Archived - 2018 Annual Greenhouse, Sod and Nursery Survey

Why do we conduct this survey?

This survey collects up-to-date information on the production and value of greenhouse plants and vegetables, and on the production of nursery stock and sod in Canada.

Agriculture and Agri-Food Canada, producer associations, and provincial agriculture departments use the data to perform market trend analysis and to study domestic production and imports. The data are also used to calculate farm cash receipts.

Your information may also be used by Statistics Canada for other statistical and research purposes.

Your participation in this survey is required under the authority of the Statistics Act.

Other important information

Authorization to collect this information

Data are collected under the authority of the Statistics Act, Revised Statutes of Canada, 1985, Chapter S-19.

Confidentiality

By law, Statistics Canada is prohibiated from releasing any information it collects that could identify any person, business, or organization, unless consent has been given by the respondent, or as permitted by the Statistics Act. Statistics Canada will use the information from this survey for statistical purposes only.

Record linkages

To enhance the data from this survey and to reduce the reporting burden, Statistics Canada may combine the acquired data with information from other surveys or from administrative sources.

Data-sharing agreements

To reduce respondent burden, Statistics Canada has entered into data-sharing agreements with provincial and territorial statistical agencies and other government organizations, which have agreed to keep the data confidential and use them only for statistical purposes. Statistics Canada will only share data from this survey with those organizations that have demonstrated a requirement to use the data.

Section 11 of the Statistics Act provides for the sharing of information with provincial and territorial statistical agencies that meet certain conditions. These agencies must have the legislative authority to collect the same information, on a mandatory basis, and the legislation must provide substantially the same provisions for confidentiality and penalties for disclosure of confidential information as the Statistics Act. Because these agencies have the legal authority to compel businesses to provide the same information, consent is not requested and businesses may not object to the sharing of the data.

For this survey, there are Section 11 agreements with the provincial statistical agencies of Newfoundland and Labrador, Nova Scotia, New Brunswick, Quebec, Ontario, Manitoba, Saskatchewan, Alberta and British Columbia. The shared data will be limited to information pertaining to business establishments located within the jurisdiction of the respective province.

Section 12 of the Statistics Act provides for the sharing of information with federal, provincial or territorial government organizations. Under Section 12, you may refuse to share your information with any of these organizations by writing a letter of objection to the Chief Statistician, specifying the organizations with which you do not want Statistics Canada to share your data and mailing it to the following address:

Chief Statistician of Canada

Statistics Canada

Attention of Director, Enterprise Statistics Division

150 Tunney's Pasture Driveway

Ottawa, Ontario

K1A 0T6

You may also contact us by email at statcan.esdhelpdesk-dsebureaudedepannage.statcan@statcan.gc.ca or by fax at 613-951-6583.

For this survey, there is a Section 12 agreement with the Prince Edward Island statistical agency.

For agreements with provincial and territorial government organizations, the shared data will be limited to information pertaining to business establishments located within the jurisdiction of the respective province or territory.

Business or organization and contact information

1. Verify or provide the business or organization's legal and operating name and correct where needed.

Note: Legal name modifications should only be done to correct a spelling error or typo.

Legal Name

The legal name is one recognized by law, thus it is the name liable for pursuit or for debts incurred by the business or organization. In the case of a corporation, it is the legal name as fixed by its charter or the statute by which the corporation was created.

Modifications to the legal name should only be done to correct a spelling error or typo.

To indicate a legal name of another legal entity you should instead indicate it in question 3 by selecting 'Not currently operational and then choosing the applicable reason and providing the legal name of this other entity along with any other requested information.

Operating Name

The operating name is a name the business or organization is commonly known as if different from its legal name. The operating name is synonymous with trade name.

- Legal name

- Operating name (if applicable)

2. Verify or provide the contact information of the designated business or organization contact person for this questionnaire and correct where needed.

Note: The designated contact person is the person who should receive this questionnaire. The designated contact person may not always be the one who actually completes the questionnaire.

- First name

- Last name

- Title

- Preferred language of communication

- English

- French

- Mailing address (number and street)

- City

- Province, territory or state

- Postal code or ZIP code

- Country

- Canada

- United States

- Email address

- Telephone number (including area code)

- Extension number (if applicable)

The maximum number of characters is 5 - Fax number (including area code)

3. Verify or provide the current operational status of the business or organization identified by the legal and operating name above.

- Operational

- Not currently operational

Why is this business or organization not currently operational?- Seasonal operations

- When did this business or organization close for the season?

- Date

- When does this business or organization expect to resume operations?

- Date

- When did this business or organization close for the season?

- Ceased operations

- When did this business or organization cease operations?

- Date

- Why did this business or organization cease operations?

- Bankruptcy

- Liquidation

- Dissolution

- Other - Specify the other reasons why the operations ceased

- When did this business or organization cease operations?

- Sold operations

- When was this business or organization sold?

- Date

- What is the legal name of the buyer?

- When was this business or organization sold?

- Amalgamated with other businesses or organizations

- When did this business or organization amalgamate?

- Date

- What is the legal name of the resulting or continuing business or organization?

- What are the legal names of the other amalgamated businesses or organizations?

- When did this business or organization amalgamate?

- Temporarily inactive but will re-open

- When did this business or organization become temporarily inactive?

- Date

- When does this business or organization expect to resume operations?

- Date

- Why is this business or organization temporarily inactive?

- When did this business or organization become temporarily inactive?

- No longer operating due to other reasons

- When did this business or organization cease operations?

- Date

- Why did this business or organization cease operations?

- When did this business or organization cease operations?

- Seasonal operations

4. Verify or provide the current main activity of the business or organization identified by the legal and operating name above.

Note: The described activity was assigned using the North American Industry Classification System (NAICS).

This question verifies the business or organization's current main activity as classified by the North American Industry Classification System (NAICS). The North American Industry Classification System (NAICS) is an industry classification system developed by the statistical agencies of Canada, Mexico and the United States. Created against the background of the North American Free Trade Agreement, it is designed to provide common definitions of the industrial structure of the three countries and a common statistical framework to facilitate the analysis of the three economies. NAICS is based on supply-side or production-oriented principles, to ensure that industrial data, classified to NAICS, are suitable for the analysis of production-related issues such as industrial performance.

The target entity for which NAICS is designed are businesses and other organizations engaged in the production of goods and services. They include farms, incorporated and unincorporated businesses and government business enterprises. They also include government institutions and agencies engaged in the production of marketed and non-marketed services, as well as organizations such as professional associations and unions and charitable or non-profit organizations and the employees of households.

The associated NAICS should reflect those activities conducted by the business or organizational units targeted by this questionnaire only, as identified in the 'Answering this questionnaire' section and which can be identified by the specified legal and operating name. The main activity is the activity which most defines the targeted business or organization's main purpose or reason for existence. For a business or organization that is for-profit, it is normally the activity that generates the majority of the revenue for the entity.

The NAICS classification contains a limited number of activity classifications; the associated classification might be applicable for this business or organization even if it is not exactly how you would describe this business or organization's main activity.

Please note that any modifications to the main activity through your response to this question might not necessarily be reflected prior to the transmitting of subsequent questionnaires and as a result they may not contain this updated information.

The following is the detailed description including any applicable examples or exclusions for the classification currently associated with this business or organization.

Description and examples

- This is the current main activity

- This is not the current main activity

Provide a brief but precise description of this business or organization's main activity

e.g., breakfast cereal manufacturing, shoe store, software development

Main activity

5. You indicated that is not the current main activity. Was this business or organization's main activity ever classified as: ?

- Yes

When did the main activity change?

Date - No

6. Search and select the industry classification code that best corresponds to this business or organization's main activity.

Select this business or organization's activity sector (optional)

- Farming or logging operation

- Construction company or general contractor

- Manufacturer

- Wholesaler

- Retailer

- Provider of passenger or freight transportation

- Provider of investment, savings or insurance products

- Real estate agency, real estate brokerage or leasing company

- Provider of professional, scientific or technical services

- Provider of health care or social services

- Restaurant, bar, hotel, motel or other lodging establishment

- Other sector

Type of production

1. Which of the following products did you grow for sale in 2018?

Please report Canadian production only.

Select all that apply.

Greenhouse products

Seedlings, potted plants, bedding plants, cuttings and other propagating material, vegetables and fruit grown for sale in a permanent, artificially heated enclosed structure made of plastic, plexiglass, poly-film or glass.

Any plants that you start cultivating in a greenhouse but are finished before sales in a nursery should be considered a nursery product.

Nursery products

A diverse range of non-edible, living plant material grown 'in field' or in containers outdoors and sold with their root system intact. Plants range from tree seedlings to full-grown trees.

Include annual and perennial plants.

Exclude field-grown cut flowers from this category.

Field-grown cut flowers should be reported in its own category only, not in the 'nursery products' category. Cut flowers produced in, and sold from, a greenhouse should be reported in the 'greenhouse products' category

Christmas trees

Include only the Christmas trees that were cut during the year.

Exclude Christmas trees that were grown in a container with their root systems intact.

Sod

Grass or turf, which has its roots intact. Sod is grown 'in field' and sold as a single product.

- Greenhouse products

Include vegetables, fruits, flowers and plants grown in heated structures.

Exclude vegetables and fruit grown outdoors or in non-heated covering tunnels or cold frames. - Christmas trees

- Field-grown cut flowers

- Nursery products

e.g., trees, shrubs and plants - Sod

- Did not grow any products for sale in 2018

Greenhouse area - unit of measure

2. What unit of measure will be used to report your greenhouse area?

- Square feet

- Square metres

- Acres

- Hectares

Greenhouse area

3. What was your greenhouse area under the following materials in 2018?

Exclude non-heated covering tunnels, cold frames or any area surrounding a greenhouse.

| Unit of measure | |

|---|---|

| Under glass | |

| Poly-film | |

| Rigid plastic, fibreglass or other enclosed area | |

| Total greenhouse area |

Greenhouse products - number of months in operation

4. How many months was your greenhouse in operation in 2018?

Report the number of months this operation was growing plants in a greenhouse.

- Months

Greenhouse products

5. Which of the following greenhouse products were grown for sale in 2018?

Select all that apply.

For this survey, we are only interested in flowers, plants, vegetables, fruits, tree seedlings and bedding plants grown in, and sold from, the greenhouse. Production of vegetables and fruits covered by cold frames or covering tunnels should not be included in the greenhouse section of the survey.

Potted herbs

Plants that will be maintained in a pot by the consumer after purchase should be reported inside the 'potted plants' section. Herb plants sold in a package ready to be consumed should be reported inside the vegetable section.

Cut flowers

Include only cut flowers produced in, and sold from, a greenhouse.

Exclude field-grown cut flowers and dried cut flowers.

Fruit and Vegetables

Include products grown to completion in a greenhouse and sold from the greenhouse.

Exclude greenhouse vegetables and/or fruit that are transplanted for field crops. Bedding plants (transplants) grown in a greenhouse that will be planted in your own fields so that they can be sold as fully grown harvested vegetables at a later date should be excluded; they are reported in Statistics Canada's annual Fruit and Vegetable Survey.

Potted Plants - indoor and outdoor

Any plants grown and sold in a pot from the greenhouse.

Exclude Christmas trees sold in pots. Pots take many forms and sizes, such as baskets (wicker), peat pots, moss pots and plastic pots or ceramic pots.

Cuttings and tree seedlings

Plants (or sections of a plant) capable of developing into a greater number of plants or spreading out and affecting a greater area. Examples include Chrysanthemums, Poinsettias, Begonias, Petunias and shrubs.

Exclude tree seedlings for reforestation.

Bedding plants, also known as transplants

Young plants that are bought and then transplanted into a garden, field, container or basket by the purchaser. These include ornamental bedding plants and vegetable bedding plants. For this survey, the term "ornamental" refers to flowers or plants cultivated for their beauty rather than use.

- Fruits and vegetables

- Potted plants - indoor or outdoor

Include any prefinished or finished plants grown and sold in a pot. - Cuttings and tree seedlings

Exclude tree seedlings for reforestation. - Bedding plants, transplants or plugs - ornamental or vegetable

Include plants sold in cell packs or trays that are ready for transplanting by the purchaser. - Cut flowers

Exclude dried cut flowers.

Greenhouse products - fruits and vegetables

6. What area of your greenhouse was used to produce the following fruits and vegetables in 2018?

For any multiple plantings of the same fruit or vegetable, count the area only once.

Greenhouse vegetables and fruits are edible and ready to eat at the time of sale. They were grown into sellable products in a greenhouse, not in a field; and sold from the greenhouse by the producer. Field vegetable and fruit farmers should report their production in the Fruit and Vegetable Survey.

Exclude tobacco, ginseng, asparagus, mushrooms, ornamental and vegetable bedding plants (young plants that are bought and transplanted into a garden, field, container or basket by the purchaser; also known as transplants).

A number of greenhouses are expanding to the United States. For this survey, report Canadian production only.

If you produced a multiple crop of the same greenhouse vegetable or fruit in the same greenhouse space, report the area only once. For example, if 1,000 square feet were used for the first tomato crop planting and then the same space was later used for the second tomato crop planting, you would report 1,000 square feet (not 2,000 square feet).

If you produced two or more different types of vegetables or fruit in the same greenhouse space, you would count that area for each type of crop produced.

For example, if you used 2,000 square feet to grow tomatoes for your first crop planting, and then switched to growing cucumbers in that same space half-way through the summer, you would report a total area of 4,000 square feet (2,000 square feet for growing tomatoes, plus 2,000 square feet for growing cucumbers).

| Unit of measure | |

|---|---|

| Greenhouse tomatoes | |

| Beefsteak tomatoes | |

| Large tomatoes on the vine | |

| Cherry and grape tomatoes | |

| Other tomatoes | |

| Total greenhouse tomatoes | |

| Greenhouse cucumbers | |

| English cucumbers | |

| Mini cucumbers | |

| Other cucumbers | |

| Total greenhouse cucumbers | |

| Other greenhouse fruits and vegetables | |

| Greenhouse eggplants | |

| Greenhouse Chinese vegetables | |

| Greenhouse herbs | |

| Sprouts grown in a controlled environment | |

| Greenhouse microgreens and shoots | |

| Greenhouse peppers | |

| Greenhouse lettuce | |

| Greenhouse beans (green and wax) | |

| Other greenhouse fruit or vegetable 1 | |

| Other greenhouse fruit or vegetable 2 | |

| Other greenhouse fruit or vegetable 3 | |

| Total area of fruits and vegetables |

7. For the following fruits and vegetables, what were the quantity sold ( i.e., marketed production) and sales in 2018?

| Quantity sold | Unit of measure | Total Sales | |

|---|---|---|---|

| Greenhouse tomatoes | |||

| Beefsteak tomatoes | |||

| Large tomatoes on the vine | |||

| Cherry and grape tomatoes | |||

| Other tomatoes | |||

| Total greenhouse tomatoes | |||

| Greenhouse cucumbers | |||

| English cucumbers | |||

| Mini cucumbers | |||

| Other cucumbers | |||

| Total greenhouse cucumbers | |||

| Other greenhouse fruits and vegetables | |||

| Greenhouse eggplants | |||

| Greenhouse Chinese vegetables | |||

| Greenhouse herbs | |||

| Sprouts grown in a controlled environment | |||

| Greenhouse microgreens and shoots | |||

| Greenhouse peppers | |||

| Greenhouse lettuce | |||

| Greenhouse beans (green and wax) | |||

| Other greenhouse fruit or vegetable 1 | |||

| Other greenhouse fruit or vegetable 2 | |||

| Other greenhouse fruit or vegetable 3 | |||

| Total gross sales of fruits and vegetables | |||

Unit of measure

|

|||

8. Of the total gross sales reported at question 7, please provide the percentage breakdown of your greenhouse fruits and vegetables sales across the following distribution channels.

Sales distribution of greenhouse vegetables and fruit (total gross sales)

The sales of greenhouse vegetables and fruit that the operation produced and sold.

Please report the value of greenhouse fruite and vegetable sales in a percentage (%). The sum of different markets should be equal to 100% of the value reported in in question 7.

Wholesaler

The organisation primarily engaged as the intermediary in the distribution of merchandise. Meaning that a wholesaler is a reseller of manufactured goods in whole (without transformation, and rendering services incidental to the sale of merchandise).

A wholesaler provides the warehousing and trade abilities the manufacturer does not want to provide. It also prefers to sell batches, truckloads, pallets, etc. of goods. Often offers discounts as quantity increases. As a result, many wholesalers are therefore organized to sell merchandise in large quantities to retailers, and business and institutional clients.

In addition, wholesalers may frequently perform one of the following related functions; breaking bulk, providing delivery services to customers, or operating warehouse facilities for storage of goods they sell, or marketing and support services such as packaging and labelling, inventory management, shipping, handling of warranty claims, in-store or co-op promotions and training.

| Percentage of total sales | |

|---|---|

| Sales to domestic wholesalers | |

| Sales to mass market chain stores | |

| Sales to other greenhouses | |

| Sales of exports directly from your operation | |

| Sales to the public from your greenhouse, roadside stand or other outlets | |

| Sales through all other distribution channels | |

| Total sales of fruits and vegetables |

Greenhouse products - indoor and outdoor potted plants

9. For the following indoor and outdoor potted plants, how many pots did this greenhouse produce and sell in 2018?

Include only prefinished and finished potted plants grown and sold by this greenhouse operation.

Exclude:

- bedding plants or plugs sold in cell packs, flats or trays for transplanting

- nursery-grown stock, such as potted shrubs or fall mums

- Christmas trees sold in pots

- plants purchased or imported by this operation for immediate resale.

Include all ornamental potted plants (annuals, biennials and perennials) and all potted vegetable, fruit and herb plants that were produced and sold from your greenhouse in Canada.

Plants grown in containers outdoors should be reported in the 'nursery products' category.

Exclude anything produced outside Canada.

Exclude Christmas trees sold in pots; bedding plants or plugs sold in cell packs, flats or trays; and other nursery stock (non-edible, living plant material grown outdoors 'in field' or in containers outdoors and sold with their root system intact).

Any plant grown in a pot from the greenhouse with the intention of selling to the final consumer can be classified as a finished potted plant (including hanging potted plants, such as baskets (wicker), peat pots, moss pots and plastic pots or ceramic pots). Any plant sold in a pot before it has fully matured or is intended to be grown to maturity at another facility can be classified as a prefinished potted plant.

| Number of pots produced and sold | |

|---|---|

| Azaleas | |

| Lilies | |

| Poinsettias | |

| African Violets | |

| Tropical foilage and green plants | |

| Gerberas | |

| Miniature Roses | |

| Orchids | |

| Kalanchoes | |

| Chrysanthemums or Potted Mums | |

| Primulas | |

| Cyclamens | |

| Tulips | |

| Indoor hanging pots | |

| Other indoor potted plants | |

| Outdoor potted plants | |

| Begonias | |

| Chrysanthemums, garden | |

| Geraniums, in pots only | |

| New Guinea Impatiens / Hawkeri | |

| Petunias | |

| Herbaceous perennials | |

| Argyranthemums | |

| Outdoor hanging pots | |

| Calibrachoas | |

| Dahlias | |

| Pansies | |

| Rudbeckias | |

| Heliopsis | |

| Verbenas | |

| Zinnias | |

| Potted herb plants | |

| Potted vegetable plants | |

| Other outdoor potted plants | |

| Total number of pots, indoor and outdoor, produced and sold |

10. What were the total gross sales of prefinished and finished potted plants in 2018?

- Total gross sales

Greenhouse products - cuttings and tree seedlings

11. For the following cuttings, what was the total number of cuttings produced and sold in 2018?

Include only cuttings produced by this greenhouse operation.

Cuttings are sections of a plant stem capable of developing into a whole plant. Examples of species that may be sold as cuttings include murrayas, grevilleas, fuchsias, and gardenias.

Exclude ornamental and vegetable bedding plants, also known as transplants, which are young plants that are bought and then transplanted into a garden, field, container or basket by the purchaser.

| Total number of cuttings produced and sold | |

|---|---|

| Chrysanthemum | |

| Poinsettia | |

| Geranium | |

| Impatien | |

| Other cuttings not listed | |

| Total number of cuttings produced and sold |

12. What were the total gross sales of cuttings in 2018?

- Total gross sales

13. What was the total number of tree seedlings produced and sold in 2018?

Include only tree seedlings produced by this greenhouse operation.

Exclude:

- nursery products grown in a cold-frame or non-heated tunnel

- tree seedlings for reforestation.

A tree seedling is a young tree grown from a seed in a nursery or greenhouse for transplanting typically at one or two years of age.

Include tree seedlings produced only inside a greenhouse. Do not report tree seedlings produced in cold frames or covering tunnels.

- Number of seedlings

14. What were the total gross sales of tree seedlings in 2018?

- Total gross sales

Greenhouse products - bedding plants/transplants - vegetable and/or ornamental

15. What were the number and total gross sales of bedding plants, transplants or plugs produced and sold in 2018?

Include plants ready for transplanting by the purchaser into gardens, fields, containers and baskets.

Report the number of individual plants. If the number is unknown, please estimate it by multiplying the number of trays by the average number of plants per tray.

Bedding plants, also known as transplants, are young plants that are bought and then transplanted into a garden, field, container or basket by the purchaser. Ornamental bedding plants are cultivated for their flowers and beauty, rather than their use. Vegetable bedding plants are not yet edible at the time of sale from your greenhouse.

Bedding plants may be sold in various containers, including plugs, cell packs, flats or trays. Report the number of individual plants. If this number is unknown, please estimate it by multiplying the number of trays by the average number of plants per tray.

Exclude vegetable and herb plants not sold directly from the greenhouse (for example, plants being transplanted from the greenhouse to the field by the producer).

| Number of plants | Total gross sales | |

|---|---|---|

| Ornamental bedding plants | ||

| Vegetable bedding plants |

Greenhouse products - cut flowers

16. For the following cut flowers, what was the total number of stems produced and sold in 2018?

Exclude:

- dried cut flowers

- field-grown flowers (these will be reported in question 22)

- flowers grown by another operation.

Include only cut flowers that were produced in, and sold from, a greenhouse in Canada.

Exclude cut flowers that were initially cultivated in a greenhouse but then grown into sellable products in a field; these should be reported in the 'field-grown cut flowers' section, which is its own category in this survey. Some operators may start seeds in their greenhouse but transplant the flowers in the field in May or June and cut and dry them in August.

Exclude any cut flowers you purchased from other growers to re-sell from your own operation within a short period of time with minimal maintenance work (watering).

| Number of stems produced and sold | |

|---|---|

| Alstroemerias | |

| Chrysanthemums | |

| Daffodils | |

| Freesias | |

| Gerberas | |

| Irises | |

| Lilies | |

| Roses | |

| Snapdragons | |

| Tulips | |

| Lisianthus | |

| Other cut flowers not listed | |

| Total number of stems produced and sold |

17. What were the total gross sales of cut flowers grown by this greenhouse operation in 2018?

- Total gross sales

Greenhouse products - flowers and plants

18. What were your total gross sales of flowers and plants purchased from other greenhouses for immediate resale in 2018?

- Total gross sales

- Did not purchase and re-sell any flowers or plants

Summary - flowers and plants

19. This is a summary of your total gross sales of greenhouse flowers and plants in 2018?

| Sales | |

|---|---|

| Total gross sales of potted plants | |

| Total gross sales of cuttings | |

| Total gross sales of tree seedlings | |

| Total gross sales of ornamental bedding plants, transplants or plugs | |

| Total gross sales of vegetable bedding plants, transplants or plugs | |

| Total gross sales of cut flowers | |

| Total sales of flowers and plants produced in your greenhouse | |

| Total gross sales of flowers and plants purchased from other greenhouses for immediate resale | |

| Total gross sales of greenhouse flowers and plants |

Greenhouse products - flowers and plants

20. Of your total gross sales [amount] reported, please provide the percentage breakdown of greenhouse flowers and plants sales across the following distribution channels.

Sales distribution of greenhouse flowers and plants (total gross sales)

The sales of greenhouse flowers and plants that the operation produced and purchased for immediate resales.

Please report the value of greenhouse flower and plant sales in percentage (%). The sum of different markets should be equal to 100%.

Wholesaler

The organisation primarily engaged as the intermediary in the distribution of merchandise. Meaning that a wholesaler is a reseller of manufactured goods in whole (without transformation, and rendering services incidental to the sale of merchandise).

A wholesaler provides the warehousing and trade abilities the manufacturer does not want to provide. It also prefers to sell batches, truckloads, pallets, etc. of goods. Often offers discounts as quantity increases. As a result, many wholesalers are therefore organized to sell merchandise in large quantities to retailers, and business and institutional clients.

In addition, wholesalers may frequently perform one of the following related functions; breaking bulk, providing delivery services to customers, or operating warehouse facilities for storage of goods they sell, or marketing and support services such as packaging and labelling, inventory management, shipping, handling of warranty claims, in-store or co-op promotions and training.

| Percentage of total sales | |

|---|---|

| Sales to retail florists | |

| Sales to domestic wholesalers | |

| Sales to mass market chain stores | |

| Sales to other greenhouses | |

| Export sales made directly by your firm | |

| Sales made directly to the public from your greenhouse or roadside stands | |

| Sales to the government and other public institutions | |

| Other methods of sales not listed | |

| Total sales of flowers and plants |

Christmas trees

21. Please enter the total area used to grow Christmas trees, the number of trees produced and cut, and the total gross sales of trees in 2018?

Include only the Christmas trees that were cut during the year.

Exclude Christmas trees that were grown in a container with their root systems intact.

When reporting the area, include the total area used to grow Christmas trees, regardless of whether the trees were cut or not. Include naturally established or planted areas, regardless of stage of growth,that are pruned or managed with the use of fertilizer or pesticides.

When reporting the number of cut trees, exclude any Christmas trees that were grown in a container with their root systems intact.

Conversions

- 1 arpent = 0.9986 acres

- 1 acre = 1.0014 arpent

- 1 acre = 0.41 hectares

- 1 hectare = 2.47 acres

- Total area

- Number of cut trees

- Total gross sales

Unit of measure

- acres

- hectares

- arpents

Field-grown cut flowers

22. Please report the total area used to grow field-grown flowers, the number of cut stems produced and sold, and the total gross sales of field-grown cut flowers in 2018?

Include field-grown fresh and dried flowers, and any plant part used for floral or decorative purposes, such as seed heads, stalks and woody cuts.

Exclude cut flowers grown in a greenhouse from start to finish.

- Total area

- Number of cut stems

- Total gross sales

Unit of measure

- acres

- hectares

- arpents

Nursery products - nursery area

23. What was the total nursery area used for growing nursery stock in 2018?

| Nursery area | Unit of measure | |

|---|---|---|

| Field area used for growing nursery stock | ||

| Container area used for growing nursery stock | ||

| Total nursery area | ||

Unit of measure

|

||

Nursery products - nursery stock

24. How many field-grown and container-grown plants did this operation produce and sell in 2018?

Exclude:

- stock purchased for immediate resale

- Christmas trees without the root system intact

- heated greenhouse production and unsold inventory.

A tree seedling is a young tree grown from a seed in a nursery for transplanting typically at one or two years of age.

Include only tree seedlings produced in a nursery.

Exclude tree seedlings produced in and sold from a greenhouse.

Exclude tree seedlings for reforestation.

Note: tree seedlings may be reported as nursery products if they were conditioned outside for part of the production cycle, after having been cared for inside the greenhouse first.

| Number of field-grown plants produced and sold | Number of container-grown plants - produced and sold | |

|---|---|---|

| Trees - conifer | ||

| Trees - fruit | ||

| Trees - shade or ornamental | ||

| Shrubs - evergreen and conifer | ||

| Shrubs - evergreen and broadleaf | ||

| Shrubs - deciduous | ||

| Vines | ||

| Perennials and annuals | ||

| Small fruit bushes | ||

| Tree seedlings | ||

| Other type of plants | ||

| Total number of field and container grown nursery stock |

25. What were the total gross sales of field-grown and container-grown nursery stock in 2018?

Exclude sales of stock purchased for immediate resale and revenue from landscaping activities.

Exclude:

- any nursery stock that was purchased for immediate resale

- Christmas trees without the root system intact

- any greenhouse production

- unsold inventory

- value received for landscaping services.

Field-grown includes all bailed and burlapped, bare root field potted stock.

Container-grown includes all containers sizes of less than one gallon; one gallon; two gallons; and greater than two gallons.

Balled and burlapped is a method of transplanting that minimizes root disturbance. The tree is dug with a ball of soil around it and wrapped in burlap (method generally used for evergreens and deciduous plants in leaf).

Bare root describes plants dug up, with the soil shaken off (method generally used for deciduous plants in a dormant condition).

Field-potted describes stock which is grown in the field and placed into a pot when dug up for sale. Please report stock that was potted up from the field for a maximum of one full growing season; if potted up for more than one growing season, report under container.

Container-grown is nursery stock grown in a container for a minimum of one growing season before time of sale.

| Total Gross Sales | |

|---|---|

| Total gross sales of field-grown stock | |

| Total gross sales of container-grown stock | |

| Total gross sales of stock grown by this nursery operation |

26. What were the total gross sales of nursery stock purchased for immediate resale in 2018?

Nursery stock for immediate resale is any nursery stock you purchased from other growers to re-sell from your own operation within a short period of time with minimal maintenance e.g., watering. Please enter your total sales of the nursery stock you purchased from other operations.

Examples of stock that may be ready for immediate resale:

Plants, flowers, bulbs, trees, shrubs, etc.

- Total gross sales

- Did not purchase and re-sell any nursery stock.

27. This is a summary of your total gross sales of nursery stock in 2018.

| Sales | |

|---|---|

| Total gross sales of stock grown by this nursery operation | |

| Total gross sales of stock purchased for resale | |

| Total sales of nursery stock |

28. Of the total gross sales [amount] reported, please provide the percentage breakdown of nursery stock sales across the following distribution channels.

Sales distribution of nursery stocks (total gross sales)

The sales of nursery stocks that the operation produced and purchased for immediate resales.

Please report the value of nursery stock sales in percentage (%). The sum of different markets should be equal to 100%.

| Percentage of total sales | |

|---|---|

| Sales to the public | |

| Sales to fruit growers | |

| Sales to landscape contractors | |

| Sales to garden centres | |

| Sales to mass merchandisers | |

| Sales to other growers | |

| Export sales made directly by your operation | |

| Sales to public agencies | |

| Sales through other channels | |

| Total sales of nursery products |

Labour

29. How many seasonal and permanent workers, paid or unpaid, were employed by your operation in 2018?

If you operate both a greenhouse and a nursery, please provide your greenhouse and nursery labour separately. If you do not track labour separately, please prove the total in the third column.

Include all workers involved in growing, maintaining and harvesting on your operation, including the owners, family workers and foreign and seasonal workers. There must be at least one employee reported.

Exclude labour for retail and clerical help, and contract work, e.g., truck driver or landscaper.

| Greenhouse employees | Nursery employees | Total employees | |

|---|---|---|---|

| Seasonal employees - employed for less than 8 months | |||

| Full-time and part-time permanent employees - employed for 8 months or more | |||

| Total number of employees |

30. Are any of the greenhouse and nursery employees on your payroll?

- Yes

- No, only unpaid family labour is involved

Operating expenses

31. In 2018 , what were your operating expenses?

Please provide your greenhouse and nursery expenses separately. If you do not track these expenses separately, please provide the total in the third column.

Growing on is a term used by operators when stock is cultivated in the greenhouse or the nursery for the purpose of growing it to greater proportions. The operators will plant a seed or seedling in their greenhouse and care for it, by maintaining it (transplanting, fertilizing, etc.) until it becomes a sellable product.

Exclude any plant materials you may have purchased from other growers for immediate resale from your own operation (please report these purchases in row c).

| Greenhouse expenses | Nursery expenses | Total expenses | |

|---|---|---|---|

| Plant material | |||

| Purchases of plant material for growing on Include flowers, cuttings, seedlings, seeds, bulbs, bedding plants, young trees or nursery stock. |

|||

| Percentage of a. purchased from within your province | |||

| Purchases of plant material for immediate resale | |||

| Total plant material purchases | |||

| Payroll | |||

|

Payroll

Exclude wages and benefits paid to employees who provide retail or clerical help, and contact work, e.g., truck driving or landscaping. |

|||

| Fuel expenses | |||

| Natural gas | |||

| Heating oil | |||

| Other types of heating fuel | |||

| Total fuel expenses | |||

| Other expenses | |||

| Electricity expenses Include fertilizer, peticicides, pollination, irrigation, containers, packaging, bioprograms, and growing mediums such as soil, peat moss, vermiculite, perlite, sand, Styrofoam and sawdust. |

|||

| Other crop expenses | |||

| Other operating expenses e.g., Interest, land taxes, insurance, advertising, repairs to farm buildings, machinery, agricultural equipment and vehicles, contract work, and telephone and telecommunications services. |

|||

| Total operating expenses |

Sod operations - area and sales

32. What was the total sod area grown in 2018 .

Sod is grass or turf, which has its roots intact at the time of sale. Sod is grown in field and sold as a single product.

Report all the area of land used for growing and maintaining sod.

Include any sod grown that was not intended for sale within the survey year (the past calendar year).

Conversions

- 1 arpent = 0.9986 acres

- 1 acre = 1.0014 arpent

- 1 acre = 0.41 hectares

- 1 hectare = 2.47 acres

- Area

Unit of measure

- acres

- hectares

- arpents

33. Of the total sod area, how much was grown for sale in 2018?

Report the area of sod intended to be sold within the survey year (the past calendar year).

The area of sod grown for sale may be less than or equal to the total area of sod reported in the previous question.

- Area

34. What were the total gross sales of sod grown on your operation in 2018?

Exclude revenue from laying sod or reselling sod purchased from others.

- Total gross sales

35. What were the total gross sales of sod purchased for immediate resale?

- Total gross sales

- Did not purchase and re-sell any sod.

Summary - total sales of sod

36. This is a summary of the total sales of sod in 2018.

| Sales | |

|---|---|

| Total gross sales of sod grown on your operation | |

| Total gross sales of sod purchased for immediate resale | |

| Total sales of sod |

Sod operations - labour

37. How many seasonal and permanent workers, paid or unpaid, were employed by your operation in 2018?

Include all workers in this operation involved in growing, maintaining and harvesting sod on your operation, including the owners, family workers and foreign and seasonal workers. There must be at least one employee reported.

Exclude all labour for retail and clerical help; laying sod; and contract work, e.g., truck driver or landscaper.

| Number of employees | |

|---|---|

| Seasonal employees - employed for less than 8 months | |

| Full-time and part-time permanent employees - employed for 8 months or more | |

| Total number of employees |

38. Are any of the employees reported in question 37 on your payroll?

- Yes

- No, only unpaid family labour is involved

Sod operations - expenses

39. Please provide your sod operating expenses in 2018.

| Sod operating expenses | |

|---|---|

| Purchases of sod for immediate resale | |

| Percentage of a. purchased from within your province | |

|

Payroll

Exclude wages and benefits paid to employees who provide retail or clerical help, and contact work, e.g., truck driving or landscaping or laying sod. |

|

| Other sod operating expenses Include fertilizer, peticicides, land taxes, interest, insurance, advertising, repairs, fuel, electricity, and telephone and telecommunications services. |

|

| Total sod operating expenses in 2018 |

Agricultural production

40. Which of the following agricultural products are currently being produced on this operation?

Select all that apply.

- Field crops

- Hay

- Summerfallow

- Potatoes

- Fruit, berries and nuts

- Vegetables

- Sod

- Nursery products

- Greenhouse products

- Cattle and calves

Include beef or dairy. - Pigs

- Sheep and lambs

- Mink

- Fox

- Hens and chickens

- Turkeys

- Maple taps

- Honey bees

- Mushrooms

- Other

- Specify agricultural products

- Not producing agricultural products

Area in crops

41. What area of this operation is used for the following crops?

Report the areas only once, even if used for more than one crop type.

Exclude land used by others.

| Area | Unit of measure | |

|---|---|---|

| Field crops | ||

| Hay | ||

| Summerfallow | ||

| Potatoes | ||

| Fruit, berries and nuts | ||

| Vegetables | ||

| Sod | ||

| Nursery products | ||

Unit of measure

|

||

Greenhouse area

42. What is the total area under glass, plastic or other protection used for growing plants?

- Total area

Unit of measure

- square feet

- square metres

Livestock (excluding birds)

43. How many of the following animals are on this operation?

Report all animals on this operation, regardless of ownership, including those that are boarded, custom-fed or fed under contract.

Include all animals kept by this operation, regardless of ownership, that are pastured on a community pasture, grazing co-op or public land.

Exclude animals owned but kept on a farm, ranch or feedlot operated by someone else.

| Number | |

|---|---|

| Cattle and calves | |

| Pigs | |

| Sheep and lambs | |

| Mink | |

| Fox |

Birds

44. How many of the following birds are on this operation?

Report all poultry on this operation, regardless of ownership, including those grown under contract.

Include poultry for sale and poultry for personal use.

Exclude poultry owned but kept on an operation operated by someone else.

| Number | |

|---|---|

| Hens and chickens | |

| Turkeys |

Maple taps

45. What was the total number of taps made on maple trees last spring?

- Total number of taps

Honey bees

46. How many live colonies ofhoney bees (used for honey production or pollination) are owned by this operation?

Include bees owned, regardless of location.

- Number of colonies

Mushrooms

47. What is the total mushroom growing area (standing footage) on this operation?

Include mushrooms grown using beds, trays, tunnels or logs.

- Total area

Unit of measure

- square feet

- square metres

Changes or events

1. Indicate any changes or events that affected the reported values for this business or organization compared with the last reporting period.

Select all that apply.

- Strike or lock-out

- Exchange rate impact

- Price changes in goods or services sold

- Contracting out

- Organizational change

- Price changes in labour or raw materials

- Natural disaster

- Recession

- Change in product line

- Sold business or business units

- Expansion

- New or lost contract

- Plant closures

- Acquisition of business or business units

- Other

- Specify the other changes or events

- No changes or events

Contact person

1. Statistics Canada may need to contact the person who completed this questionnaire for further information. Is Provided Given Names, Provided Family Name the best person to contact?

- Yes

- No

Who is the best person to contact about this questionnaire?

- First name

- Last name

- Title

- Email address

- Telephone number (including area code)

- Extension number (if applicable)

The maximum number of characters is 5. - Fax number (including area code)

Feedback

1. How long did it take to complete this questionnaire?

Include the time spent gathering the necessary information.

- Hours

- Minutes

2. Do you have any comments about this questionnaire?

Motor vehicles

Motor vehicles Transportation equipment

Transportation equipment

Access to health care

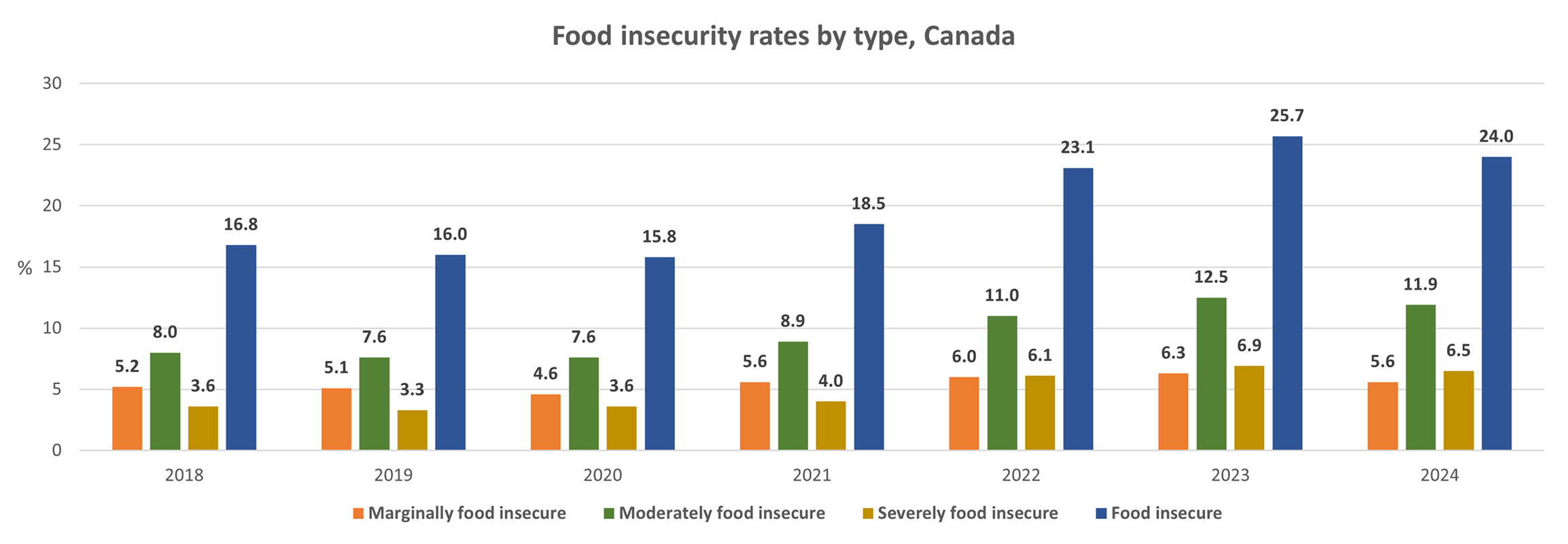

Access to health care Food insecurity

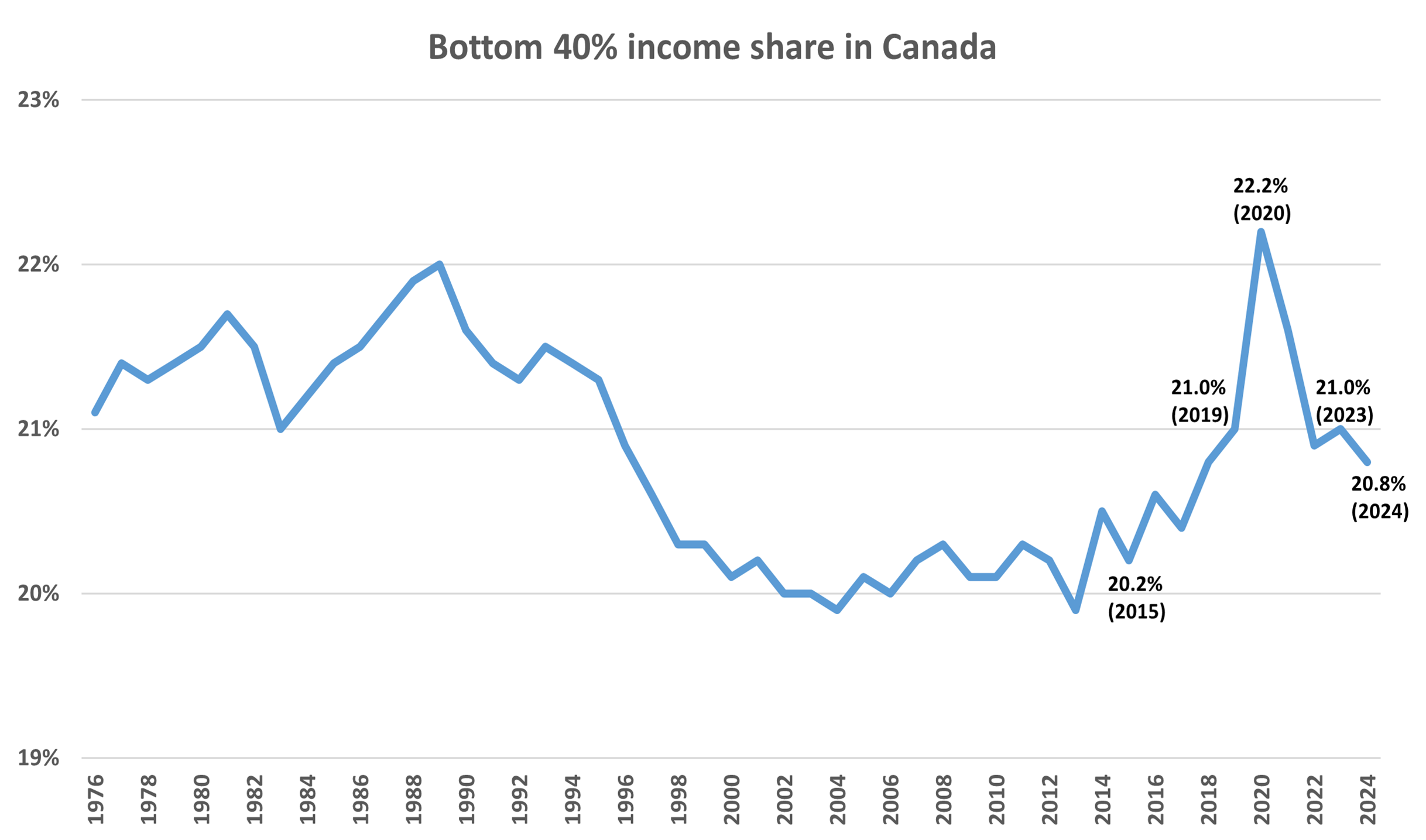

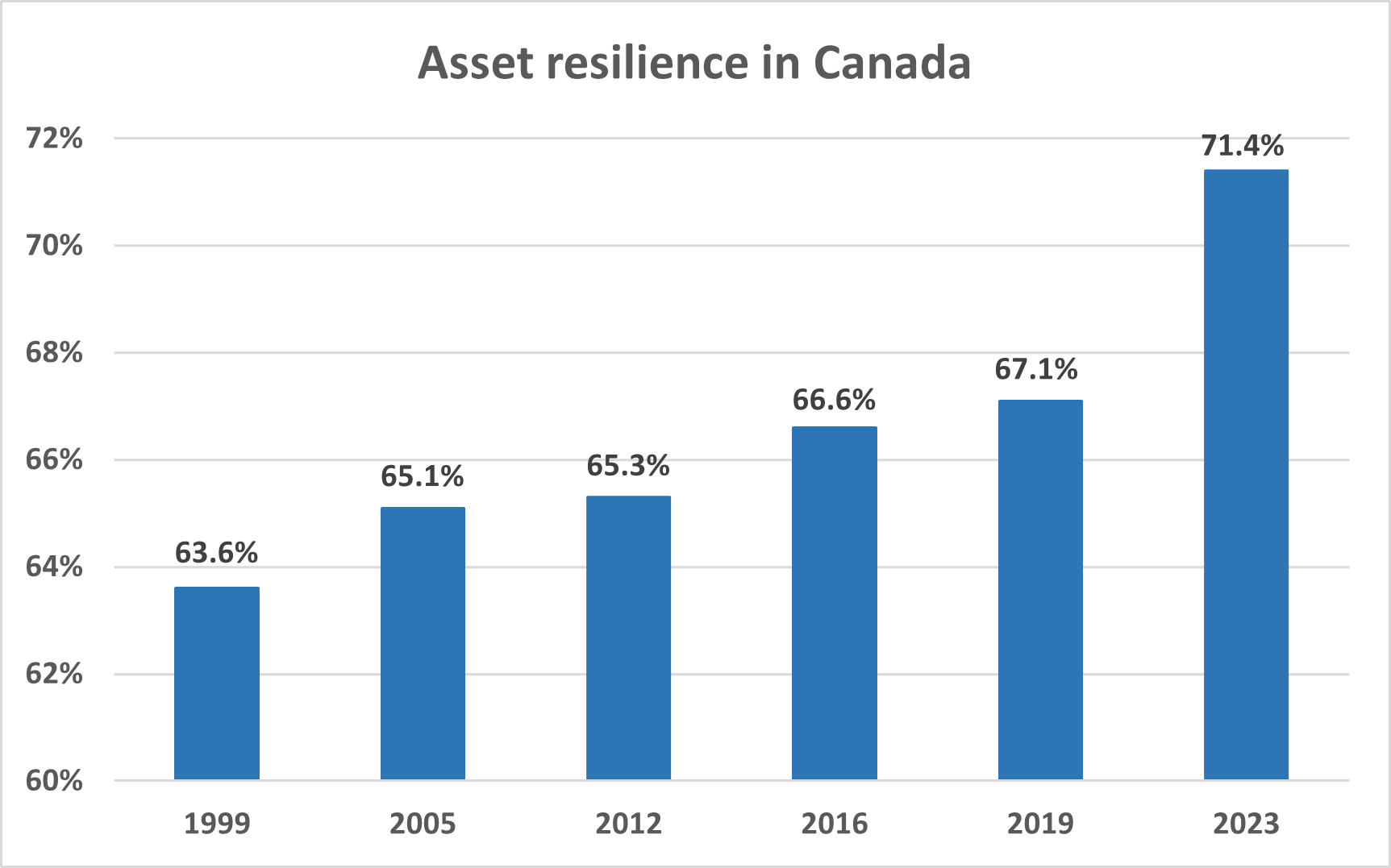

Food insecurity Income inequality

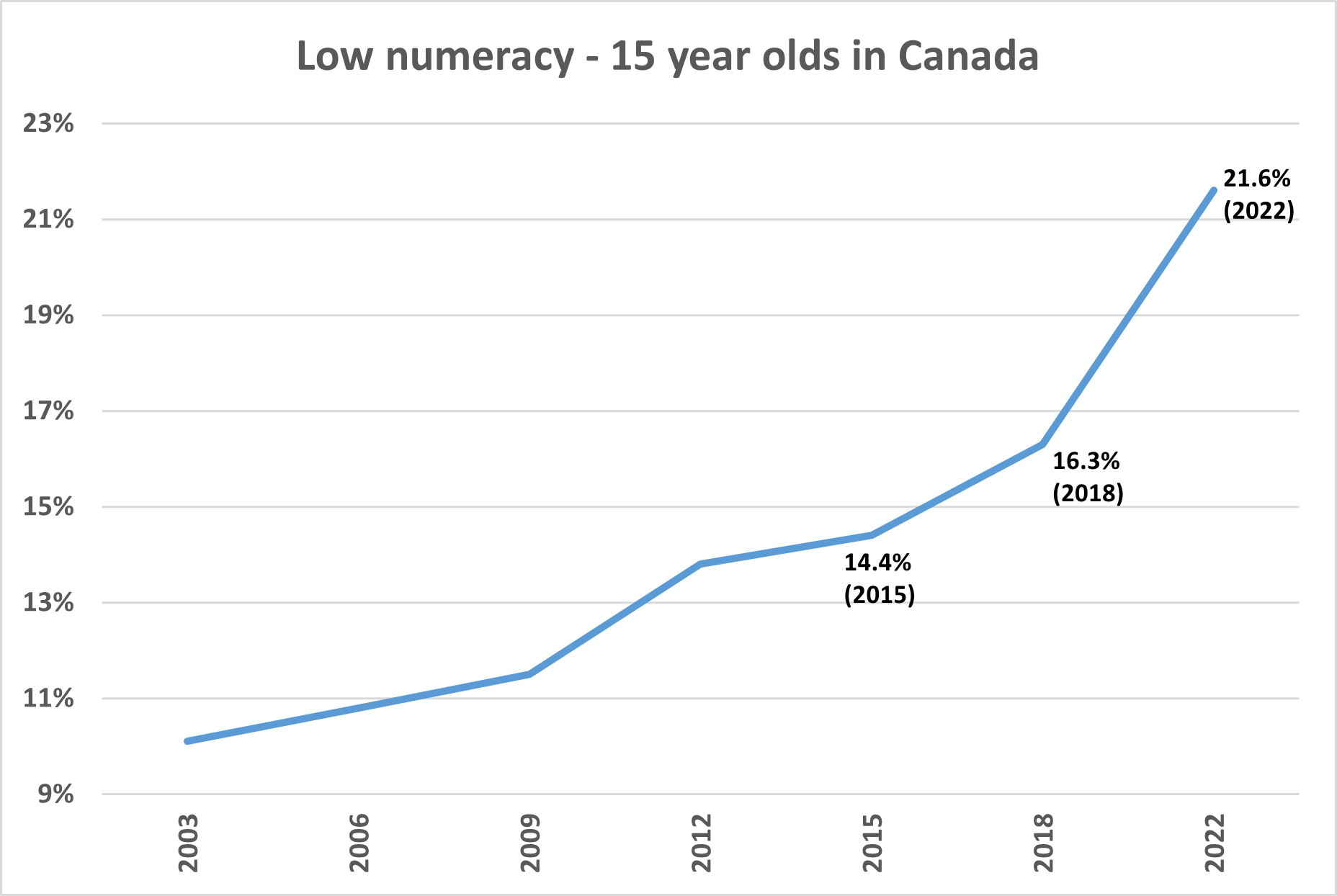

Income inequality Literacy

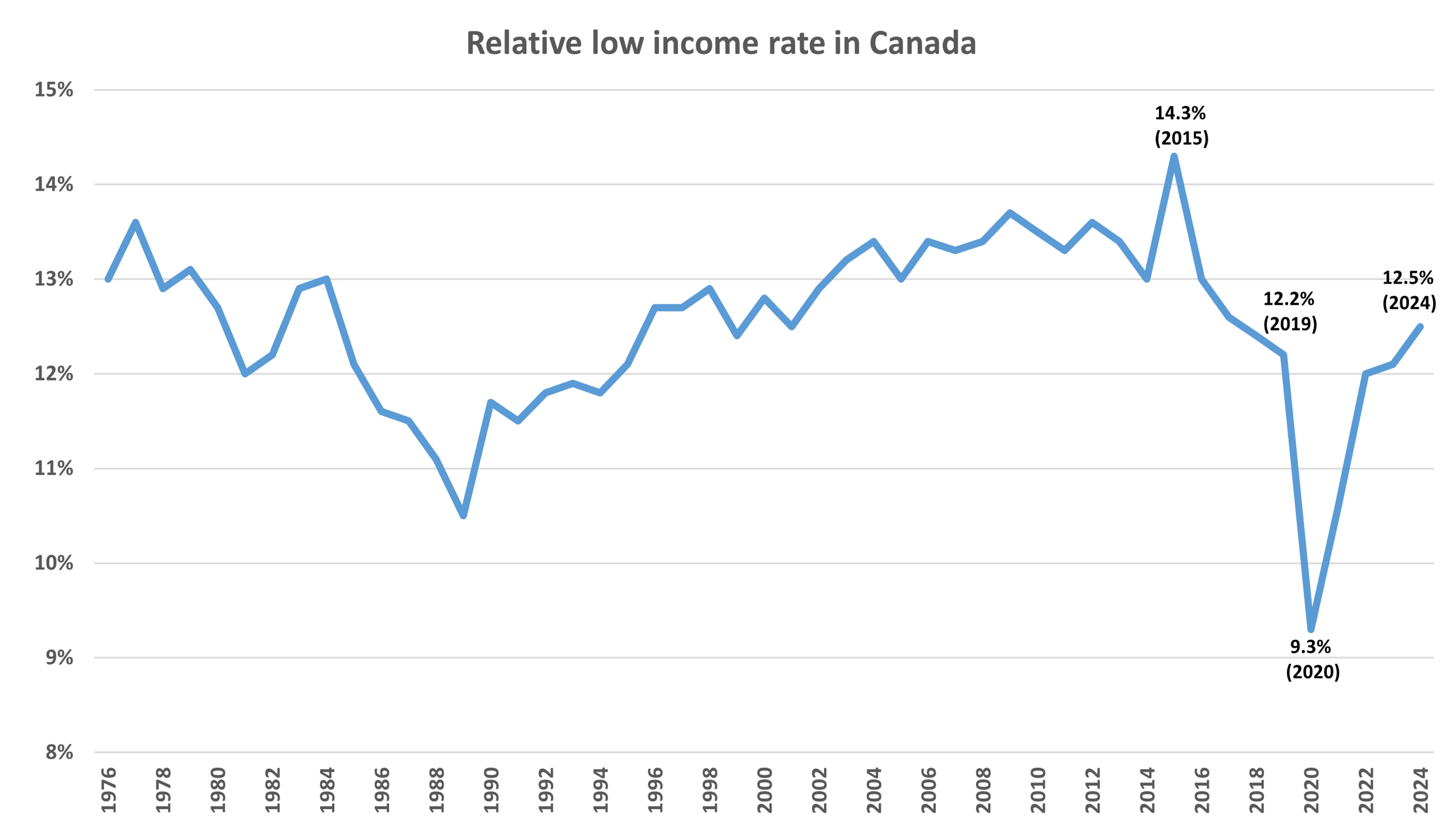

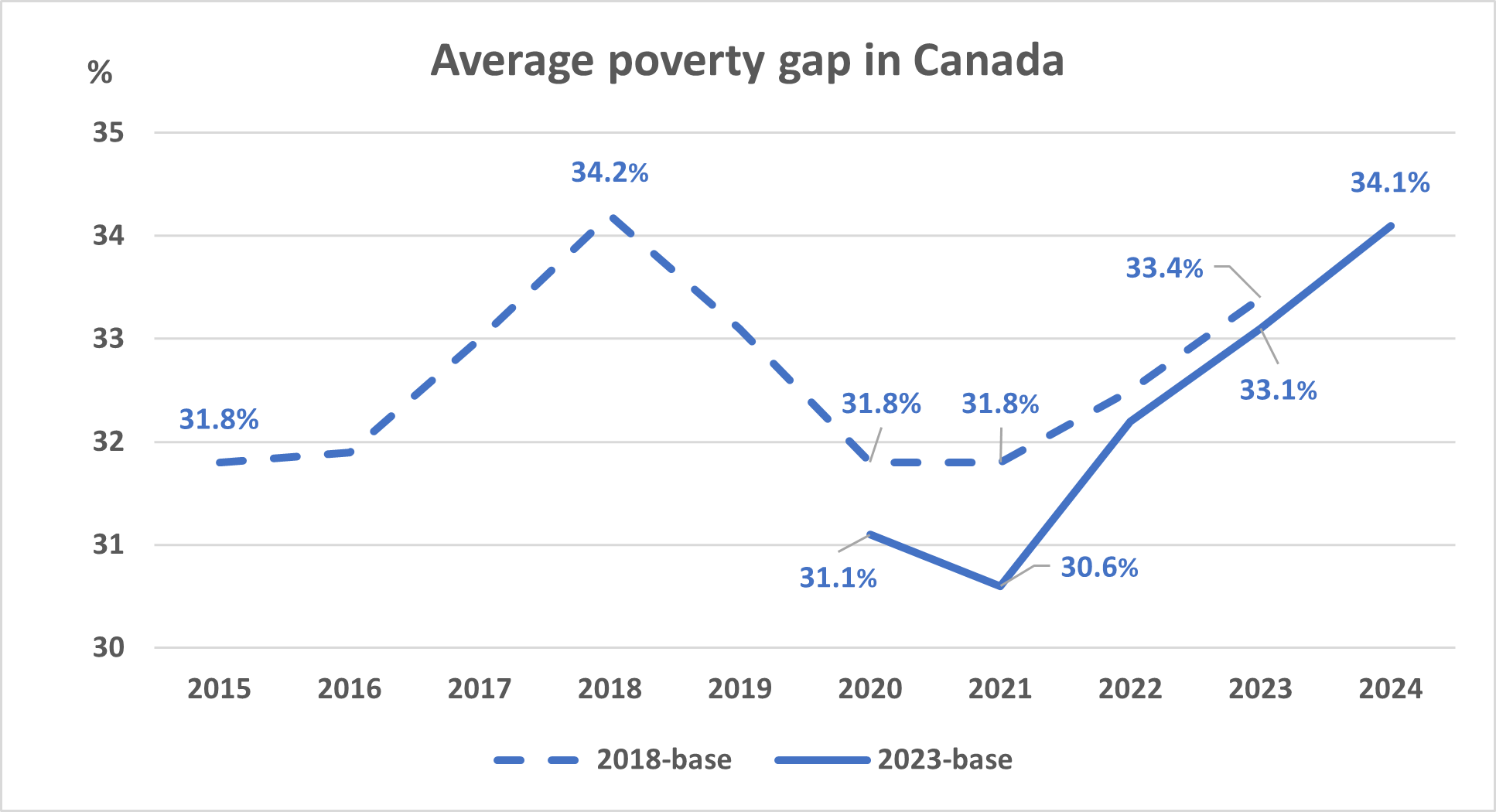

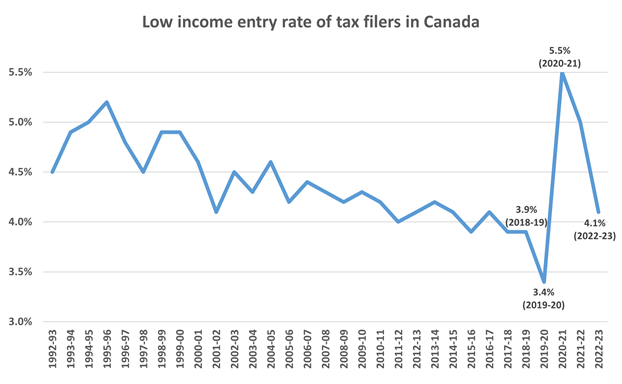

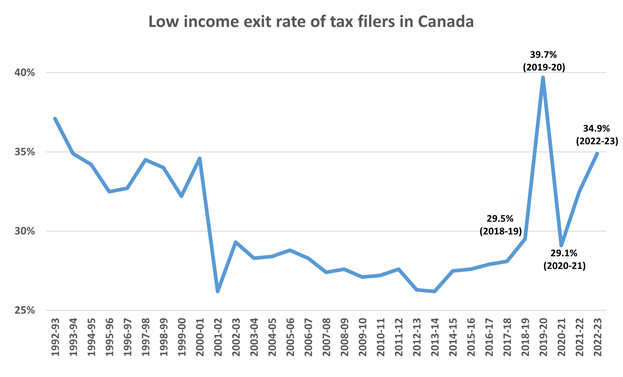

Literacy Low income

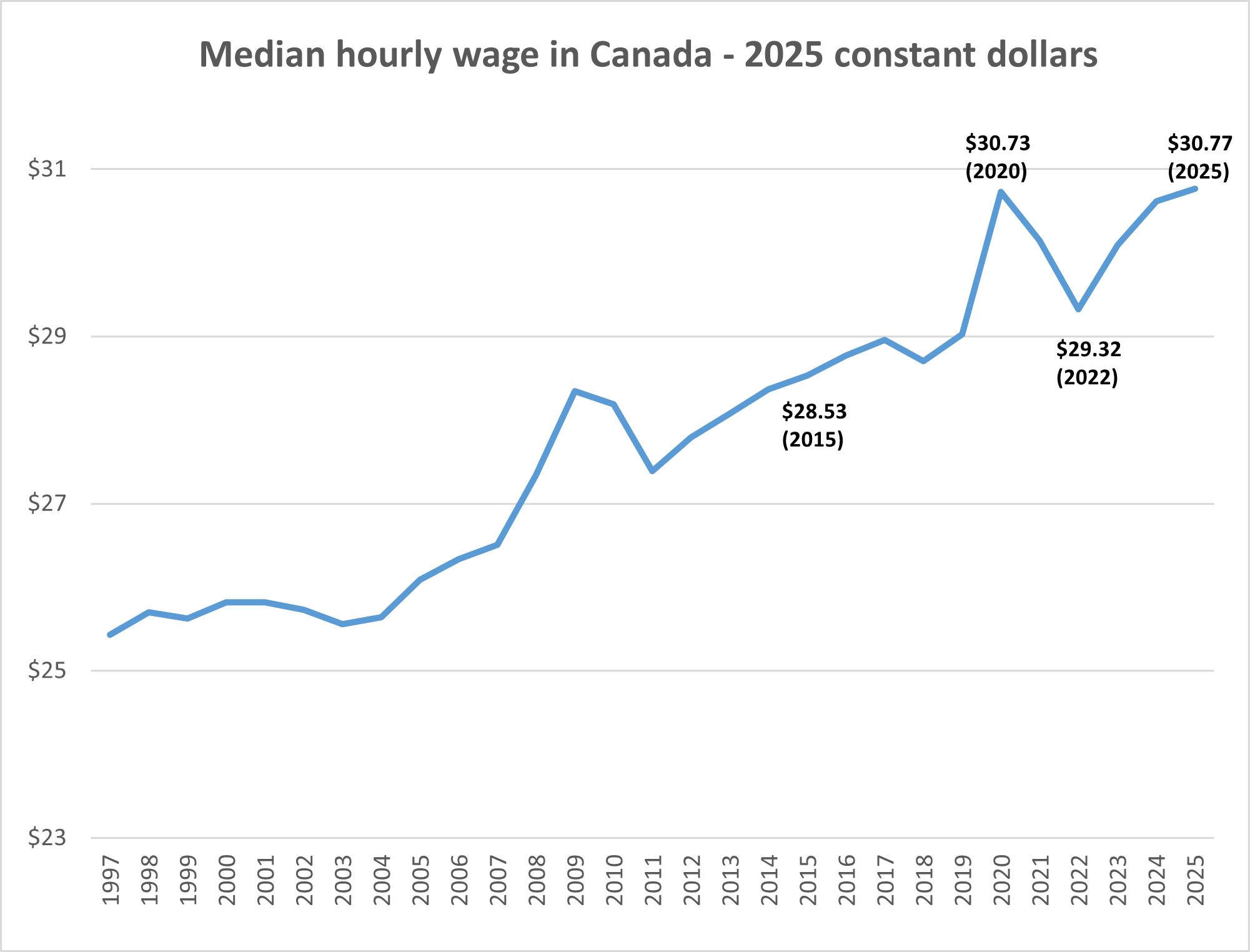

Low income Minimum wage or low-paid work

Minimum wage or low-paid work