canada's strategic planningEndnote 2 is one of fostering innovation and making sound investments. Innovation and investments lead to improved operations and systems—and, consequently, increased efficiency. Being and remaining efficient is the best way for the agency to ensure its financial viability and to proactively implement a strategic plan for maintaining the quality of existing statistical programs, improving existing programs, and creating new programs—that is, for ensuring continuity and relevance (see Chapter 3.1: Corporate Business Architecture).

Operating at the highest level of efficiency is critical to Statistics Canada's ability to carry out its statistical program and maintain the necessary level of innovation, and should be a permanent priority. For this reason, the Corporate Business Architecture (CBA) is at the heart of the ISPP. CBA investment proposals have the highest priority because they improve the efficiency of operations. This efficiency generates the funds to maintain the quality of programs, as outlined in the long-term strategic plan.Endnote 3 Once the quality of existing programs has been assured, new initiatives for innovating and for exploring strategic opportunities can also be funded.

Strategies and tools

This section provides an overview of the governance structure at Statistics Canada and of the agency's ISPP. It describes the key elements of the six-step process and the key success factors associated with each step, and illustrates how these are supported by the governance structure.

Strategic planning is integral to Statistics Canada's Corporate Management Framework (shown in Figure 2.2.1.). To produce relevant, high-quality and timely information, sound planning and priority-setting are essential. Integrated strategic planning allows the organization to achieve maximum efficiency, manage operational risks, and align programs with the evolving data needs of the country.

Figure 2.2.1: Statistics Canada's Corporate Management Framework

Description for Figure 2.2.1

This figure is a pyramid of the Corporate Management Framework.

At the top of the pyramid, there is the Outcome (Canadians have access to timely, relevant and quality statistical information on Canada's changing economy and society).

The three sides of the pyramid represent the human resources, the risk management and the governance.

Inside the pyramid, there are four layers (from top to bottom): relevance; then trust, splitting into quality, objectivity and confidentiality; then access and finally stewardship.

1. Governance

The leadership of Statistics Canada's overall governance and management system is provided by the Executive Management Board (EMB). The EMB is comprised of the Chief Statistician, who chairs the committee, as well as the Assistant Chief Statisticians (ACSs), who head the various functional areas of the agency. The EMB provides strategic direction for the organization and acts as the corporate decision-making body. Centralized decision making ensures that strategic planning investments are optimal for the corporation. This governance model is based on the objective that significant corporate issues be reviewed at the highest appropriate level; final decisions are rendered by the Chief Statistician, on the advice of the EMB.

The annual ISPP is governed by the Senior Management Review Board, composed of the EMB, the Chief Audit Executive, and all Directors General. Including all senior managers in strategic planning ensures that cross-cutting issues are considered when senior management makes final decisions about resource allocations.

As shown in Figure 2.2.2, a bottom-up process that follows the strategic direction allows investment proposals developed by divisional program managers to be reviewed for possible consideration by the Field Planning Board (FPB)—a senior management committee chaired by the ACS for each field or functional area of the organization.

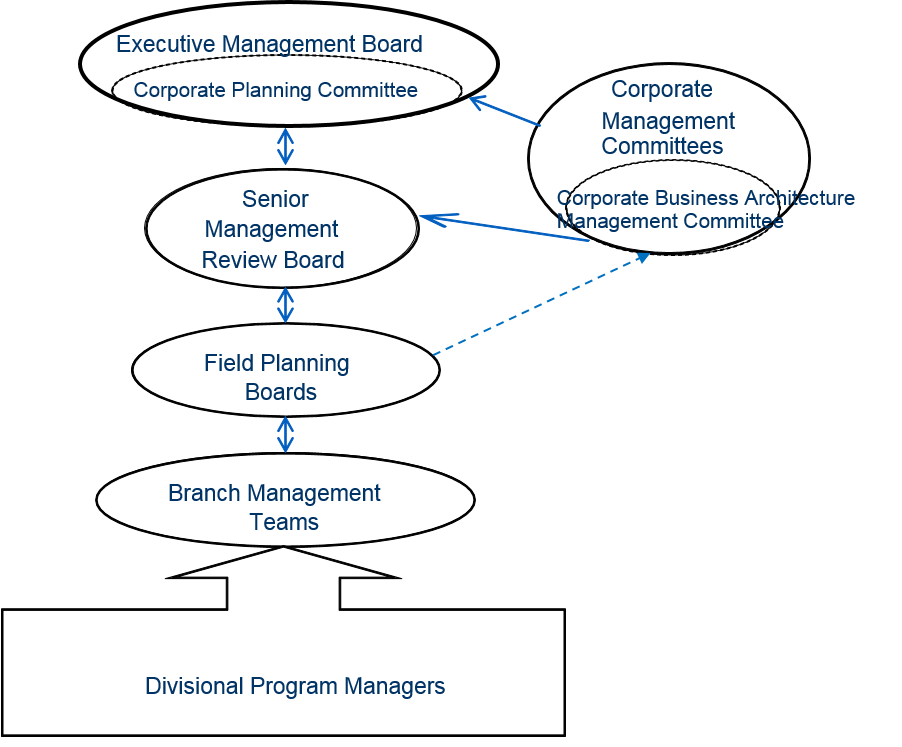

Figure 2.2.2: Governance of the Integrated Strategic Planning Process at Statistics Canada

Description for Figure 2.2.2

This figure represents the Governance of the Integrated Strategic Planning Process at Statistics Canada.

At the top, there is the Executive Management Board and the Corporate Planning Committee that is within it.

Under, you have the Senior Management Review Board.

In third, you have the Field Planning Boards.

In fourth, you have the Branch Management Teams.

Leading them, you have the Divisional Program Managers.

On the right of the figure, you have the Corporate Management Committees and the Corporate Business Architecture Management Committee that receives from the Field Planning Boards and report to the Senior Management Review Board, the Executive Management Board and the Corporate Planning Committee.

Where significant interdependencies exist, FPBs work together to ensure all key decision factors have been taken into consideration. Each FPB is also responsible for ensuring that business proposals are realistic in terms of deliverables, timelines and costs, and that service areas have reviewed costs for their services. Each FPB ensures that business proposals for its field are integrated and aligned with the corporate strategic priorities, and recommends proposals to the Senior Management Review Board.

Business proposals to improve the efficiency, robustness or responsiveness of the agency's business architecture are also vetted by the Corporate Business Architecture Management Committee. The proposals pertain to aspects of the business architecture, which includes the following:

- business processes

- enabling computer systems and hardware

- business rules

- organizational structure

The CBA places the emphasis on solutions that maximize the use of corporate tools and systems—an approach whose aim is to make the most of investments, reduce risks, and enable the agency to generate sufficient efficiencies to fund the punctual investments necessary for maintaining the quality of programs.

2. The six-step ISPP process

At Statistics Canada, the ISPP has been defined as an annual six-step process beginning with a review of the agency's strategic planning priorities and culminating with resource allocation for approved projects to begin in the new fiscal year. This is followed by regular monitoring and reporting of progress against plans.

Three key decision-making points in this process are identified with an asterisk (*) below: deciding which areas require strategic investment; deciding which specific investment ideas warrant a formal business case; and deciding which business cases will receive investment funding.

- Set the strategic planning direction.*

- Update the 10-year Continuity and Quality Maintenance Investment Plan (CQMIP), and prepare business proposals for the next fiscal year.*

- Develop business cases.

- Decide which business cases will receive investment funding.*

- Communicate plans and priorities.

- Monitor performance.

Through the ISPP, the agency integrates sound management practices, such as risk management, investment planning and project management, into the planning process. The ISPP includes an environmental scan, financial, human, and information technology resource management, as well as tools for project management and performance monitoring. The integration of financial, human resources (HR) and information technology (IT) planning into a unified process helps ensure that investment decisions are realistic and are able to support ongoing statistical program needs, the punctual investments required for continuity and quality maintenance, and the development of new programs and initiatives. As well, under the ISPP, managers are equipped with a standard set of tools for project planning, implementation and reportingEndnote 4 (see Chapter 2.4: Project Management Framework). This process establishes a heightened level of accountability both within Statistics Canada and in response to requirements from central government agencies. It includes feeding results into the official annual planning and reporting documents: Reports on Plans and Priorities and Departmental Performance Reports.

2.1 Step 1: Set the strategic planning direction

One year before the beginning of the fiscal year,Endnote 5 the EMB sets the strategic planning direction for the upcoming ISPP cycle. The EMB determines which areas require new initiatives, and requests proposals. This is the first key decision-making point.

Box 2.2.1: Step 1

Key Elements

- Review of corporate priorities with discussion organized around relevance, trust, access and stewardship

- Environmental scan— government, stakeholders

- Review of Corporate Risk Profile

Output

Strategic planning direction for the upcoming ISPP cycle, and strategic direction and priorities for the coming year as set by the Corporate Planning Committee.

The agency's strategic planning direction is informed by an environmental scan—including a review of external and internal drivers, and an integrated risk management exercise. The external environmental analysis involves conducting political, economic, technological, and social demographics analysis and documenting the needs of stakeholders. See details in Box 2.2.1.

The agency's corporate priorities are relatively stable over time. As the NSO for Canada, Statistics Canada is legislated by the Statistics Act to produce statistics that help Canadians better understand their country—its population, resources, economy, society and culture, and to serve this function for the whole of Canada.

Some corporate priorities (such as conducting the Census and the Labour Force Survey) are legislative obligations in Canada. Other priorities evolve over time to meet current information needs. At the annual Strategic Planning Direction Setting Session in April, corporate priorities are revisited on the basis of an environmental scan and an analysis of the Corporate Risk Profile, for the purpose of ensuring relevance to public policy development and maintaining the agency's ability to meet the highest information needs of Canadians and Canadian institutions.

Although risk is actively managed throughout the year via the priorities being addressed by managers and corporate management committees, a coordinated effort to update the Risk Register is completed annually. This allows the organization to identify where strategic investment is required in order to mitigate risks to an acceptable level. Risks are categorized according to the four elements at the heart of the Corporate Management Framework: relevance, trust, access and stewardship. The result is an updated Corporate Risk Profile that focuses the ISPP discussions around mitigating important corporate risks.

In its capacity as an agency of the federal government, Statistics Canada regularly monitors the information needs and the priorities of federal departments. An extensive stakeholder network and participation in various national and international organizations help the agency keep informed of emerging issues and remain at the forefront of innovation in statistical measurement (see Chapter 1.4: Understanding User's Needs and Maintaining Relationships).Engagement with stakeholders involves managers at all levels and provides information on evolving user needs, program weaknesses and information gaps. Combined with the results of client feedback surveys, internal program evaluations, and ad hoc external program reviews and audits, this input reflects the priority needs of Canadians and of their governing institutions, as well as those of businesses and other groups.

2.2 Step 2: Update the 10-year Continuity and Quality Maintenance Investment Plan, and prepare business proposals for the next fiscal year

From May to June, managers update their ten-year CQMIP and develop high-level investment business proposals, paying particular attention to proposals that would begin in the next fiscal year. Those proposals are reviewed and recommended by FPBs. See details in Box 2.2.2.

In June, the third month of the fiscal year, at the Strategic Planning Conference, the Senior Management Review Board decides which business proposals are supported for further consideration. This is the second key decision-making point.

Box 2.2.2: Step 2

Key Elements

- Review of corporate priorities with discussion organized around relevance, trust, access and stewardship

- Environmental scan— government, stakeholders

- Review of Corporate Risk Profile

Output

Strategic planning direction for the upcoming ISPP cycle, and strategic direction and priorities for the coming year as set by the Corporate Planning Committee.

A key element in the ISPP process is having a reasonable forecast of all investments required to preserve the quality of information programs and ensure the continuity of operations over time. To this end, the CQMIP is an essential tool. This step includes projects that require punctual investment to produce and maintain quality and, to some degree, relevance.

Much of the agency's work is cyclical in nature. Many of the investments necessary to ensure continuity and quality of programs are known in advance over a long planning horizon. For example, the Labour Force Survey redesign occurs approximately every ten years. Such instances of known investments constitute the CQMIP.

The ISPP is the mechanism by which program areas request additional funding from the agency to carry out new or cyclical projects that could not be covered by their regular base funding. Specifically, the CQMIP covers a ten-year planning horizon and identifies to the agency what draws will be made on the corporate financial availabilities.

The CQMIP is an effective tool to manage the timing of all strategic investments so that significant expenditures are planned well in advance, while total investment is relatively stable from year to year. This allows the agency to project long-term financial, IT and HR needs against planned financial availabilities. The ever greening of the CQMIP also represents a streamlining of the planning process. The strategic investments of the organization are understood long in advance and require only annual adjustments at the margin for new or emerging needs.

Ongoing program funding is treated separately from the punctual investment "project" funding required to maintain quality, ensure relevance, or generate efficiencies. However, both are integrated into a single ten-year view of the organization's overall financial picture.

At this step in the planning process, all projects included in the CQMIP are at Stage 1 of the Departmental Project Management Framework (DPMF): idea generation. The idea or proposed initiative that addresses a business problem or opportunity is identified at this stage. This first attempt at describing the problem, need or opportunity, and at roughly estimating the project's scope, duration and cost, is carried out at the highest appropriate level. This step provides the necessary information to determine the priority of the project in the context of the agency's strategic direction.

2.3 Step 3: Develop business cases

From July to October, business cases and detailed cost estimates are developed for the investment proposals for the next fiscal year that were supported for further consideration at the Strategic Planning Conference. See details in Box 2.2.3.

Box 2.2.3: Step 3

Key Elements

- Review of corporate priorities with discussion organized around relevance, trust, access and stewardship

- Environmental scan— government, stakeholders

- Review of Corporate Risk Profile

Output

Strategic planning direction for the upcoming ISPP cycle, and strategic direction and priorities for the coming year as set by the Corporate Planning Committee.

The development of business cases that integrate all the necessary information for planning decisions is essential to the success of this stage of the ISPP. At this step in the planning process, all projects that will start in the next fiscal year must produce a business case. This consists of a description of the project, the project's contribution to corporate objectives, an options analysis, cost estimates and resource requirements, a risk assessment including mitigation strategies, clearly documented planning assumptions, and business benefits / outcomes. The business case includes all information necessary to describe the rationale for undertaking the project.

The FPB performs a challenge function to ensure that the costs and benefits of projects and the relationship of business cases to corporate and program priorities are fully examined. This also includes an assessment of interdependencies between projects and across fields with respect to project deliverables and human and IT resource allocation. It is essential that all service areas be consulted at this stage of the process and that required approvals be obtained for planned activities.

First priority is given to the CBA projects. These investment proposals have the highest priority because they improve the efficiency of operations. This generates the corporate financial availabilities to maintain programs, as outlined in the CQMIP. Once the quality of existing programs has been assured, new initiatives to innovate and to explore strategic opportunities can also be funded. Thus, investment proposals are grouped into three broad categories to reflect different aspects of strategic planning: finding new and better ways to do business, maintaining the quality of existing programs, and enhancing and developing new programs.

The key tool used to ensure rigour of project assessments is the Departmental Project Management Framework (DPMF) (see Chapter 2.4: Project Management Framework). The process for developing new programs and for conducting substantial redesigns of existing programs must ensure that the project management of these initiatives is separated from responsibility for ongoing programs, that projects are properly resourced and funded, and that program design conforms to the approved business and systems architecture.

The goal is to collect information once at the beginning of the planning process and re-use it for many purposes. The DPMF templates gather information about funding sources, HR and IT needs, risks, etc., in a standardized manner. Information reported at the beginning of the planning cycle is used to manage projects and monitor performance.

2.4 Step 4: Decide which business cases will receive investment funding

In November, the Senior Management Review Board determines which investments will be funded, as well as how the human resource and IT strategy will be implemented to ensure that necessary resources are available for delivery of the investment projects. This is the third key decision-making point.

This step begins with a high-level update on the strategic planning direction, including a final integrated analysis of financial, HR and IT availabilities. This incorporates all investment business cases and the impact if all investments were approved, as well as an analysis of options and recommendations. See details in Box 2.2.4.

Box 2.2.4: Step 4

Key Elements

- Final integrated analysis of financial, HR and IT availabilities

- Presentations of business cases

- Peer review and challenge function

- Prioritization versus available resources

Output

Final integrated strategic planning decisions.

The detailed analysis of HR and IT availabilities is only as robust as the underlying business cases (created during the previous step of the ISPP). These must be completed prior the Senior Management Review Conference and must consider the overall resource demand relative to supply at the agency level. This explicitly takes into account ongoing program requirements as well as new investment proposals.

Business cases are presented to the Senior Management Review Committee, chaired by the Chief Statistician, for peer review and challenge. This ensures that the overall context and the impacts on the agency are taken into consideration. It also includes an examination of the relative contribution to strategic objectives and the prioritization of investments in light of available resources.

The Senior Management Review Committee then makes decisions about the approval or rejection of all business cases, including investments included in the CQMIP. The integrated analysis of financial, HR and IT availabilities over a ten-year horizon ensures that the approval of projects, many of which constitute multi-year investments, are made in context of future operational requirements.

2.5 Step 5: Communicate plans and priorities

In the three months before the beginning of the new fiscal year (December to March), managers finalize and initiate project plans, while budgets are allocated by the beginning of the upcoming fiscal year. Plans and priorities are communicated both externally, in annual reports required by Parliament, and internally, to the agency's employees and managers. See details in Box 2.2.5.

Box 2.2.5: Step 5

Key Elements

- Project charter and high-level business requirements

- Report on Plans and Priorities

- Corporate Business Plan

- Chief Statistician's Annual Address

- Budget allocations

Output

Plans and resource allocation for upcoming year finalized.

Record keeping and strong information management practices related to ownership, version control and transmission are an important part of the ISPP with respect to ensuring sound data stewardship, data integrity, and clear communication of the strategic plan. An ISPP Record of Decision records the approved / refused status of investments, along with the funding strategy for each. Taken together with the ongoing base-funded program of activities, this provides the basis for the development of the Report on Plans and Priorities and the Corporate Business Plan, including an official HR strategy and an official IT resource allocation plan to ensure the capacity to deliver on the agency's operations. As well, divisional and program budgets are adjusted to reflect investment decisions.

In January of each year, the budgeting exercise for the upcoming fiscal year begins. Approved investment budgets are allocated to the responsible financial responsibility centres and the appropriate program elements to reflect the agency's matrix management structure (see Chapter 2.1: Organizational Structure and Matrix Management). Full budgets are allocated by April 1 of each year. At this step in the planning process, new investment projects are initiated in Stage 3 of the DPMF. This includes the identification of high-level business requirements and the creation of the project charter to ensure that all stakeholders are ready to commit to implementing the project as outlined.

The Report on Plans and Priorities (RPP), which provides information on the agency's plans and expected performance, is the official external planning report. It is tabled in the Parliament of Canada along with the Main Estimates (see Chapter 2.3: Financial Management) in March each year. The RPP is a compilation and explanation of the annual business plan; it incorporates lessons learned from the previous years' experience. Important elements from the ISPP are reported in the RPP.

The key internal communication mechanisms are the Corporate Business Plan and the Chief Statistician's Annual Address. The Corporate Business Plan outlines how the organization conducts its business, the challenges it faces, and the approaches it has adopted to manage these challenges over the next three years. It is updated annually, and includes the HR and IT strategic plans, thereby ensuring coherence. It links the mandate and mission with program priorities and key strategic investments. This document ensures that all stakeholders and participants involved in the delivery of the agency's priorities are knowledgeable about the agency's priorities for the upcoming fiscal year and have all the necessary resources to deliver on these. It is also critical that all program funding and changes approved as part of the ISPP be known and understood by all concerned staff to promote buy-in and commitment.

In March of each year, the Chief Statistician presents the agency's Annual Address in a live webcast accessible to all Statistics Canada employees. The Annual Address communicates the priorities and challenges that will be the agency's focus in the coming year. To ensure that employees unable to attend or to view the simulcast presentation have access to this information, a special issue of the agency's internal newsletter, @StatCan, is published and made available electronically on the Internal Communications Network. The @StatCan Special Issue provides a unique magazine-style presentation of the information contained in the Chief Statistician's annual address to all employees.

2.6 Step 6: Ongoing: Monitor Performance

The final step in the ISPP, monitoring performance, is an ongoing activity; it includes both corporate reporting requirements and performance monitoring. Projects are also audited selectively for performance against deliverables and compliance with corporate policies, standards and procedures (see Chapter 2.8: Program Evaluation and Chapter 2.9: Internal Audit).

Many of the reports described below become inputs to the next year's planning cycle. This step in the process coincides with stages 4, 5 and 6 of the Departmental Project Management Framework—Project Planning, Execution and Close-Out. At this step, one must decide how the project will be structured and executed. This includes establishing the baselines of scope, schedule and cost; and, subsequently, executing, completing, tracking and measuring the project activities over the life of the project as defined at the planning stage. The project's final close-out report summarizes accomplishments, and measures the project against criteria set out in the charter to determine its success. See details in Box 2.2.6.

Internal reporting

Monthly financial reports are prepared and presented to managers, who use them to forecast the year-end position of their divisions, to assess the financial risks to their programs, and to review changes in operations and personnel. They are signed as an attestation of completeness and accuracy. Monthly financial reports also provide timely information to the Chief Statistician in his role as Accounting Officer. This information is aggregated at the field level and supports the production of a monthly report reviewed by the Chief Financial Officer (CFO). Corporate Finance consolidates the financial information, and highlights any changes from the previous month. All changes to the financial profile of programs and projects must be approved by the EMB.

Box 2.2.6: Step 6

Key Elements

- Executive dashboards

- Performance management agreements

- Corporate management committees

- Financial reporting

- Departmental Performance Report

- Departmental Staffing Accountability Report

- Performance measurement strategies and evaluation reports

Output

Completed planning cycle

Financial reporting is also a key element of the Executive Project Dashboard, which is the mandatory format for project status reporting as per the DPMF. Through its use, governance committees will be kept informed on the triple constraints of scope, schedule and cost, as well as provided with the status of changes, issues and risks related to strategic investment projects on a monthly basis. Selected larger projects are subject to Internal Audit and Evaluation upon completion to determine whether the planned outcomes were fully delivered and to assess compliance with corporate policies, directives, procedures and standards. All programs are also subject to formal evaluations on a cyclical basis.

Strategic priorities are also reflected in the performance agreements of executives and employees. Senior executives ensure that strategic priorities are reflected in their commitments and performance measures. These commitments are then cascaded down into the objectives of managers and employees. They form the basis for measuring the results achieved ((see Chapter 2.5: Planning and Management of Human Resources).

Strategic priorities also drive the work of Corporate Management Committees. These committees are responsible for managing risks related to one of the four corporate priorities (i.e., relevance, trust, access and stewardship). Each committee meets at least monthly to discusses the corporate strategic priorities and sets out plans that will address the corporate risks. Committee work plans are approved and monitored by the EMB.

External reporting

The Departmental Performance Report (DPR) is the official external performance report to the Parliament of Canada. The DPR provides an account of results achieved against planned performance expectations set out in the RPP and is submitted to the Minister responsible for Statistics Canada, generally in September. Statistics Canada's DPR, along with those of other federal departments, is tabled in Parliament in the fall by the President of the Treasury BoardEndnote 6 , on behalf of the ministers who preside over agencies and departments.

As well, a rigorous external financial forecasting and reporting process is in place. It provides for monthly updates to the CFO and the EMB on the agency's financial situation, including quarterly progress reports on significant projects and ISPP-approved investments. Quarterly Financial Reports are published externally on Statistics Canada's website in accordance with Treasury Board policy.

At the end of each fiscal year, the organization prepares the Public Accounts Plates, which present the financial operations of the organization and its use of the Main Estimates provided to the organization. The Public Accounts Plates are used for consolidation into government-wide financial statements, which are audited by the Auditor General of Canada and tabled annually in the Parliament of Canada.

Other external performance reporting mechanisms include the Departmental Staffing Accountability Report, required under the Public Service Employment Act to ensure that the public service organizations meet accountability requirements and expectations with respect to hiring and is tabled with the Public Service Commission in February.

Conclusion

Integrated strategic planning is a key mechanism used to maintain quality and relevance in a statistical organization. Both relevance and quality tend to deteriorate over time in the absence of proactive intervention. The 10-year strategic plan records the decisions about how the organization will fulfill its mission and mandate into the future. The 10-year strategic plan should help the organization to remain focused on long-term strategic priorities, in light of at times frequently changing shorter-term priorities.

The key success factor is a corporate culture that fosters innovation and reinforces awareness of emerging issues and buy-in among managers and staff. Specific elements of this type of corporate culture include the following:

- Appropriate infrastructure and governance mechanisms are in place for effective planning

- Direction-setting by senior management based on an environmental scan of priorities and emerging issues

- An up-to-date long-term plan for continuity and quality maintenance

- Comprehensive business-case assessments

- Integrated analysis of financial, human-resource and IT availabilities over at least a three-year horizon

- Coherence of communications

- Measurement of performance against plans.

The agency must ensure that, in a steady state, sufficient funds are available annually for routine maintenance and periodic redesign of all corporate processes, systems, applications and infrastructure, as well as for implementation of new classifications and standards and survey redesigns. Through the ISPP, the agency integrates sound management practices, such as risk management, investment planning, project management, and evaluation into the planning process. Integrated strategic planning allows Statistics Canada to achieve maximum efficiency, manage operational risks, and align programs with the evolving data needs of Canadians.

Endnotes:

- Endnote 1

-

Statistics Canada's mission is "Serving Canada with high-quality statistical information that matters." Under the Statistics Act, Statistics Canada's mandate is to collect, compile, analyze, abstract and publish statistical information relating to the commercial, industrial, financial, social, economic and general activities and condition of the people of Canada.

- Endnote 2

-

The base budget of Statistics Canada is fixed; it is allocated on an annual basis by Parliament. See the chapter on financial management.

- Endnote 3

-

At Statistics Canada, the long-term strategic plan is called the Continuity and Quality Maintenance Investment Plan (CQMIP).

- Endnote 4

-

At Statistics Canada, this is called the Departmental Project Management Framework (DPMF).

- Endnote 5

-

Each fiscal year begins on April 1 and ends on March 31. Therefore, Step 1 begins one year before the beginning of the next fiscal year.

- Endnote 6

-

The Treasury Board is responsible for accountability and ethics, financial, personnel and administrative management, comptrollership, approving regulations and most Orders-in-Council.

Bibliography

Government of Canada (2005). Statistics Act. L.R.C 1985, c. S-19. Amended by 1988, c. 65, s. 146; 1990, c. 45, s. 54; 1992, c. 1, ss. 130, 131; 2005, c. 31; 2005, c. 38. Consulted on 11th of March 2016 and retrieved from http://laws-lois.justice.gc.ca/eng/acts/S-19/FullText.html

Government of Canada (2016). Office of the Auditor General of Canada. Consulted on the 31st of March 2016 and retrieved from http://www.oag-bvg.gc.ca/internet/English/admin_e_41.html

Government of Canada (2003). Public Service Employment Act. (S.C. 2003, c. 22, ss. 12, 13). Consulted on the 31st of March 2016 and retrieved from http://laws-lois.justice.gc.ca/eng/acts/P-33.01/index.html

Government of Canada (2016). Public Service Commission of Canada. Consulted on the 31st of March, 2016 and retrieved from http://jobs-emplois.gc.ca/index-eng.htm

Statistics Canada (2015). Report on Plans and Priorities 2015-2016. Consulted on the 31st of March 2016 and retrieved from http://www.statcan.gc.ca/eng/about/rpp/2015-2016/index

Statistics Canada (2016). Departmental Performance Report 2014-2015. Consulted on the 31st of March 2016 and retrieved from http://www.statcan.gc.ca/eng/about/dpr/2014-2015/index

Statistics Canada (2016). Corporate Business Plan - Statistics Canada 2015-16 to 2017-18. Consulted on the 31st of March and retrieved from http://www.statcan.gc.ca/eng/about/bp

- Date modified: