Canada's exports over time: Resources and manufactured goods

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

International trade has played an integral role in Canada's economic history. Trade affects the economy in a myriad of ways—as a source of industrial production and income growth, and as a means through which Canadians gain access to foreign funds, investment goods, new technologies, and an ever-expanding array of products and services.

Exports in particular contribute substantially to economic growth in Canada. Canadian export flows have evolved over time as trade-oriented sectors responded to shifts in the global demand for Canadian commodities. Both resources and manufactured goods have been important to the development of Canadian export markets.

Exports in early Canada

For much of Canada's early history, merchandise exports served a growing international demand for resource-based staples, from agricultural and forestry products in the late 1800s to metals and minerals and processed resource products during the first half of the 20th century.

During the early part of Canada's history, exports reflected periods of resource-led growth. The growth was partly due to changes in global demand as new technologies made it more commercially viable to extract different commodities.

Since the country's centennial anniversary in 1967, Canadian merchandise exports have continued to evolve in response to notable changes in market conditions and regulatory regimes.

Growth of export-based manufacturing and resources since Canada's centennial

In the 30 years that followed the country's centennial, changes in the pace and composition of export growth largely reflected the development of Canada's export-oriented manufacturing sector.

During those years, new legislation on cross-border trade with the United States supported the growth in manufacturing exports. These included the introduction of the Canada‒United States Automotive Products Agreement in 1965, the implementation of the Canada‒United States Free Trade Agreement in 1989 and the implementation of the North American Free Trade Agreement in 1994.

In 2001, China joined the World Trade Organization. As manufacturing shifted to China and to other emerging economies, a global commodities boom occurred, strengthening the demand for oil and other primary commodities produced in Canada.

In the early 2000s, global oil prices began to increase sharply, while new advancements in extraction technologies made it more commercially viable to produce oil using non-conventional extraction methods, such as those used in western Canada's oil sands.

As a result, Canadian energy exports to the United States expanded rapidly, and energy became an important source of export growth. At the same time, exports of manufactured goods, particularly shipments of automotive products to the United States, slowed, as exporters diversified into other markets.

Growth in overall merchandise trade

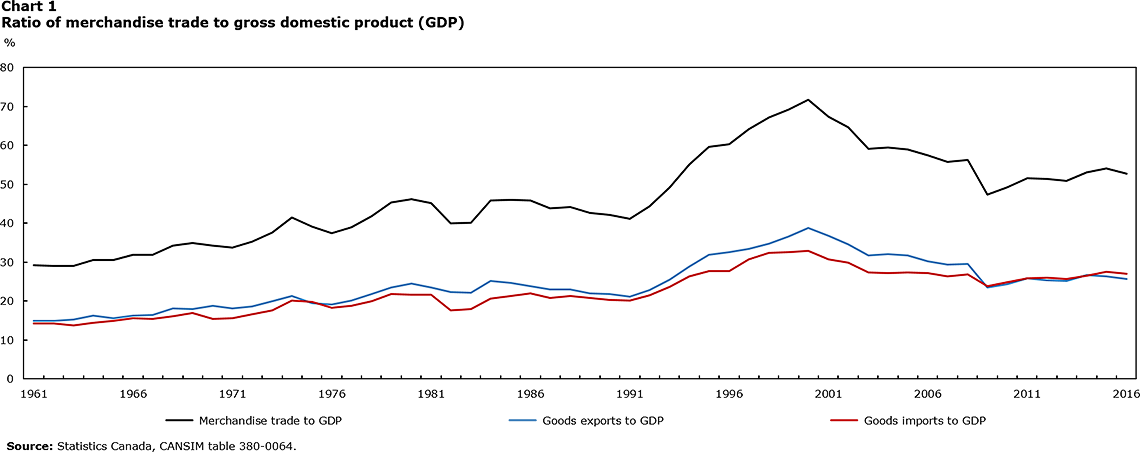

The importance of trade overall to Canada's economy has grown considerably over the last 50 years. At the time of Canada's centennial anniversary, the combined value of Canadian merchandise exports and imports amounted to about one-third of gross domestic product (GDP).

During the late 1960s and early 1970s, the ratio of trade to GDP edged higher as both exports and imports rose on higher shipments of manufactured and resource-based commodities. In particular, higher exports of industrial goods, machinery and equipment, agricultural products, and forestry products contributed to double-digit increases in annual exports during the early 1970s.

By the late 1970s, export growth was led by higher shipments of automotive products and industrial goods, as manufacturers of these and other durable manufacturing products expanded production.

Description: Chart 1 - Ratio of merchandise trade to gross domestic product (GDP)

| Year | Merchandise trade to GDP | Goods exports to GDP | Goods imports to GDP |

|---|---|---|---|

| 1961 | 29.2 | 14.9 | 14.2 |

| 1962 | 29.1 | 14.9 | 14.2 |

| 1963 | 29.0 | 15.2 | 13.8 |

| 1964 | 30.6 | 16.2 | 14.4 |

| 1965 | 30.5 | 15.5 | 15.0 |

| 1966 | 31.8 | 16.2 | 15.6 |

| 1967 | 31.9 | 16.5 | 15.5 |

| 1968 | 34.2 | 18.1 | 16.2 |

| 1969 | 34.8 | 18.0 | 16.9 |

| 1970 | 34.3 | 18.8 | 15.4 |

| 1971 | 33.7 | 18.1 | 15.6 |

| 1972 | 35.2 | 18.5 | 16.7 |

| 1973 | 37.7 | 20.0 | 17.6 |

| 1974 | 41.5 | 21.3 | 20.2 |

| 1975 | 39.1 | 19.4 | 19.7 |

| 1976 | 37.4 | 19.1 | 18.3 |

| 1977 | 38.9 | 20.1 | 18.8 |

| 1978 | 41.8 | 21.8 | 20.0 |

| 1979 | 45.3 | 23.4 | 21.8 |

| 1980 | 46.2 | 24.6 | 21.7 |

| 1981 | 45.2 | 23.5 | 21.7 |

| 1982 | 40.0 | 22.4 | 17.6 |

| 1983 | 40.1 | 22.1 | 18.0 |

| 1984 | 45.8 | 25.1 | 20.7 |

| 1985 | 46.0 | 24.6 | 21.4 |

| 1986 | 45.8 | 23.8 | 21.9 |

| 1987 | 43.8 | 22.9 | 20.8 |

| 1988 | 44.2 | 22.9 | 21.3 |

| 1989 | 42.7 | 21.9 | 20.8 |

| 1990 | 42.2 | 21.9 | 20.3 |

| 1991 | 41.1 | 21.1 | 20.1 |

| 1992 | 44.3 | 22.8 | 21.5 |

| 1993 | 49.2 | 25.5 | 23.7 |

| 1994 | 55.1 | 28.8 | 26.3 |

| 1995 | 59.6 | 31.9 | 27.7 |

| 1996 | 60.3 | 32.6 | 27.7 |

| 1997 | 64.2 | 33.5 | 30.7 |

| 1998 | 67.1 | 34.8 | 32.3 |

| 1999 | 69.1 | 36.6 | 32.5 |

| 2000 | 71.7 | 38.8 | 32.8 |

| 2001 | 67.4 | 36.7 | 30.7 |

| 2002 | 64.6 | 34.6 | 30.0 |

| 2003 | 59.2 | 31.8 | 27.4 |

| 2004 | 59.4 | 32.1 | 27.3 |

| 2005 | 59.0 | 31.6 | 27.3 |

| 2006 | 57.4 | 30.3 | 27.1 |

| 2007 | 55.7 | 29.3 | 26.4 |

| 2008 | 56.3 | 29.5 | 26.8 |

| 2009 | 47.3 | 23.4 | 23.9 |

| 2010 | 49.2 | 24.3 | 24.9 |

| 2011 | 51.6 | 25.8 | 25.8 |

| 2012 | 51.4 | 25.3 | 26.0 |

| 2013 | 50.9 | 25.3 | 25.7 |

| 2014 | 53.1 | 26.6 | 26.5 |

| 2015 | 54.0 | 26.4 | 27.6 |

| 2016 | 52.7 | 25.7 | 27.0 |

| Source: Statistics Canada, CANSIM table 380-0064. | |||

During the 1980s, the ratio of merchandise trade to output averaged 44%, as exports of manufactured products continued to expand. Large annual increases in automotive exports fuelled export growth as automotive production, supported by the Canada‒United States Automotive Products Agreement, rose significantly early in the decade. Higher shipments of forestry products contributed to export growth late in the 1980s.

Acceleration of export growth under free trade agreements

The 1990s witnessed a sharp increase in the value of trade as firms in Canada adjusted to the implementation of the Canada‒United States Free Trade Agreement in 1989 and the North American Free Trade Agreement in 1994. Following the recession in the early 1990s, current-dollar exports rose, on average, by over 10% annually throughout the rest of the decade, led in large part by higher shipments of motor vehicles and parts. Higher shipments of forestry products also supported export growth early in the decade. Shipments of electronics and electrical equipment bolstered exports toward the end of the 1990s, as manufacturers of information and communications technologies expanded output.

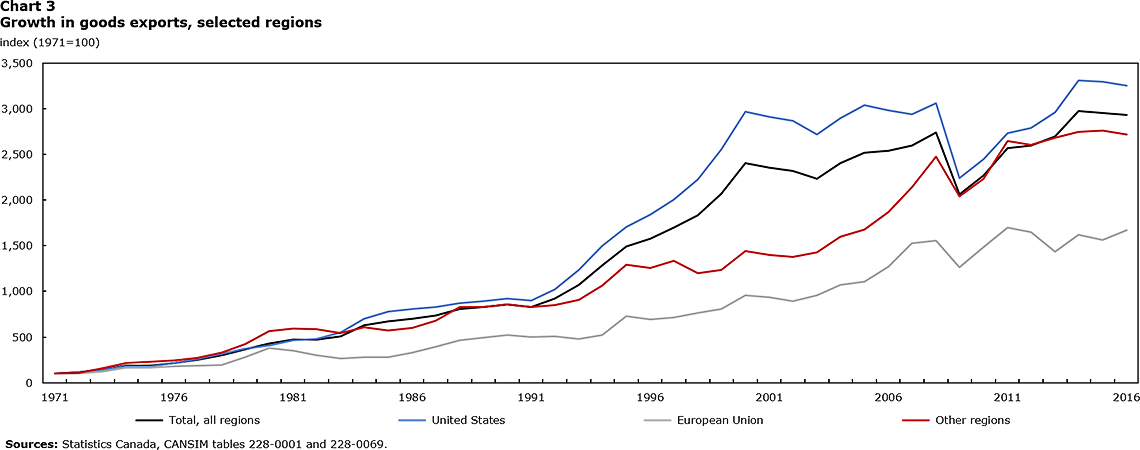

Much of the export growth during this period reflected a deepening of trade ties with the United States. Between the early 1990s and the early 2000s, the share of Canadian exports going to the United States rose by about 10 percentage points, peaking at 84% in 2002. Shipments to the European Union in that year accounted for 5% of total exports, as did combined shipments to China, Mexico and Japan.

By the end of the 1990s, the ratio of total trade to GDP had risen to about 70%. Throughout the 1990s, export flows, measured in volume terms, made notable contributions to economic growth, often exceeding those from higher household spending and business investment.

Description: Chart 2 - Goods exports, selected commodities

| Year | All products | Energy products | Forestry products and building and packaging materials | Motor vehicles and parts | Other non-energy products |

|---|---|---|---|---|---|

| 1971 | 18.4 | 1.3 | 3.0 | 4.2 | 9.9 |

| 1972 | 21.0 | 1.7 | 3.6 | 4.7 | 11.0 |

| 1973 | 26.5 | 2.5 | 4.6 | 5.4 | 14.1 |

| 1974 | 33.5 | 5.2 | 5.6 | 5.7 | 17.1 |

| 1975 | 34.4 | 5.3 | 5.1 | 6.4 | 17.6 |

| 1976 | 39.1 | 5.0 | 6.5 | 8.2 | 19.5 |

| 1977 | 45.6 | 5.4 | 7.9 | 10.3 | 22.0 |

| 1978 | 54.7 | 5.9 | 9.6 | 12.4 | 26.8 |

| 1979 | 67.1 | 8.9 | 11.7 | 11.8 | 34.7 |

| 1980 | 79.0 | 10.7 | 12.3 | 10.9 | 45.1 |

| 1981 | 86.1 | 10.2 | 12.7 | 15.6 | 47.5 |

| 1982 | 86.6 | 11.1 | 11.7 | 18.7 | 45.1 |

| 1983 | 92.8 | 11.2 | 12.6 | 23.4 | 45.6 |

| 1984 | 115.5 | 12.5 | 15.1 | 32.1 | 55.8 |

| 1985 | 122.7 | 14.2 | 15.8 | 35.9 | 56.8 |

| 1986 | 125.0 | 9.7 | 18.2 | 34.9 | 62.2 |

| 1987 | 131.2 | 11.4 | 21.2 | 34.9 | 63.8 |

| 1988 | 143.3 | 12.4 | 23.2 | 34.7 | 72.9 |

| 1989 | 146.7 | 13.3 | 23.0 | 34.1 | 76.3 |

| 1990 | 151.8 | 13.6 | 22.0 | 35.6 | 80.6 |

| 1991 | 147.3 | 13.7 | 20.2 | 33.6 | 79.8 |

| 1992 | 163.0 | 15.1 | 21.9 | 39.3 | 86.6 |

| 1993 | 189.6 | 17.3 | 25.8 | 49.8 | 96.8 |

| 1994 | 227.6 | 18.7 | 32.5 | 58.8 | 117.6 |

| 1995 | 264.7 | 19.9 | 40.8 | 64.0 | 140.1 |

| 1996 | 279.3 | 25.4 | 39.5 | 64.4 | 150.0 |

| 1997 | 302.5 | 26.4 | 41.0 | 70.7 | 164.5 |

| 1998 | 326.3 | 23.0 | 42.5 | 80.2 | 180.6 |

| 1999 | 367.9 | 29.0 | 48.4 | 99.4 | 191.1 |

| 2000 | 428.0 | 51.9 | 52.5 | 100.5 | 223.1 |

| 2001 | 419.1 | 54.4 | 50.7 | 95.3 | 218.7 |

| 2002 | 412.1 | 47.8 | 48.1 | 99.4 | 216.8 |

| 2003 | 397.3 | 58.9 | 44.8 | 89.1 | 204.4 |

| 2004 | 427.2 | 66.0 | 50.1 | 91.5 | 219.6 |

| 2005 | 448.4 | 84.9 | 47.3 | 88.3 | 228.0 |

| 2006 | 452.0 | 81.5 | 44.6 | 82.7 | 243.1 |

| 2007 | 461.4 | 85.2 | 40.0 | 77.6 | 258.7 |

| 2008 | 487.3 | 118.0 | 35.5 | 61.3 | 272.5 |

| 2009 | 367.2 | 74.4 | 27.5 | 44.2 | 221.1 |

| 2010 | 404.0 | 83.6 | 29.4 | 57.4 | 233.6 |

| 2011 | 456.6 | 103.7 | 30.4 | 59.6 | 262.9 |

| 2012 | 461.5 | 103.7 | 30.6 | 68.5 | 258.7 |

| 2013 | 479.2 | 113.9 | 33.4 | 68.2 | 263.7 |

| 2014 | 528.4 | 128.7 | 36.6 | 74.6 | 288.5 |

| 2015 | 524.9 | 83.8 | 39.6 | 87.3 | 314.2 |

| 2016 | 521.3 | 71.6 | 41.3 | 95.6 | 312.7 |

| Sources: Statistics Canada, CANSIM tables 376-0006 and 376-0107. | |||||

Description: Chart 3 - Growth in goods exports, selected regions

| Year | Total, all regions | United States | European Union | Other regions |

|---|---|---|---|---|

| 1971 | 100.0 | 100.0 | 100.0 | 100.0 |

| 1972 | 113.7 | 117.7 | 100.5 | 109.1 |

| 1973 | 144.2 | 145.2 | 125.0 | 155.6 |

| 1974 | 184.1 | 180.7 | 163.1 | 213.5 |

| 1975 | 189.0 | 182.8 | 167.6 | 229.2 |

| 1976 | 214.6 | 213.9 | 177.9 | 246.0 |

| 1977 | 250.2 | 258.6 | 184.2 | 270.6 |

| 1978 | 300.1 | 313.4 | 196.0 | 331.5 |

| 1979 | 368.8 | 373.6 | 279.7 | 420.3 |

| 1980 | 431.2 | 405.9 | 378.7 | 567.6 |

| 1981 | 474.8 | 467.9 | 352.2 | 596.7 |

| 1982 | 474.6 | 481.5 | 298.8 | 586.3 |

| 1983 | 509.2 | 550.2 | 268.6 | 543.6 |

| 1984 | 626.1 | 702.9 | 282.5 | 605.9 |

| 1985 | 669.5 | 777.4 | 276.3 | 571.9 |

| 1986 | 703.9 | 809.3 | 330.0 | 600.2 |

| 1987 | 739.4 | 826.8 | 392.4 | 682.2 |

| 1988 | 807.2 | 872.7 | 466.0 | 828.0 |

| 1989 | 826.4 | 895.3 | 495.0 | 827.0 |

| 1990 | 855.1 | 924.6 | 522.4 | 853.9 |

| 1991 | 830.4 | 900.2 | 500.9 | 826.0 |

| 1992 | 919.2 | 1,022.5 | 508.5 | 852.2 |

| 1993 | 1,069.7 | 1,235.7 | 478.0 | 908.2 |

| 1994 | 1,283.1 | 1,500.5 | 519.0 | 1,063.4 |

| 1995 | 1,492.1 | 1,704.8 | 726.6 | 1,291.5 |

| 1996 | 1,575.0 | 1,843.7 | 692.7 | 1,254.9 |

| 1997 | 1,701.3 | 2,003.8 | 713.5 | 1,337.1 |

| 1998 | 1,834.9 | 2,225.8 | 767.4 | 1,200.2 |

| 1999 | 2,068.7 | 2,553.2 | 809.4 | 1,231.9 |

| 2000 | 2,406.9 | 2,965.4 | 956.4 | 1,441.1 |

| 2001 | 2,356.8 | 2,906.7 | 937.2 | 1,399.4 |

| 2002 | 2,317.6 | 2,864.2 | 890.8 | 1,377.8 |

| 2003 | 2,234.1 | 2,715.2 | 954.9 | 1,425.5 |

| 2004 | 2,402.6 | 2,893.8 | 1,072.0 | 1,596.2 |

| 2005 | 2,521.7 | 3,041.3 | 1,106.7 | 1,674.4 |

| 2006 | 2,541.7 | 2,984.1 | 1,270.9 | 1,871.9 |

| 2007 | 2,594.6 | 2,938.2 | 1,525.5 | 2,139.1 |

| 2008 | 2,740.1 | 3,057.4 | 1,555.1 | 2,474.3 |

| 2009 | 2,065.0 | 2,238.6 | 1,260.5 | 2,042.1 |

| 2010 | 2,271.7 | 2,445.9 | 1,481.0 | 2,235.7 |

| 2011 | 2,567.8 | 2,728.9 | 1,696.8 | 2,643.6 |

| 2012 | 2,595.3 | 2,789.7 | 1,647.9 | 2,606.0 |

| 2013 | 2,694.9 | 2,961.8 | 1,433.7 | 2,678.8 |

| 2014 | 2,971.5 | 3,312.7 | 1,617.5 | 2,748.2 |

| 2015 | 2,952.0 | 3,292.1 | 1,560.9 | 2,761.9 |

| 2016 | 2,931.7 | 3,251.2 | 1,666.9 | 2,720.2 |

| Sources: Statistics Canada, CANSIM tables 228-0001 and 228-0069. | ||||

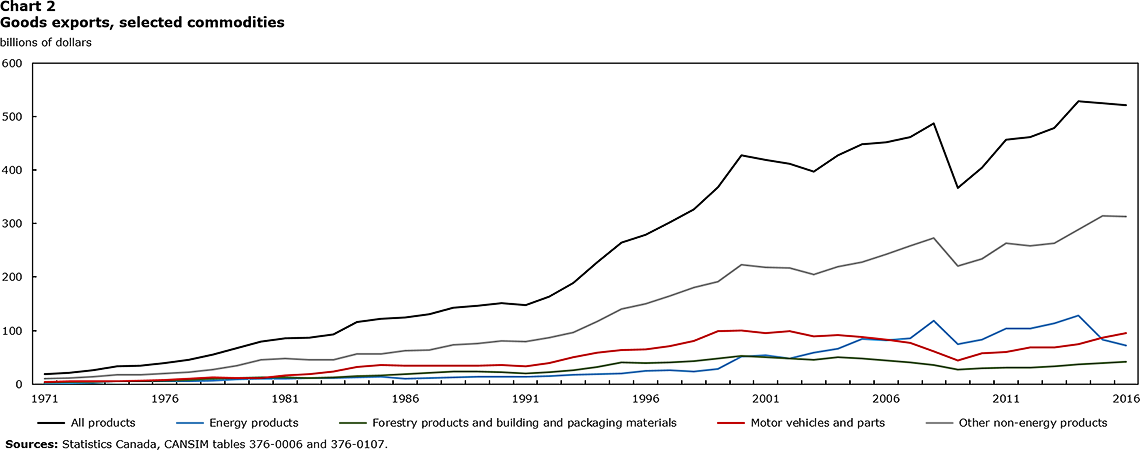

Export growth since 2000: Energy offsets declines in autos

At the start of the 2000s, manufactured products accounted for almost three-quarters of total exports. At that time, shipments of motor vehicles and auto parts represented nearly a quarter of export earnings. In contrast, shipments of energy products—crude oil and crude bitumen, natural gas and refined petroleum products—accounted for 12% of total exports.

Since 2000, the composition of exports has shifted significantly, most notably as a result of changes in relative earnings from automotive and energy products. These shifts were well underway prior to the 2008‒2009 recession. Exports of motor vehicles and parts declined markedly from 2005 to 2008, as the share of U.S. auto imports from Canadian producers fell.

Annual auto exports totalled about $60 billion in 2008, down 40% from levels in 2000, while the share of export receipts from automotive products fell from 24% to 13%. Exports of forestry products and electronics and electrical equipment—strong contributors to export growth during previous decades—also declined during this period.

Decreases in shipments of manufactured products to the United States contributed to overall reductions in the intensity of trade. From 2000 to 2008, the ratio of merchandise trade to total output trended lower, falling to levels last observed in the mid-1990s prior to the sharp acceleration in trade flows during that decade.

While manufacturing exports to the United States declined during the 2000s, the export of manufactured goods to non-US markets rose, notably to the European Union and China. By 2008, exports to the European Union, led by shipments to the United Kingdom, accounted for 8% of total exports, while exports to China represented just over 2% of total shipments.

While lower automotive shipments to the United States slowed export growth during the early 2000s, the value of energy exports increased. Supported by higher prices and volumes, oil exports rose from $18.6 billion in 2002 to $61.0 billion in 2008. Total receipts from energy products in that year, which include earnings from crude oil, natural gas and refined petroleum products, accounted for 24% of export earnings. Virtually all of these energy exports were to the United States.

Economic developments since the 2008‒2009 recession have moderated the shift from auto exports to energy. Automotive shipments have risen substantially since the recession. In 2016, annual exports of motor vehicles and parts reached $96 billion, the highest level since 2002, on higher shipments of passenger cars and light trucks.

While exports of crude oil also increased after the recession, the decline in oil prices that began in mid-2014 markedly reduced export earnings from energy products. In 2015, annual receipts from automotive exports eclipsed those from energy products for the first time since 2006.

Other non-energy exports have also recorded notable gains in recent years, as shipments of food products and pharmaceuticals, building and packaging materials, and communications equipment all expanded.

Much of the overall growth in exports following the 2008‒2009 recession has reflected higher shipments to the United States, the United Kingdom and non-EU countries, most notably China. In 2016, exports to China totalled $22.4 billion, about one-half of the value of Canada's exports to the European Union.

References

Baldwin, J.R. and R. Macdonald. 2012. "Natural Resources, the Terms of Trade, and Real Income Growth in Canada: 1870 to 2010." Economic Analysis Research Paper Series, no. 79, Statistics Canada catalogue no. F110027M.

Baldwin, J.R., and B. Yan. "Export Market Dynamics and Plant-level Productivity: Impact of Tariff Reductions and Exchange Rate Cycles." Economic Analysis Research Paper Series, no. 63, Statistics Canada catalogue no. F110027M.

Bank of Canada. 2015. Drilling Down ‒ Understanding Oil Prices and Their Economic Impact. Remarks by Timothy Lane at the Madison International Trade Association meetings.

Carrière, B. 2014. "2002-2012: A Decade of Change in Canadian Manufacturing Exports." Analysis in Brief, no. 92, Statistics Canada catalogue no. 11-621-M.

Cross, P. and D. Wyman. 2006. "The changing composition of the merchandise trade surplus." Canadian Economic Observer, November 2006, Statistics Canada catalogue no. 11-010-X.

Contact information

To enquire about the concepts, methods or data quality of this release, contact Guy Gellatly (guy.gellatly@canada.ca; 613-415-6894), Analysis Studies Branch.

- Date modified: