Chapter 2.3: Financial management

Context

Sound financial management contributes to the effective and efficient use of public resources and ensures that government organizations, including national statistical agencies, are accountable for the prudent stewardship of public funds and the safeguarding of public assets.

Effective financial management is usually grounded in a code of values and ethics that guides public servants in everything they do while carrying out their professional duties. In the Canadian context, these values include the following: respect for democracy, respect for people, integrity, stewardship and excellence.

In Canada, the Financial Administration Act (FAA) provides the cornerstone of the legal framework for financial management within the federal government. The FAA gives the Treasury Board SecretariatEndnote 1 the authority over financial management matters and other matters relating to the prudent and effective use of public resources. This is done by approving financial management policies, allocating financial resources, and overseeing departmental performance.

The Government of Canada defines four fundamental principles of financial management: value for money, accountability, transparency and risk management. Value for money means that public fundsEndnote 2 are managed with prudence and probity, assets are safeguarded and resources are used effectively, efficiently and economically to achieve departmental and governmental objectives. Accountability requires that there be clear responsibilities for financial management that provide assurance to the government and citizens regarding the effective use of public funds and the results achieved. Transparency means that the public and the government are provided with pertinent, reliable and timely financial and related non-financial information and reports so that they can be well-informed of the use and management of public funds. Proper risk management requires effective and efficient systems of internal control, where controls are proportionate to the risks they aim to mitigate yet support innovation and results for citizens. The Government of Canada has published several policy instruments regarding financial management to ensure consistency and effective financial management across the public sector.

Public sector managers always have three budgets in play, reflecting the cyclical nature of financial management: current, future and past. They must manage the budget and deliverables for the current fiscal year while making plans for the future and accounting for how monies were spent in the previous year.

Strategies and tools

All managers are, to some degree, financial managers. However, it is essential to have clear roles and responsibilities for financial management of the current, future and past budget allocations within the statistical agency.

This section describes the governance structure and the financial cycle that underlie strategic and efficient financial management.

1. Governance

In Statistics Canada, financial responsibilities reside with the senior management of the organization—the Chief Statistician, the Chief Financial Officer, executive managers, and senior audit and evaluation executives.

Deputy Head (Chief Statistician)

As accounting officers, deputy heads are accountable to the government (Parliament) for their management responsibilities, including their financial management responsibilities. This includes accountability for allocating resources to deliver departmental programs in compliance with government laws (and the regulations, policies and procedures derived from them), for maintaining effective systems of internal controls, for signing accounts in a manner that accurately reflects the financial position of the department, and for exercising any other duties prescribed by law or regulations relating to the administration of their department or agency. In practice, accounting officers are also held responsible for the parliamentary appropriations received.

Chief Financial Officer (CFO) and other senior executives of the Finance Branch

The Chief Financial Officer (CFO) and the other senior executives of the Finance Branch directly support the deputy head, as the lead departmental executive for financial management, providing key objective strategic advice on the overall stewardship of the financial management culture and on the agency's financial performance. The CFO is accountable to the Office of the Comptroller GeneralEndnote 3 as the most senior financial manager within the department or agency. The CFO must adhere to explicit requirements throughout the financial management function.

All executive-level managers (Directors, Directors General and Assistant Deputy Heads) of program and service areas

Executive-level managers of program and service areas are responsible for ensuring effective financial management of all the activities falling within their areas of responsibility (including financial resources), and have final control with respect to organizing and staffing their own units. An instrument of financial delegation is used to define the various authorities that managers at various levels can exercise. In Canada, the Delegation of Financial Signing Authorities ensures that appropriate financial and management controls are applied to the decision-making process in spending public money and that they contribute to the effectiveness of program delivery and to the accountability of the authority process. The Delegation of Financial Signing Authorities is legally enforceable under the Financial Administration Act.

Senior audit and evaluation executives

Senior audit and evaluation executives provide objective assurance services for all areas of departmental responsibility (see Chapter 2.8: Program evaluation and Chapter 2.9: Internal audit). In addition, Statistics Canada established a Departmental Audit Committee (DAC) in 2009, in response to the federal government's new Policy on Internal Audit. The DAC is an essential component of the governance structure, and a critical aspect of a strong and credible internal audit regime. The DAC, whose membership includes three independent members who are currently outside the federal public service, ensures that the Chief Statistician has independent, objective advice, guidance and assurance on the adequacy of the agency's risk management, control and governance processes. The DAC does this by actively overseeing the internal audit program to ensure it properly and regularly assesses Statistics Canada's key control and accountability measures in an integrated and systematic way.

2. Cyclical nature of financial management

Public sector managers are involved with three budgets that are constantly in play: current, future and past.

2.1 Current budget

The current budget allocation is established before the fiscal year begins, along with the expected program deliverables. A manager's first concern is to spend and manage these funds according to the rules, for their intended purpose, and in keeping with objectives.

Statistics Canada is organized by subject matter and service areas and by centralized centres of expertise in order to optimize resource utilization. Centres of expertise include IT systems development, data collection and processing, and methodology (see Chapter 2.1: Organizational Structure and Matrix Management). The various areas work together on specific deliverables within the agency's matrix-management framework. Under this approach, resources and related budgets are allocated and controlled on two axes: a functional axis and a program axis. Matrix management requires that a strong analytical accounting capability be in place to support budgeting decisions and monitoring of outcomes.

Also, each expenditure is coded to correspond with specific characteristics or line objects that allow monitoring of expenditures and comparison with commitments (shows variances between what was initially planned and what was actually spent).

As indicated in Figure 2.3.1, all costs for any given program / project are recorded at the FRC level but are also ascribed to the program/project in our matrix cost accounting system. The matrix cost accounting system is illustrated by a chart showing the three programs that make up the operating budget of the Income Statistics Division: Pension Plans in Canada Survey, Survey of Household Expenditures, and Survey of Labour and Income Dynamics. Two types of FRCs can contribute to a program/project: sponsoring FRCs and supplying FRCs. The two axes may coincide, but this is very rare for statistical programs/projects, which generally require multi-disciplinary teams.

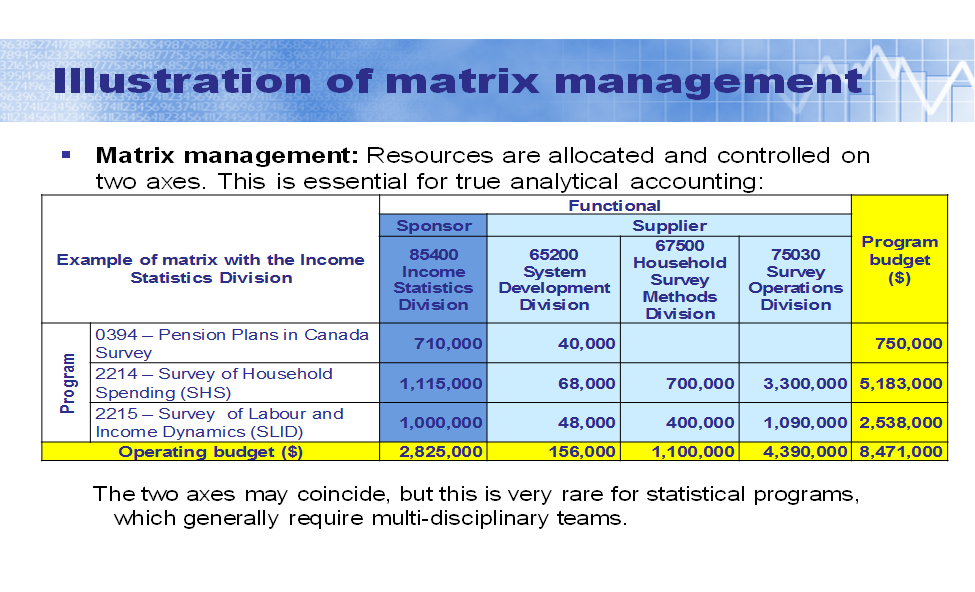

Figure 2.3.1: Illustration of matrix management

Description for Figure 2.2.1

This graphic represents the illustration of a matrix management. In matrix management, the resources are allocated and controlled on two axes. This is essential for true analytical accounting.

For the example of the matrix with the Income Statistics Division, the graphic is split vertically by programs, with the operating budget at the bottom. It is split horizontally by function (sponsor or supplier) with the program budget at the end.

For the Pension Plans in Canada Survey Program, the sponsor of Income Statistics Division gives 710,000. The supplier of System Development Division gives 40,000. The program budget is 750,000.

For the Survey of Household Spending (SHS) Program, the sponsor of Income Statistics Division gives 1,115,000. The supplier of System Development Division gives 68,000. The supplier of Household Survey Methods Divisions gives 700,000. The supplier of Survey Operations Divisions gives 3,300,000. The program budget is 5,183,000.

For the Survey of Labour and Income Dynamics (SLID) Program, the sponsor of Income Statistics Division gives 1,000,000. The supplier of System Development Division gives 48,000. The supplier of Household Survey Methods Divisions gives 400,000. The supplier of Survey Operations Divisions gives 1,090,000. The program budget is 2,538,000.

The operating budget of Income Statistics Division is 2,825,000. The operating budget of System Development Division is 156,000. The operating budget of Household Survey Methods Divisions is 1,100,000. The operating budget of Survey Operations Divisions is 4,390,000. The total budget is 8,471,000.

The two axes may coincide, but this is very rare for statistical programs, which generally require multi-disciplinary teams.

In this example, the total budget for all three programs is $8.471 million, but only one-third of the total program budget is sponsored by FRCs within the Income Statistics Division. The remainder is supplied by FRCs from other divisions, which provide services to support the various Income Statistics Division programs: Systems Development Division (IT services), Household Survey Methods Division (methodological services) and Survey Operations Division (survey operations).

For example, the manager of the Survey of Labour and Income Dynamics (SLID) is accountable for delivering this entire survey program, with a budget of $2.538 million, associated with the program element code 2215. The supplying FRCs are the functional units responsible for providing resources that contribute to the delivery of the SLID program; i.e., System Development Division (FRC 65200), Household Survey Methods Division (FRC 67500), and Survey Operations Division (FRC 75030). The FRCs that sponsor and supply resources for the SLID code their time to project element 2214 to manage the total budget for program element 2215.

Regular financial reviews are carried out on a functional basis (monthly) and on a program basis (quarterly) to provide robust oversight and control of funds, from both cash- and cost-accounting perspectives. The financially delegated managers, who sponsor and supply resources, sign off on these reviews because they are ultimately accountable for the financial management of these delegated resources and the related program outcomes.

2.2 Future Budget

As part of the Integrated Strategic Planning Process, managers must develop a financial plan to ensure that the statistical agency continues to fulfill its mission and mandate into the future. This process includes reviewing the base budget from government appropriations, proposing strategic investments, and confirming external funding for work carried out on a cost-recovery basis. For some strategic or cyclical investments (e.g., Census of Population and Census of Agriculture), it may also be necessary to develop a business case to request additional funding from the federal government (Parliament).

An integrated analysis of financial, human-resource and IT availabilities over a 10-year horizon provides a key tool for managers to ensure that all project approvals, many of which constitute multi-year investments, are made in the context of future operational requirements. This analysis also helps managers to project the availability of and demand for funding. The Report on Plans and Priorities, a compilation that explains the annual business plan is the official external planning report for federal departments and agencies in Canada (see Chapter 2.2: Integrated Strategic Planning).

2.3 Past budget

Given that a manager's primary concern is to spend funds and manage a budget according to the rules, and for a program's intended purpose, and in keeping with program objectives, the manager must report on this at the end of the fiscal year. The final functional review and program financial review carried out every year clearly demonstrates the surplus or deficit position of the program. The ability to successfully manage planned budgets with a small margin of variation is also part of the Performance Management Agreement of senior executives. Of course, some deviations from initial plans are virtually unavoidable across the vast range of programs usually found in a national statistical agency. That is why an accurate retrospective picture is important to assessing performance, to serving as a basis for funding adjustments and to assessing the financial implications of additions or subtractions to a program or service that may be contemplated as part of the strategic planning exercise.

At the end of each fiscal year, the organization prepares its Public Accounts, which present the financial operations of the agency and its use of the funding (Main Estimates) provided to the organization by Parliament. Those accounts are used for consolidation within government-wide financial statements, which the Auditor General of Canada audits and tables annually in the Parliament of Canada. The organization also produces the Departmental Performance Report (DPR), which is the official external performance report to the Parliament of Canada. The DPR provides an account of results achieved against planned performance expectations set out in the Report on Plans and Priorities (RPP).

Key success factors

The following are the four key successful practices or guiding principles for efficient control and management of funds: (1) transparency and public disclosure, (2) segregation of duties and clear responsibilities, (3) oversight of higher-risk operations and quality assurance, and (4) independent audit and evaluation functions.

- Transparency and public disclosure include three important components: timely reporting using standard templates and periodic forecasting (to fiscal year end) of program and functional expenditures; in-year adjustments to program funding and investments as per the evolution of the financial situation; and strong, dedicated financial professionals to support executives as strategic partners in providing advice and decision-making.

- Segregation of duties and clear accountabilities means taking into account the Delegation of Financial Signing Authorities and separating the authorizing authority from the payment authority. This also means that accountability for the sponsoring and supplying FRC managers is clearly defined and, thus, will ensure the most effective delivery of programs within the matrix management framework.

- Oversight of higher-risk operations and quality assurance include the following: Detailed regular reports (ideally monthly) and critical analysis of key performance indicators submitted to the Chief Financial Officer; a summary of financial highlights presented monthly to the Corporate Planning Committee (chaired by the Chief Statistician), and a multi-year perspective / projections to support the Integrated Strategic Planning Process.

- Independent audit and evaluation functions include the following: a five-year evaluation plan, which includes the full evaluation coverage of the agency's direct program spending over a five-year cycle, an evaluation committee, chaired by the Chief Statistician, which supports, oversees and monitors the evaluation function and management accountabilities arising from evaluations and evaluation-related products, and a Departmental Audit Committee, which actively oversees core areas of the agency's control and accountability in an integrated and systematic way—a critical aspect of a strong and credible internal audit regime

It is important for a national statistical office to have full control over the allocation of its budget. This ensures that the organization can be politically independent and allocate funds to the most important programs.

Challenges and next steps

The Canadian government is continuously improving and adapting its financial management function as the fiscal environment evolves. Any changes require organizations to remain current in terms of their financial procedures to ensure compliance. Recent challenges include allocating funds to the highest priorities in the context of fiscal restraint and providing effective and efficient monitoring of the financial environment to ensure that the agency has the capacity to react to new pressures or opportunities

Endnotes:

- Endnote 1

-

The Treasury Board Secretariat is a central agency of the Government of Canada. It provides advice and makes recommendations to the Treasury Board committee of ministers on how the government spends money on programs and services, how it regulates and how it is managed.

- Endnote 2

-

Statistics Canada has two main sources of funding: annual parliamentary appropriations (historical annual average between $500 million and $800 million) and funding from external partners (historical annual average of $100 million).

- Endnote 3

-

The Comptroller General of Canada is responsible for providing functional direction and assurance for financial management, internal audit, investment planning, procurement, project management, and the management of real property and materiel across the federal government.

Bibliography

Government of Canada (2016). Constitution Act, 1867. Consulted on the 31st of March 2016 and retrieved from http://laws.justice.gc.ca/eng/const/page-1.html.

Government of Canada (2016). Financial Administration Act (R.S.C., 1985, c. F-11). Consulted on the 31st of March 2016 and retrieved from http://laws-lois.justice.gc.ca/eng/acts/F-11/index.html.

Government of Canada (2016). Treasury Board of Canada Secretariat. Consulted on the 31st of March 2016 and retrieved from https://www.canada.ca/en/treasury-board-secretariat/index.html.

Government of Canada (2012). Policy on Internal Audit. Consulted on the 31st of March 2016 and retrieved from http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=16484.

Statistics Canada (2015). Report on Plans and Priorities 2015-2016. Consulted on the 31st of March 2016 and retrieved from http://www.statcan.gc.ca/eng/about/rpp/2015-2016/index.

Statistics Canada (2016). Departmental Performance Report 2014-2015. Consulted on the 31st of March 2016 and retrieved from http://www.statcan.gc.ca/eng/about/dpr/2014-2015/index.

- Date modified: