2 Methodology

Stephen J. Kaputa and Katherine Jenny Thompson

Previous | Next

2.1 Decile estimation

We consider two approaches to decile estimation for

continuous data: the sample decile (SD) method and interpolation. The SD method uses ordered sample weights to

locate the estimate (Rao and Shao 1996). For this, the characteristics values

are sorted in ascending order, and the sample weights are accumulated until

they exceed the desired decile's percent of the total weight.

Interpolation methods group the continuous data in bins and interpolate over the bin

containing the decile. To obtain the decile estimate we use the Woodruff formula (Woodruff 1952)

for interpolation provided below:

where

cumulative

frequency of the characteristic using sample weights,

lower

limit of the bin containing the decile,

estimated

total number of elements in the population,

cumulative

frequency in all intervals preceding the bin containing the sample decile,

decile

class frequency (estimated total number of elements in the population of the

interval containing the sample decile),

width

of the bin containing the sample decile,

desired

decile (0.1, 0.2, 0.3, … , 0.9).

Notice that this formula does not require that each bin

to be of equal length. However, it does require that the data within each bin

be uniformly distributed. This later requirement poses the true challenge with

a highly skewed population, especially in the upper tail.

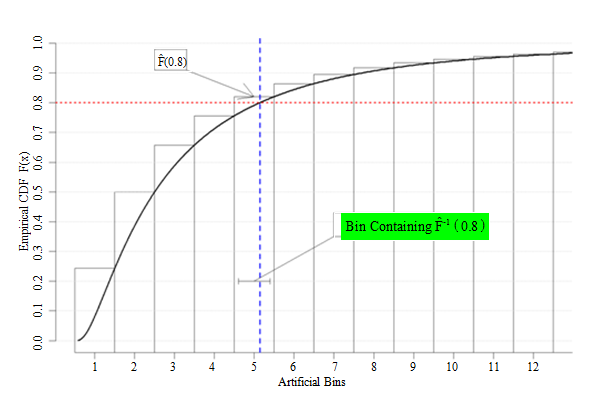

Figure 2.1 below illustrates how to use the Woodruff

method to estimate the 80th decile. The sample data have been

grouped into twelve separate bins. The empirical CDF is produced from the

complete set of weighted sample data (as one referee noted, the empirical CDF

is extremely smooth for sample survey data; in practice, the curve would

include discrete steps. The Woodruff method procedure would be the same,

however). The decile estimate is located at the intersection of the empirical CDF

curve and red asymptote at The 80th decile is contained in the 5th bin; the

interpolated estimate of the 80th percentile would therefore be

obtained by using (2.1) over the fifth bin.

Description for figure 2.1

Figure 2.1 Illustration of the Woodruff method

Determining the optimal bin size for both estimation and

variance estimation can be difficult. As the bins narrow (approaching width 1),

then the variance estimates become more unstable. Smoothing the estimates via

the interpolation reduces the instability of variance, but increases the bias

in the estimate. The bias component increases as the bin widths increase.

Economic data generally have a positive skewed

distribution. Moreover, the subdomains' characteristic distributions will vary,

and their respective moments change over time as the economy changes.

Consequently, developing a standard set of fixed bins for interpolation that

work consistently over time is nearly impossible. Instead, Thompson and Sigman

(2000) developed a "data-dependent� binning procedure, where the width of each

bin is determined separately by the estimation cell. Their recommended method

linearly transforms each characteristic to a standard scale and then uses a

standard set of bins for every characteristic. The authors use the following

linear transformation

where is the 75th percentile (3rd

quartile) of the sample distribution, obtained using the SD method. The

interpolated-median estimate of the is multiplied by to obtain a value on the original scale. This

procedure is equivalent to simply dividing the original sample in each

estimation cell from 0 to into bins of equal width and placing the remainder

of the sample into one bin, which, by design, is much larger than the others.

With the highly positive skewed housing data, this transformation works well

for estimating the median because it is far from the scaling parameter. However, it does not permit

estimation of either the 80th or 90th deciles. Thus, if

we wanted to continue using an interpolation method, we needed to consider

alternative transformations.

The simplest approach is to

use the original data-dependent bin method with a higher scaling parameter, i.e., use any percentile value larger

than 90%. We use the 95th percentile as the scaling factor and

hereafter refer to this method as the "P95 method�.

The P95 method does create uniform distributions within

the majority of the bins but is still problematic at the upper end of the

distribution for two reasons. First, the final bin contains only five percent

of the sample distribution, and the values within this bin are generally very

different. Second, the data-dependent binning procedure requires that each

decile be "far from� the large final bin; if not, then the decile estimates

exhibit the same instability as those obtained using the "SD method�.

Unfortunately, the bin containing the 90th percentile is often close

to the final bin when using a scaling parameter of 95%.

To address the second issue, we considered another

data-binning approach, denoted as the "P75 method�. For this, we create two

sets of bins per estimation cell, each with different widths above and below

the cell's value. This requires two separate linear

transformations per estimation cell, given by

The is then placed into equal length bins, and into equal length bins, where The interpolation is performed independently

for each decile, with the appropriate inverse transformation being applied to

each interpolated decile. This procedure ensures that median estimates exactly

match those obtained with the current procedure.

Our third considered interpolation approach makes

parametric assumptions about the characteristics. Often, economic data are

approximately log-normally distributed (e.g.,

Steel and Fay 1995). The Normal Binning method (denoted "NB�) uses the

properties of the normal distribution applied to the log-transformed data to

obtain data-dependent bins. The binning technique ensures that areas of high

probability have smaller bin widths to limit the amount of observations per bin

and areas of low probability have larger bin width to increase the amount of

observations per bin.

The NB method centers the log-transformed data around

the weighted sample median, then scales the centered data by an estimate of the

population standard deviation. We use the sample median because it is more

outlier resistant than the sample mean. Of course, the mean and median are

equivalent with normally distributed data. Given a standard normal distribution

where and then

We estimated the standard deviation (sigma) as the ratio

where the IQR

is obtained from the empirical CDF in the estimation cell. To normalize the data,

we applied the following transformation

where

log-transformed sample median over domain

log-transformed sample interquartile range

over domain

Again, the

sample deciles and interquartile ranges are obtained via the SD method. If

the data are log-normally distributed, should have a standard normal distribution, so

that roughly 68.3% of the data are within one standard deviation of the mean

and 95.4% of the data are within two standard deviations of the mean. Using

those properties, we split the transformed into the five different zones and created the

45 bins shown in Table 2.1.

Table 2.1

Bins for the log-normal transformation (Normal method)

Table summary

This table displays Bins for the log-normal transformation. The information is grouped by zone (appearing as row headers), 1, 2, 3, 4, 5 (appearing as column headers).

|

Zone

|

1

|

2

|

3

|

4

|

5

|

|

Range

|

[Low, -2)

|

[-2, -1)

|

[-1, 1)

|

[1, 2)

|

[2, High]

|

|

Percent in Zone

|

2.3

|

13.6

|

68.2

|

13,6

|

2.3

|

|

Bins

|

1

|

6

|

31

|

6

|

1

|

|

Average Percent of Sample Units per Bin

|

2.3

|

2.3

|

2.2

|

2,3

|

2.3

|

There are four different bin widths with roughly the

same average percentage of sampled units per bin. Woodruff's method is applied

to the transformed data to obtain the deciles and we exponentiate these decile

estimates to obtain values on the original scale. Unlike the linear rescaling

methods presented above, there is an additional induced estimation bias caused

by the power transformation. It may have been possible to make a bias

adjustment for the transformation via a Taylor expansion, as suggested by a

referee, but we did not consider this approach.

2.2 Variance estimation

The MHS replication method (aka "Fay's method�) is a

"compromise� between the stratified jackknife and the BRR method (Fay 1989).

Rao and Shao (1999) demonstrate that the MHS variance estimator is

asymptotically consistent for both smooth statistics such as ratio estimators

and for non-smooth statistics such as sample quantiles estimated using the SD

method outlined in 2.1. Their paper does not extend this property to

interpolated decile estimates, although it does follow that these variance

estimates should be consistent as the bin width approaches width 1. Like BRR,

MHS replication uses a Hadamard matrix to form replicates, but uses replicate

weights of 1.5 and 0.5 instead of the values of 2 and 0 used in BRR. The MHS

formula for standard error estimation of any estimate is

where is the replicate estimate and is the full sample estimate. The sum of

squared error term is adjusted by a factor of to prevent negative bias in

the variance estimate (Judkins 1990).

Previous | Next