Retail Commodity Survey: CVs for Total Sales March 2024

Table summary

This table displays the results of Retail Commodity Survey: CVs for Total Sales (March 2024). The information is grouped by NAPCS-CANADA (appearing as row headers), and Month (appearing as column headers).

NAPCS-CANADA

Month

202312

202401

202402

202403

Total commodities, retail trade commissions and miscellaneous services

0.50

0.70

0.66

0.59

Retail Services (except commissions) [561]

0.49

0.69

0.65

0.59

Food and beverages at retail [56111]

0.41

0.48

0.43

0.43

Cannabis products, at retail [56113]

0.00

0.00

0.00

0.00

Clothing at retail [56121]

1.24

0.76

0.85

0.98

Jewellery and watches, luggage and briefcases, at retail [56123]

3.49

2.01

2.46

2.03

Footwear at retail [56124]

0.99

1.26

1.08

1.30

Home furniture, furnishings, housewares, appliances and electronics, at retail [56131]

0.80

0.91

0.86

0.88

Sporting and leisure products (except publications, audio and video recordings, and game software), at retail [56141]

1.77

2.53

2.81

2.48

Publications at retail [56142]

5.29

5.34

7.39

7.17

Audio and video recordings, and game software, at retail [56143]

3.91

4.06

3.80

3.90

Motor vehicles at retail [56151]

1.85

2.48

2.24

1.85

Recreational vehicles at retail [56152]

5.15

5.24

4.89

4.64

Motor vehicle parts, accessories and supplies, at retail [56153]

1.35

2.50

1.89

1.66

Automotive and household fuels, at retail [56161]

1.71

1.65

1.54

1.68

Home health products at retail [56171]

3.06

3.32

3.27

3.38

Infant care, personal and beauty products, at retail [56172]

2.83

2.92

2.80

2.80

Hardware, tools, renovation and lawn and garden products, at retail [56181]

By Steve Matthews, Kyle Virgin and Ramdane Djoudad—Statistics Canada

This special-edition article provides nontechnical answers to questions related to the production, use and interpretation of advance indicators for Statistics Canada's Monthly Survey of Manufacturing, Monthly Wholesale Trade Survey and Monthly Retail Trade Survey. Organized as a set of frequently asked questions, this reference document complements the technical documentation on definitions, data sources and methods available for individual programs. It is composed of two sections. Section 1 reviews concepts and definitions that are central to the production of advance indicators, while Section 2 relates to the analysis and interpretation of these special statistical products.

Section 1: Context, definitions and terminology

1 What is an advance indicator?

Advance indicators are statistical estimates designed to provide early information on economic activities for a given reference period. For the surveys listed above, advance indicators are generated when information for a portion of respondents has been received but data collection is still underway. Advance indicators for monthly manufacturing, wholesale trade and retail trade are typically published 21 to 25 days after the end of a reference month, while preliminary indicators are published approximately one month later. For example, the monthly retail advance indicator for the January reference month would be published in February (21 to 25 days after), while the preliminary indicator for January would be published in March (one month later). Therefore, a February publication would showcase a preliminary indicator for December, as well as an advance indicator for January.

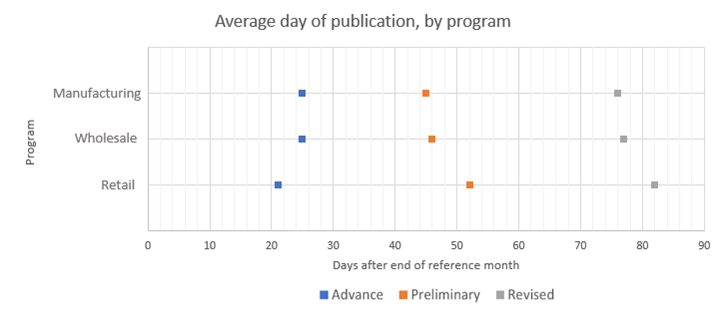

Chart 1 shows the average number of days to publish advance, preliminary and revised indicators for the three programs following the end of the reference month.

Chart 1 - Average day of publication, by program

Description - Average day of publication, by program

Average day of publication, by program

Program

Advance

Preliminary

Revised

Manufacturing

25

45

76

Wholesale

25

46

77

Retail

21

52

82

2 What led Statistics Canada to publish advance indicators?

Statistics Canada first published advance indicators in 2020. This work was done primarily to provide users with more timely information, given the economic uncertainty that arose from the COVID-19 pandemic. Demand was high for advance indicators to monitor the economic impacts of COVID-19 in different areas of the Canadian economy and to provide early signals and information about the direction of trends. By using early respondent data, Statistics Canada was able to compile timely and reliable economic signals based on observed data.

Reference month of first release of advance indicator

Program

Reference month of first release of advance indicator

Monthly Retail Trade Survey

April 2020

Monthly Survey of Manufacturing

May 2020

Monthly Wholesale Trade Survey

August 2020

3 How does Statistics Canada produce advance indicators?

Statistics Canada uses a technique called flash estimation to produce advance indicators for selected survey programs. Flash estimation refers to a type of advance indicator that uses the same methods used to produce preliminary indicators, but these methods are applied to a more limited dataset, at an earlier point in time. For example, to produce the advance retail trade indicator, only responses that have been received by a predetermined point in the collection period are used. Once collection is complete, the same non-response treatments and weighting methods are used on the full set of received data, which is then used to produce the preliminary indicator.

The amount of collected data incorporated into an advance indicator varies from month to month and across surveys. Table 1 shows that in 2023, the average response rates for advance indicators (rounded to the nearest percentage point) were 68% for the Monthly Survey of Manufacturing, 59% for the Monthly Wholesale Trade Survey and 45% for the Monthly Retail Trade Survey. These response rates are typically published along with each advance indicator to provide users with information on the quality of that month's figure.

Table 1 - Average response rates, 2023

Program

Advance indicator

Preliminary indicator

Revised indicator

Manufacturing

68%

87%

94%

Wholesale trade

59%

69%

75%

Retail trade

45%

83%

88%

The monthly gross domestic product (GDP) by industry program uses the advance indicators discussed in this article to compile its own advance indicators of GDP. More information on estimates of monthly GDP can be found in Revisions to Canada's GDP.

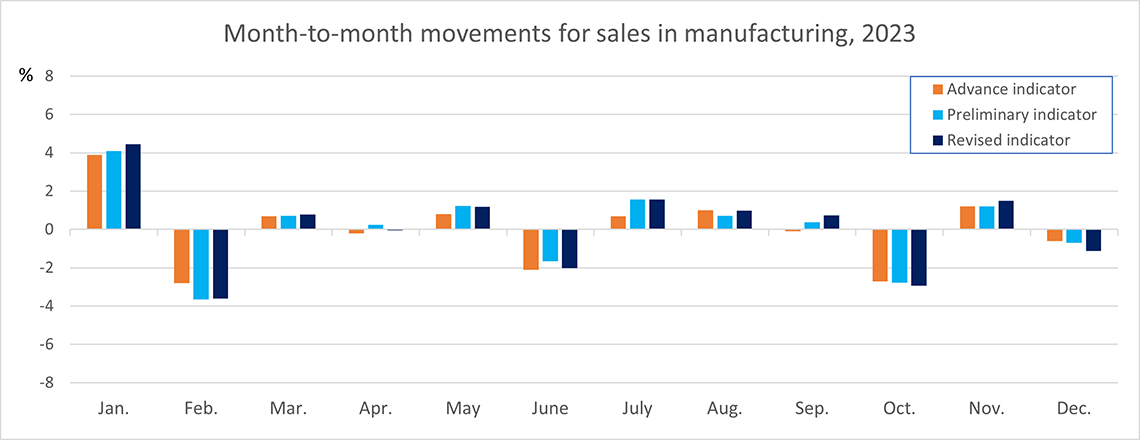

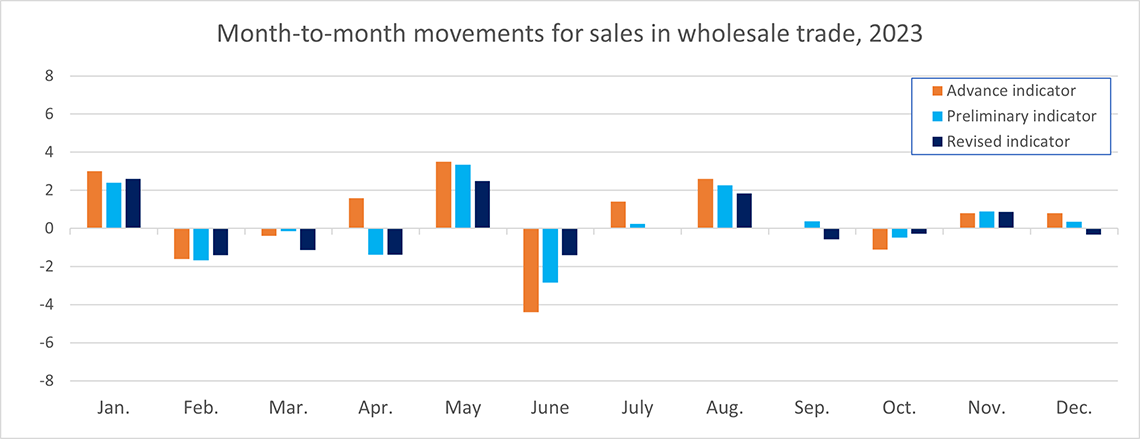

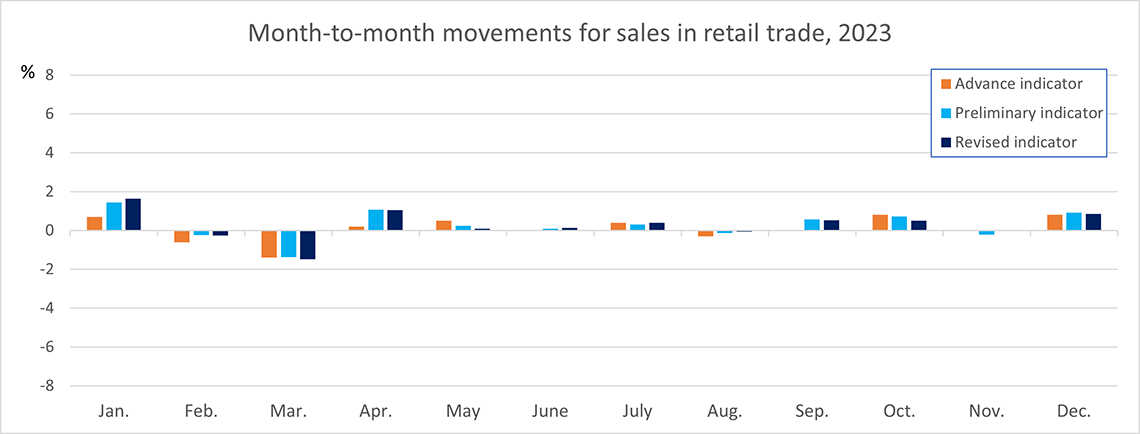

Figure 1 illustrates the published month-to-month movements for sales in manufacturing, wholesale trade and retail trade throughout the 2023 reference year. The advance, preliminary and revised indicators are highly coherent, in terms of both the direction (increase or decrease) and the magnitude of the month-to-month change in sales.

Figure 1 - Comparison of month-to-month movements from advance, preliminary and revised indicatorsFootnote 1

Description - Month-to-Month Movements for Sales in Manufacturing, 2023

Month-to-month movements for sales in manufacturing, 2023

Advanced indicator

Preliminary indicator

Revised indicator

January

3.9

4.1

4.5

February

-2.8

-3.6

-3.6

March

0.7

0.7

0.8

April

-0.2

0.3

-0.1

May

0.8

1.2

1.2

June

-2.1

-1.7

-2.0

July

0.7

1.6

1.6

August

1.0

0.7

1.0

September

-0.1

0.4

0.7

October

-2.7

-2.8

-2.9

November

1.2

1.2

1.5

December

-0.6

-0.7

-1.1

Description - Month-to-Month Movements for Sales in Wholesale, 2023

Month-to-month movements for sales in wholesale, 2023

Advanced indicator

Preliminary indicator

Revised indicator

January

3.0

2.4

2.6

February

-1.6

-1.7

-1.4

March

-0.4

-0.1

-1.1

April

1.6

-1.4

-1.4

May

3.5

3.3

2.5

June

-4.4

-2.8

-1.4

July

1.4

0.2

0.0

August

2.6

2.3

1.8

September

0.0

0.4

-0.6

October

-1.1

-0.5

-0.3

November

0.8

0.9

0.9

December

0.8

0.3

-0.3

Description - Month-to-Month Movements for Sales in Retail, 2023

Month-to-month movements for sales in retail, 2023

Advanced indicator

Preliminary indicator

Revised indicator

January

0.7

1.4

1.6

February

-0.6

-0.2

-0.2

March

-1.4

-1.4

-1.5

April

0.2

1.1

1.0

May

0.5

0.2

0.1

June

0.0

0.1

0.1

July

0.4

0.3

0.4

August

-0.3

-0.1

-0.1

September

0.0

0.6

0.5

October

0.8

0.7

0.5

November

0.0

-0.2

-0.0

December

0.8

0.9

0.9

4 Are there other approaches that can produce advance indicators?

Besides flash estimation, nowcasting is another method that can be used to produce advance indicators. In contrast to flash estimation, nowcasting encompasses more types of advance indicators that use either different input data or different compilation methods than preliminary indicators. For example, a nowcast may include estimators based entirely on models that use information from alternative sources available at the time when the model is applied to generate the nowcast. Similar to flash estimation, nowcasting models typically yield advance indicators that are less precise than preliminary indicators.

An important distinction exists between advance indicators produced at Statistics Canada and what are commonly referred to as forecasts. Typically, forecasting models are used to project data forward to describe future reference periods and as a consequence no information is available on the reference period of interest. The absence of observed data in forecasts increases the risk of inaccurate results because models rely on the assumption that historical trends and patterns will continue. In contrast, Statistics Canada incorporates some form of observed data in the production of advance indicators. Advance indicators released by Statistics Canada use direct observations as much as possible, such as data received from respondents or administrative data for a reference period of interest. The appropriate use of these data reduces the risk of large differences between advance indicators and preliminary indicators.

Section 2: Issues related to analysis and interpretation

1 What are the strengths and weaknesses of advance indicators?

Advance indicators provide timelier information to users; however, they are less precise than preliminary and revised indicators produced at a later date. Statistics Canada follows a multidimensional framework to assess data quality (Statistics Canada, 2019), including the dimensions of accuracy and timeliness. Statistical products typically aim to strike a balance between these dimensions to best meet the needs of data users. In this particular framework, advance indicators are intended to be timelier, with some compromise in accuracy. Because of this compromise in accuracy, the advance indicators are published at more aggregated levels of detail, such as the national level rather than the provincial level, compared with preliminary and revised indicators. They are also not released through the official Statistics Canada data repository but are only disseminated as part of articles in Statistics Canada's official release bulletin, The Daily.

2 How is the quality of advance indicators monitored?

Before this initiative, studies demonstrated that publishing advance indicators would provide a desirable balance of data timeliness and accuracy for users. In particular, the criteria used for accuracy accounted for the direction and the magnitude of relative month-to-month movements. This element is particularly important because it identifies turning points in a time series; the magnitude of movements is a key consideration because it estimates the pace of economic change. The historical performance of advance indicators produced with flash estimation was assessed, and these indicators outperformed forecasting and nowcasting methods with comparable timeliness. Furthermore, advance indicators can be generated approximately one month earlier than preliminary indicators.

Each month, Statistics Canada compares advance indicators with the preliminary indicators that follow for the same reference period to monitor the size of the differences between them, as well as their coherence in terms of the direction of the month-to-month movement.

Additionally, a comprehensive review of advance indicators and their past performance is conducted periodically. This review includes analysis of descriptive statistics over time, as well as any noteworthy differences observed for individual reference periods.

3 Why are advance indicators and preliminary indicators different?

Since advance indicators are derived using the same methods as preliminary indicators, they are subject to the same types of sampling and non-sampling errors, but with different sensitivities to these sources of error. The differences between advance and preliminary indicators can be attributed to the following sources:

Responses received after the production of advance indicators: Imputation, designed to produce unbiased and accurate aggregate estimates, is used to estimate values for each non-responding unit when advance indicators are produced. If an individual unit does not respond in time for the advance indicator but provides a response before the preliminary indicator is produced, this causes a difference between the advance and preliminary indicators. Large differences can occur when individual units have notable differences, or when relatively small differences accumulate from many units.

Improvements to imputation from additional responses received: Even for units that do respond in time for the advance indicator, the imputed values themselves can differ between advance and preliminary indicators. Since imputation for the preliminary indicator is based on more complete information, this indicator should be viewed as an improved estimate for non-responding units versus the advance indicator. While these differences are typically small, they can accumulate to yield notable differences between the advance and preliminary indicators.

Updates made to data after the advance indicator: When advance indicators are produced, respondent data are subjected to a further revision and are updated as part of the data validation process, which can result in differences between the advance and preliminary indicators.

4 Are other approaches being considered to produce advance indicators?

Statistics Canada continually seeks to adopt leading-edge methods to maximize data quality. To support these efforts, Statistics Canada collaborates regularly with other national statistical offices, other statistical organizations and academia to identify, develop and evaluate methods that would assist in producing advance indicators. In particular, nowcasting approaches hold promise to further improve timeliness, if statistical models with suitable accuracy relying only on the information available can be developed.

People are Statistics Canada's most valuable resource. Collectively, they drive the agency's mandate and priorities in producing statistics that help Canadians better understand their country. Staffing processes must be effective and efficient to ensure Statistics Canada hires the right people with the right competencies at the right time.

Staffing processes are a shared responsibility between the hiring manager and the staffing advisor. The hiring manager is responsible for making selection decisions that respect the public service values and ethics while acting in conformity with organizational goals. The staffing advisor is responsible for providing options, strategic advice, and guidance on the available staffing mechanisms and associated risks and considerations. The human resources (HR) assistant works alongside their assigned staffing advisor by being responsible for administrative components of the staffing process, such as creating and maintaining the staffing action file in GCdocs. Finally, Corporate Staffing is responsible for designing the staffing process; monitoring; and overseeing many of the fundamental components that support staffing advisors and HR assistants in executing staffing actions, such as developing tools and templates, developing training and guidance, and representing the agency in the event of a complaint.

The agency has experienced an extraordinary staffing landscape since the onset of the COVID-19 pandemic . Annual staffing actions processed by the agency grew from 6,473 in 2019/2020 to 13,947 in 2021/2022, before falling to 8,643 in 2022/2023. As hiring ramped up to meet the demands of new projects and programs, staffing processes were strained, leading to a backlog of staffing actions. This sudden increase took place during a period when HR leadership and teams were seized with efforts to transition the agency to full telework (followed by a shift to a hybrid model), multiple implementations of vaccine reporting, the hiring of thousands of contact tracers and the implementation of a rapid testing program for census employees. However, through significant work and effort, and without additional resources, the agency successfully recruited all required employees to work on the new projects and programs. This extraordinary staffing volume is not expected to be repeated in the foreseeable future.

Why is this important?

Staffing actions more than doubled over the last few years, leading to a persistent backlog and increasing the length of time to hire. An effective and efficient staffing process is critical to ensuring Statistics Canada has the HR required to achieve its mandate and priorities.

Further, according to the Public Service Commission's Appointment Framework, Statistics Canada is required to conduct a cyclical assessment at least once every five years. This assessment takes a broad look at the health of the organizational staffing system and identifies areas that need to be strengthened, as well as potential measures to address weaknesses. This Audit of Staffing contributes to fulfilling this requirement.

Overall conclusion

The agency's staffing processes have been stressed by a sudden increase in the volume of staffing transactions, combined with the departure of experienced staffing advisors. To optimize the effectiveness and efficiency of the staffing process as the agency moves towards more regular staffing levels, opportunities for improvement were identified in the areas of staffing advisor support and development, process design and documentation, staffing integrated systems, and the monitoring of and reporting on the process.

Key findings

Hiring managers' views on staffing

While the agency has been successful in recruiting employees to meet the increased demand in recent years, the administrative burden of staffing processes on hiring managers has resulted in some frustration among hiring managers. They find it cumbersome and overly compliance driven, inefficient, and sometimes ineffective in finding the best candidate. While acknowledging the challenges faced by staffing advisors, hiring managers would like to better leverage HR expertise throughout the staffing process.

Staffing advisor and human resources function views on staffing

There has been significant turnover in the staffing team in recent years. Most staffing advisors are new to their role, yet do not feel adequately supported. Staffing processes are not well defined, are not optimized at the agency level, are inadequately supported by integrated information systems and undergo frequent change. Together, these factors add administrative burden for staffing advisors and make it difficult for them to fully meet hiring manager expectations.

Monitoring the efficiency and effectiveness of the staffing process

There is limited reporting on metrics related to the efficiency and effectiveness of staffing processes overall. This type of monitoring would support data-driven decision making and the ongoing improvement of the effectiveness and efficiency of the staffing process.

Conformance with professional standards

The audit was conducted in accordance with the Mandatory Procedures for Internal Auditing in the Government of Canada, which include the Institute of Internal Auditors'International Standards for the Professional Practice of Internal Auditing.

Sufficient and appropriate audit procedures have been conducted, and evidence has been gathered to support the accuracy of the findings and conclusions in this report and to provide an audit level of assurance. The findings and conclusions are based on a comparison of the conditions, as they existed at the time, against pre-established audit criteria. The findings and conclusions are applicable to the entity examined and for the scope and period covered by the audit.

Steven McRoberts

Chief Audit and Evaluation Executive

Introduction

Background

People are Statistics Canada's most valuable resource. Collectively, they drive the agency's mandate and priorities in producing statistics that help Canadians better understand their country. Staffing processes must be effective and efficient to ensure Statistics Canada hires the right people with the right competencies at the right time.

The agency has defined three specific objectives for the staffing process that can be summarized as follows:

Achieving operational objectives: The agency must build an agile and competent workforce through effective human resources (HR) planning activities and staffing and recruitment strategies adapted to its organizational context and business needs.

Compliance: The agency must ensure compliance with the Public Service Employment Act (PSEA), the Values and Ethics Code for the Public Sector, and requirements of internal and central agency policies.

Equity, diversity and inclusion: Hiring managers should always look for the best qualified person to fill a position. They must also put in place strategies to attract talent from different backgrounds who offer a wide variety of ideas and strengths that, together, lead to innovative outcomes.

Staffing processes are a shared responsibility between the hiring manager and the staffing advisor. The hiring manager is responsible for planning for their workforce; identifying needs; engaging meaningfully with HR throughout the process; providing information as required; and ultimately making selection decisions that respect public service values and ethics, legislation, and policies while acting in conformity with organizational goals. The staffing advisor is responsible for providing options, strategic advice, and guidance on the available staffing mechanisms and associated risks and considerations. The HR assistant works alongside their assigned staffing advisor by being responsible for administrative components of the staffing process, such as creating and maintaining the staffing action file in GCdocs. Finally, Corporate Staffing is responsible for designing the staffing process; monitoring; and overseeing many of the fundamental components that support staffing advisors and HR assistants in executing staffing actions, such as developing tools and templates, developing training and guidance, and representing the agency in the event of a complaint.

Staffing mechanisms within the federal public service are subject to the PSEA, the Treasury Board's Policy on People Management, and the Public Service Commission's (PSC) Appointment Framework. Notably, the PSC's Appointment Framework was launched in 2016 with the intention of streamlining requirements, reducing administrative burden, offering greater flexibility and accountability, encouraging agile and customized approaches to staffing and policies, and increasing focus on outcomes. Within Statistics Canada, hiring also adheres to the agency's Staffing Governance Framework, which took effect on May 15, 2022.

In 2020/2021, like all organizations, Statistics Canada responded to the COVID-19 pandemic quickly, pivoting operations to focus on mission-critical programs and, with an unprecedented need for data, delivering data-driven insights to Canadians at a time when they were needed most. Throughout this time, the agency experienced an extraordinary staffing landscape as annual staffing actions processed by the agency grew from 6,473 in 2019/2020 to 13,947 in 2021/2022, before falling to 8,643 in 2022/2023. This sudden increase took place during a period when HR leadership and teams were seized with efforts to transition to full telework (some 7,500 employees were moved to telework, a great advance), followed by a shift to a hybrid model (including the use of personas, pulse surveys and an employee wellness survey to support employees' transition to a hybrid work environment); multiple implementations of vaccine reporting; the hiring of thousands of contact tracers (over 2,000 additional Statistical Survey Operations employees were hired in less than four months); and the implementation of a rapid testing program for census employees. As hiring ramped up to meet the demands of new projects and programs, the agency struggled to keep pace, leading to a persistent backlog of staffing actions. However, through significant work and effort, and without additional resources, the agency successfully recruited all required employees to work on the new projects and programs. This extraordinary staffing volume is not expected to be repeated in the foreseeable future.

Audit objective

The objective of this audit is to provide reasonable assurance on the effectiveness and efficiency of staffing processes and tools to facilitate appropriate and timely staffing of personnel.

Scope

The scope of the engagement included an examination of selected components of the agency's management control framework for staffing, including processes to

ensure management and the Workforce and Workplace Branch work in partnership to execute on staffing needs and priorities

enable all parties to understand and adhere to their respective staffing responsibilities

enable effective and timely staffing in accordance with management's needs.

Compliance with the PSC's Appointment Framework was excluded from the engagement scope, as the Workforce and Workplace Branch conducts annual self-assessments of staffing files to assess compliance and identify areas for improvement.

For the purposes of this engagement, the staffing process was considered to begin when the hiring manager identifies a need to fill a vacancy and to be complete once the letter of offer is issued to the selected candidate.

The scope period covered processes in place for the fiscal years 2021/2022 to 2022/2023.

Executive staffing was excluded from the engagement scope, as it follows different processes and requirements from other staffing actions.

Finally, the engagement scope also excluded the following elements, as they would be better assessed through separate, targeted engagements: the parts of the hiring process that take place after the selection of the successful candidate (including the security clearance process and pay-related processes); equity, diversity and inclusion initiatives; official languages measures; and financial management controls.

Approach and methodology

This audit was conducted in accordance with the Mandatory Procedures for Internal Auditing in the Government of Canada, which include the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing.

The audit work consisted of

examination and analysis of relevant internal documentation

questionnaires for hiring managers and staffing advisors

interviews and walkthroughs with hiring managers from across the agency, staffing operations team leads, staffing advisors, HR assistants and a team lead, along with representatives from Corporate Staffing and HR management.

Authority

The audit was conducted under the authority of the approved Statistics Canada Integrated Risk-based Audit and Evaluation Plan (2023/2024 to 2027/2028).

Findings, recommendations and management response

Hiring managers' views on staffing

While the agency has been successful in recruiting employees to meet the increased demand in recent years, the administrative burden of staffing processes on hiring managers has resulted in some frustration among hiring managers. They find it cumbersome and overly compliance driven, inefficient, and sometimes ineffective in finding the best candidate. While acknowledging the challenges faced by staffing advisors, hiring managers would like to better leverage HR expertise throughout the staffing process.

Staffing is a shared responsibility between hiring managers, staffing advisors and HR assistants. Staffing advisors and HR assistants support the administration of the process, while hiring managers are accountable for planning their staffing needs, making selection decisions, and ensuring compliance with staffing-related legislation and policies.

Staffing processes are cumbersome and overly compliance driven

While the agency's objectives for staffing do not explicitly include the concept of efficiency, achieving the three objectives in the least amount of time and at the lowest cost to the agency remains an important, yet unstated, goal. Further, these objectives are sometimes in tension with one another, requiring careful balancing to optimize results. Specifically, achieving operational objectives and ensuring compliance are often at odds, as attaining compliance adds burden to the process and can delay staffing actions, putting operational objectives at risk.

Hiring managers noted that staffing templates, established to demonstrate compliance, are burdensome and time-consuming to complete. They questioned whether the agency was striking the right balance between operational and compliance objectives, noting that often the feedback they received when completing the forms added marginal business value. Hiring managers also reported that staffing advisors each had their own interpretation of what was required and the point at which compliance requirements were satisfied.

Completing the Candidate Assessment Validation (CAV) form was identified as a common challenge in this regard. This form exists to fulfill compliance objectives and the PSEA requirement that the hiring decision for non-advertised appointments be documented. Staffing advisors and hiring managers alike noted that hiring managers spend significant time in completing the document and that it often included multiple rounds of going back and forth between the hiring manager and staffing advisor. The CAV template did not provide detailed guidance on what could represent sufficient documentation of the hiring decision, leaving room for varying interpretations of the point at which the documentation was acceptable.

Striving for perfection in achieving compliance can lead to inefficiencies and unnecessary complications. While it is essential to meet the requirements set by the PSC, aiming for perfection beyond the established threshold can result in prolonged staffing processes, increased administrative burden and cost, and delays in filling critical positions. An overemphasis on perfection can also divert resources and attention from other pressing matters, leading to an imbalance in priorities.

Certain staffing processes are slow and may not result in finding good candidates

Two-thirds of hiring managers noted that traditional staffing processes and assessments were not always effective in finding the right candidate. While candidates often looked good on paper and answered questions appropriately in the interview stage, their on-the-job performance was not always reflective of their assessment results. Certain types of staffing actions are very labour-intensive for hiring managers, with varying results in finding candidates with the specific skills they are looking for. Other challenges included processes receiving too few applicants and taking too long (applicants often accepted positions elsewhere when the processes took too long).

Hiring managers also reported using several staffing actions to expedite employee start dates with the agency. In such scenarios, once a candidate is selected, they are offered an acting appointment to allow time for an indeterminate appointment to be processed. While this practice effectively speeds hiring, it also increases the workload for both staffing advisors and hiring managers as it creates two staffing actions in the place of one.

Siloed human resources functions create extra steps in the process for hiring managers

There are various HR functions that can be involved in a hiring process, including staffing and classification, along with other functions within the Corporate Strategy and Management Field (e.g., security, official languages and finance). Hiring managers reported taking on the facilitator role between the various HR functions, which were viewed as siloed. Several hiring managers noted that they are uncertain which group to reach out to for various HR issues, and this could add to the complexity and time of the staffing process. Members of the staffing function also expressed similar concerns.

Hiring managers want to better leverage strategic support from their staffing advisors

While acknowledging the challenges faced by staffing advisors, hiring managers indicated they would like staffing advisors to take on more responsibility throughout the staffing process. This would allow the agency to leverage the expertise of the staffing advisors and would align with the desired evolution of the staffing function. This change would include support such as providing strategic advice, assisting with screening large numbers of candidates and helping with the completion of mandatory compliance documentation. As the staffing function is not currently resourced or equipped to provide this level of support, some fields and divisions have created staffing "shadow shops" to perform these tasks. Using their knowledge of the hiring manager's business needs and past knowledge of the staffing process, these support teams act as a liaison between hiring managers and staffing advisors.

However, these shadow shops create challenges for staffing advisors. They disconnect the staffing advisor from the business, resulting in the advisor focusing mostly on the administrative aspects. Further, the guidance provided by the shadow shops may not align with that of the staffing advisor. While some of these shops have been disbanded or reduced, the demand for their services has not waned. Many staffing advisors acknowledged the need for the services these shadow shops provide. The team of staffing advisors wants to better support clients and acknowledged the challenges in the current environment, which include the high volume of staffing actions, the number and diverse needs of hiring managers they serve, and the administrative burdens caused by a manual and inefficient staffing process (discussed further in the Monitoring the efficiency and effectiveness of the staffing process section below).

The staffing process has not been designed to optimize efficiency and effectiveness

Many of the issues identified point towards a staffing process that has been designed based on accountabilities, rather than efficiency and effectiveness. Along these lines, the total cost of the staffing process is not known or monitored. While the cost of the staffing function itself is known, the considerable time invested by hiring managers in staffing is not tracked. Hiring manager time has thus become an unmeasured resource when designing the staffing process, and over time the process can drift towards being optimized at the staffing function level rather than the agency level. This results in tasks being assigned to hiring managers because they are accountable for them, not because they are the most efficient or effective people to perform them. In many cases, tasks for which hiring managers are accountable may be better or more efficiently performed by a centralized resource with the knowledge and volume of transactions to become proficient in the tasks.

For example, hiring managers are accountable for the selection decision. Consequently, they are expected to define the competencies required for a position, develop assessment tools for each competency, and evaluate the assessment tools for bias—all with limited support or training in these activities. Each of these activities can benefit from in-depth knowledge and experience and may be more effectively and efficiently performed, or guided, by a centralized resource with expertise in competencies and their assessment. Under an agency-level mindset, a more efficient and effective process might have a centralized resource maintain a bank of competencies, complete with definitions and bias-free assessment tools. Hiring managers could leverage these as required, rather than having to independently research competencies and develop assessment tools for their own personal use. While the agency does maintain a bank of tools for larger collective processes that are repeated on a periodic basis, similar support is not available for individual processes.

Staffing advisor and human resources function views on staffing

There has been significant turnover in the staffing team in recent years. Most staffing advisors are new to their role, yet do not feel adequately supported. Staffing processes are not well defined, are not optimized at the agency level, are inadequately supported by integrated information systems and undergo frequent change. Together, these factors add administrative burden for staffing advisors and make it difficult for them to fully meet hiring manager expectations.

Staffing advisors, operating within the existing manually driven processes, are faced with many challenges while supporting hiring managers. Many staffing advisors are new to their role and would like more support and the opportunity to learn from more experienced advisors. A commonly identified theme was that staffing advisors have the best interests of the agency and hiring managers in mind and are dedicated to providing an effective service.

Most staffing advisors are new to their role

Staffing advisors play a key role in the staffing process. They are process experts, responsible for guiding hiring managers from need identification to the appointment of the chosen candidate. They provide strategic advice on staffing mechanisms, risks and compliance requirements. This advice demands a strong understanding of their clients' business and staffing needs; of how to reach, attract and assess high-quality candidates; and of how to navigate the complex web of regulations, policies and directives that govern federal government hiring.

Across the federal government, staffing advisors are in short supply and in high demand, making movement between departments a common challenge.

As noted, the agency has seen a sharp increase in the volume of staffing actions over the past few years. Concurrently, turnover rates among the agency's Personnel Administration (PE) category have also spiked. During this time, the agency experienced turnover rates of 25% to 33% among PEs, compared with 7% to 12% across the federal public service. In 2022/2023, the staffing function had a turnover rate of 36%, compared with a turnover rate of 23% for the agency.

Management reported difficulty in replacing departing experienced staffing advisors with similarly experienced advisors. Consequently, junior staffing advisors (PE-01 or PE-02 levels) were hired in their place. As of September 2023, the agency had 14 staffing advisors in total: 12 junior staffing advisors at the PE-01 or PE-02 level and 2 senior staffing advisors at the PE-03 level.

Staffing advisors require more support, straining team leads working to fill the gap

Developing a staffing advisor takes time, training and mentoring. They begin at the PE-01 level as a developmental HR advisor, typically for a period of one year or more, before progressing to the PE-02 level as an HR advisor, at which point they deliver operational services of limited scope. Junior staffing advisors are supported throughout this process by a more experienced staffing advisor at the PE-03 (HR specialist) or PE-04 (team lead) level. This advisor serves as a mentor, allowing the junior advisor to shadow them, reviewing their work before it is communicated to the hiring manager and acting as a sounding board when they encounter difficult situations. It is only once staffing advisors have attained the PE-03 HR specialist level that they may work fully independently and are considered to provide expert staffing advice.

Because of this high turnover among senior staffing advisors, junior staffing advisors have been assigned as lead advisors to work directly with hiring managers without an assigned mentor (but with supervision from their team lead). In some respects, they are performing the responsibilities of a senior staffing advisor without having the knowledge, experience or support to perform at that level. Junior staffing advisors reported taking on roles they do not feel sufficiently equipped or supported to execute. Many reported being uncomfortable providing advice to senior managers and executives without having experience with all types of staffing actions (particularly advertised processes) or fully understanding staffing processes.

With a shortage of experienced staffing advisors, team leads are struggling to fill the gap. The staffing team is presently composed of two team leads, each of whom is assigned seven to eight staffing advisors. Staffing management reported that team sizes of four to five were more typical, with a mix of junior and experienced advisors. Team leads reported being overwhelmed with their workload and having to work overtime to keep up while providing coaching, review and ongoing support to junior staffing advisors. Staffing advisors also noted that team leads seemed overburdened, making staffing advisors hesitant to approach them when they needed help. They stated this has led to delays in responding to hiring managers and has slowed the staffing process.

Frequent rotation of staffing advisors across client groups is causing frustration for hiring managers and staffing advisors

Adding to these challenges, the high turnover and volume of staffing actions have resulted in a frequent rotation of client groups among staffing advisors. Hiring managers and staffing advisors expressed frustration with this constant change and noted that greater stability was required. For staffing advisors, frequent rotation makes it difficult to establish strong working relationships with their clients and to understand their business and their needs. For hiring managers, a new staffing advisor requires dedicating time to update them on ongoing staffing actions, their business and their broader staffing needs. It also means adjusting to different ways of doing things, which can lead to challenges as advisors may have different interpretations of what is required and how the staffing process should proceed.

The shortage of experienced staffing advisors able to provide expert advice, coupled with the frequent rotation of staffing advisors across client groups, has affected the quality of service staffing advisors can provide and the cohesion between hiring managers and staffing advisors. These factors also serve to compound the other challenges discussed throughout this report.

Hiring managers are not involving staffing advisors early in the process

HR management noted that a common challenge concerned staffing advisors not being informed of staffing needs and activities early enough in the process. Last-minute requests result in backdated transactions and a high volume of urgent staffing actions. These issues make it difficult for staffing advisors to plan their work; complicate pay processes; and create problems for employees, who risk being paid wrong, late or not at all, or experiencing delays or refusal of benefits. These issues also affect the relationship between hiring managers and staffing advisors. Hiring managers expressed a desire for more support from their staffing advisors. Likewise, staffing advisors expressed a desire to provide more strategic advice and support to hiring managers and to be seen as a trusted partner in their clients' staffing activities. However, not involving staffing advisors early in the process relegates them to simply processing paperwork, often under tight time pressures. This in turn can lead to staffing advisors being seen as an obstacle to hiring managers, as the staffing advisor is left scrambling to ensure all the administrative requirements necessary to process the staffing action are fulfilled.

The agency introduced a timeliness initiative in May 2023 to establish clear timelines that hiring managers must meet for HR actions to be processed in time. As the initiative was implemented during the audit, it was not possible to assess its effectiveness. That said, management hopes that it will increase rigour and discipline in staffing processes and lead to hiring managers including staffing advisors earlier in their staffing actions.

Staffing processes are not well defined, making it difficult to optimize the process

Well-designed and implemented processes and procedures contribute to an effective staffing function. They help ensure common and standardized approaches in the administration of staffing actions, establish clear expectations for the level of service provided by staffing advisors, and inform all participants of the requirements and timelines of a typical staffing action. They can also ensure the most efficient approach is taken on each staffing action by properly sequencing actions and ensuring that no steps are forgotten.

Staffing advisors and hiring managers noted that the process was not fully defined. The HR function has not developed clear, comprehensive and documented procedures outlining the specific steps required for each type of staffing process. That said, a comprehensive flowchart was developed for the non-advertised staffing process in coordination with Field 7's Operations and Integration Division but was not shared with staffing advisors or hiring managers as the project was discontinued because of fiscal constraints. This work is a good start and could be leveraged in documenting other types of staffing actions. Various checklists have also been developed to define the key documentation required for each type of staffing action, but hiring managers and junior staffing advisors reported that these were not sufficiently detailed to meet their needs as they do not include all the steps of the process, the expected timelines for each step or the purpose behind each step.

The lack of clear, standardized procedures has resulted in a process that varies depending on the staffing advisor and hiring manager involved.

As an example, a key step at the outset of a staffing action is the development of the statement of merit criteria (SoMC). This document outlines the experience, skills and competenciesFootnote 1 required for the position and forms the basis of the candidate assessment. Completing the SoMC is the responsibility of the hiring manager, with guidance from the staffing advisor. There was no common approach to determining the level of support that should be provided. Also, staffing advisors who reported sharing SoMCs from other departments were sharing them from their personal collection rather than a list curated and maintained by the agency and available to all other staffing advisors.

Non-integrated information systems create administrative burden for staffing advisors

Information management and information technology (IT) systems are required to facilitate efficient and effective staffing processes. These systems should support process flows, document management, and monitoring and reporting.

Statistics Canada employs several systems to support its staffing process. These systems include Orbit, the Staffing Activity Management System, a work-in-progress (WIP) spreadsheet shared among all staffing advisors, SharePoint for financial approvals, GCdocs for key documents, staffing advisor and HR assistant mailboxes for correspondence and documents in progress, and various spreadsheets and other unique tools created and used by staffing advisors and HR assistants to track their files. Notably, these systems are not integrated, affecting the availability and accuracy of data related to the staffing process. Many data points are duplicated across multiple systems, leading to conflicting information that needs to be reconciled when information is compiled for reporting purposes.

These disparate systems add significant burden for staffing advisors, create complications and frustration for hiring managers, cause delays to staffing processes, and take staffing advisor time away from providing strategic support to their clients. There are also multiple entry points for new staffing actions, meaning staffing advisors must monitor their emails, SharePoint and WIP to know what work they have underway. Reporting for senior management requires staffing advisors to manually compile and reconcile data from multiple systems. Hiring managers cannot see the status of their staffing actions, leading to numerous emails to staffing advisors requesting status updates that must also be manually compiled and reconciled by staffing advisors. Additionally, the systems do not support the process of completing the required forms, meaning that they must be shared by email between the hiring manager, their delegate and the staffing advisor during their development, leading to lost documents and version control issues. These issues create frustration and undermine the hiring manager's trust in the staffing advisor in several ways. First, the lack of system-level support for the staffing process can make it hard for staffing advisors to locate files from previous staffing actions, giving the appearance of disorganization to hiring managers. Second, staffing advisors sometimes ask hiring managers to provide documents a second or third time for a given process, causing frustration and a loss of trust among hiring managers who understood that the staffing advisor was responsible for storing documentation for the staffing action.

Further, there is no formal documentation on which system is used to track what information, who should enter the information and when it should be done. Staffing advisors and their HR assistants work out roles and responsibilities between themselves. Consequently, some HR assistants may do more to support their staffing advisor while others may do less. These inconsistencies are manifested in the information available in the systems.

The HR team has undertaken a project to implement an integrated system to automate monitoring and improve the efficiency of the staffing process. However, this is not its first attempt to do so. Previous attempts have been set aside in favour of newer or more urgent priorities or have had their scope changed during implementation such that they did not deliver the integrated system that had been envisioned. Several concerns were raised regarding this current implementation that warrant consideration:

Senior HR management stated an expectation of implementation in the fall at minimal cost (attributable to having the selected software available to the agency at no additional cost). However, according to IT staff, a project of this scope will take months (at minimum) to implement, making a fall implementation unrealistic. They further noted that the development costs will be significant.

Two competing software alternatives are being considered. These alternatives were chosen for their low cost (the agency already owns licensing for them) and pre-existing in-house support. However, the system selection is being conducted while user needs are still being defined by Corporate Staffing, and staffing processes have not yet been documented.

The requisite resources from IT and Human Resources Business Intelligence (HRBI) have not been formally assigned to the project. It is being conducted "from the corner of the desk," and the HRBI team expressed concerns about competing priorities and deadlines that may affect the system implementation. The availability of the IT team to work on this project is also dependent on other priorities and resource constraints.

Frequent process changes with insufficient communication affect awareness and buy-in

Staffing advisors, Corporate Staffing and hiring managers reported a high pace of change in staffing priorities and processes. Staffing advisors are asked to communicate these changes to hiring managers and enforce the changes when hiring managers push back. However, staffing advisors said they were frequently not consulted on the changes or their implementation or told why the change was being made. As a result, there are missed opportunities to consult staffing advisors for their input and to prepare them to answer questions from hiring managers and build buy-in and awareness for the changes.

Monitoring the efficiency and effectiveness of the staffing process

There is limited reporting on metrics related to the efficiency and effectiveness of staffing processes overall. This type of monitoring would support data-driven decision making and the ongoing improvement of the effectiveness and efficiency of the staffing process.

Establishing clear performance targets and tracking the performance of the staffing process are important and can provide valuable data to support the improvement of its efficiency and effectiveness.

The agency has established timeliness service standards for each type of staffing action, but these standards are insufficient for assessing the efficiency of the overall process. These standards address only the time elapsed after all the documentation has been satisfactorily completed by the hiring manager. It therefore excludes the time spent planning the staffing action and soliciting, screening, interviewing and assessing candidates, as well as the time spent by the hiring manager documenting the selection decision. It also excludes any time spent going back and forth with the staffing advisor to bring the documentation to a satisfactory state.

Without clear targets and more complete monitoring of the time to hire (from need identification to start date), cost to hire (inclusive of hiring manager time) and time spent on the various steps of the process, it is difficult to know whether the staffing process is appropriately designed to meet agency needs or to understand where it may be falling short. Including hiring manager time—by tracking it through the Time Management System or elsewhere—in the cost of the process will be critical to understanding whether portions of the process would be better assigned to lower-cost resources or centralized resources with specialized expertise. These targets, particularly time to hire and cost to hire, should be negotiated with senior management to ensure that the staffing process is designed to appropriately balance cost, compliance objectives and business needs.

The effectiveness of the process is also not currently monitored. This can include monitoring the effectiveness of specific aspects of the staffing process (such as quality of staffing advisor advice and guidance) but should also include monitoring the quality of hires. Doing so could help identify which types of staffing processes are most successful, as well as areas where more work is required to improve effectiveness, such as better identifying the skills and competencies required for a job or designing new assessment tools that more accurately predict on-the-job performance.

Recommendations

Recommendation 1

It is recommended that the assistant chief statistician, Corporate Strategy and Management, ensure that

a consistent approach to each type of staffing action be documented, communicated and implemented.

Management response

Management agrees with the recommendation.

A comprehensive review and analysis of staffing processes will be undertaken, prioritizing the staffing actions that account for the greatest staffing volume, and will include

working with partners in fields 6 and 7 to define and document each type of staffing process, including the steps within the process, the timelines associated with each step, and the roles and responsibilities of each individual involved

producing documentation and tools that support a standardized approach to staffing processes, with clear roles and responsibilities for each individual involved and associated timelines

refreshing the staffing page on the Internal Communications Network (ICN) to articulate staffing processes, steps and requirements, as well as roles and responsibilities for each individual involved in the process.

Deliverables and timeline

The director general, Workforce and Workplace Branch, will

document process maps for each type of staffing action (approximately 20 in total), 10 of which account for 96% of the actions that make up the staffing transaction volume; the first 10 processes will be done in 2024, and the remaining lower-priority processes will be done in 2025, with the following schedule: 5 processes documented by the end of June 2024, 5 processes documented by the end of December 2024, 5 processes documented by the end of June 2025 and the remaining processes documented by December 2025

launch tools spanning guides, infographics and training materials by the beginning of June 2024, with the release of process-specific tools aligning with timeframes in the previous deliverable

refresh and update the staffing page on the ICN by the beginning of June 2024.

Recommendation 2

It is recommended that the assistant chief statistician, Corporate Strategy and Management, ensure that

a plan to address gaps in the development, day-to-day support and retention of staffing advisors be developed and implemented.

Management response

Management agrees with the recommendation.

A thorough review will be conducted to understand and implement the measures required to better support the development and retention of staffing advisors.

To address the findings of the review, the following will be developed: standard procedures; supporting tools; and a development program for staffing advisors that encompasses a blend of formal training, informal training, coaching, and exposure to a range of staffing files and actions to support development and consistency in service delivery. This includes reviewing and updating the PE Recruitment and Development Program, support measures, and training roadmaps and career paths for staffing advisors.

Deliverables and timeline

The director general, Workforce and Workplace Branch, will

document a review of planned measures to support the development and retention of staffing advisors by September 2024.

Recommendation 3

It is recommended that the assistant chief statistician, Corporate Strategy and Management, ensure that

a business case be developed and executed for the implementation of an integrated system to enable the staffing function to efficiently carry out its responsibilities, reduce administrative burden and enable monitoring.

Management response

Management partially accepts the recommendation.

Because of austerity, it is not anticipated that any investment in an integrated system will be supported by central agencies over the next number of years. Management will

conduct an internal scan to determine integrated system needs, gaps and immediate options

conduct an external scan with the Office of the Chief Human Resources Officer to determine anticipated implementation dates for Next Generation Human Resources and Pay (NextGen HR and Pay) to determine potential implementation at Statistics Canada

as an interim measure, implement Workbench to improve tracking of actions and improve oversight of processes.

Deliverables and timeline

The director general, Workforce and Workplace Branch, will

present a documented internal and external scan to define integrated system needs, gaps, and recommended short- and long-term solutions (including NextGen HR and Pay) for the approval of the assistant chief statistician, Corporate Strategy and Management, by March 2024

complete Workbench system changes to improve tracking of actions and improve oversight of processes by June 2024.

Recommendation 4

It is recommended that the assistant chief statistician, Corporate Strategy and Management, ensure that

key performance indicators and targets for the efficiency and effectiveness of the staffing process be developed, implemented, monitored and reported to senior management.

Management response

Management agrees with the recommendation.

Management will establish a systematic approach to measure the performance and health of the staffing activity. This will include developing quantitative key performance indicators (KPIs) and targets to gauge the efficiency of staffing processes (including time elapsed and effort expended on staffing actions) and the effectiveness of the staffing process (including measures of hiring manager satisfaction).

Deliverables and timeline

The director general, Workforce and Workplace Branch, will

present to the Operations Committee for review and approval a plan for the monitoring and reporting of staffing activity results, including the proposed monitoring cycle by June 2024

present to the Operations Committee for review and approval specific KPIs and targets to be monitored by December 2024 (for the first 10 staffing processes documented, as outlined in the first deliverable)

present reporting of results to the Operations Committee by December 2025 (and ongoing).

Recommendation 5

It is recommended that the assistant chief statistician, Corporate Strategy and Management, ensure that

an agency-level plan to assess and improve the efficiency and effectiveness of the staffing process be developed, following the implementation of actions associated with recommendations 1 through 4, in a way that balances operational objectives with compliance requirements; senior management should be consulted in its development and approve the plan, and progress on its implementation should be reported to a tier 1 governance committee periodically.

Management response

Management agrees with the recommendation.

Following implementation of actions linked to recommendations 1 through 4, management will conduct an annual review of the staffing system to further identify efficiencies, review compliance requirements and measure effectiveness of the function, with input from senior management.

Deliverables and timeline

The director general, Workforce and Workplace Branch, will

present to the Operations Committee for approval a review of the efficiency and effectiveness of the staffing function and proposed action plan to address areas for improvement, the initial part of the review to begin in June 2026, following the completion of process and efficiency reviews of all staffing processes, with a target presentation date of December 2026.

Appendices

Appendix A: Audit criteria

Audit criteria

Control objectives

Core controls and criteria

Policy instruments and sources

1. The planning of staffing processes is efficient and effective, and hiring managers, staffing advisors and human resources (HR) assistants are adequately supported.

1.1 The planning of staffing processes is efficient.

1.2 The planning of staffing processes is effective in defining the staffing need and establishing a staffing strategy that fulfills the identified need.

1.3 Hiring managers, staffing advisors and HR assistants are adequately supported throughout the planning process.

Statistics Canada's Staffing Governance Framework

Audit Criteria related to the Management Accountability Framework: A Tool for Internal Auditors

Human resource planning is aligned with strategic and business planning. (PPL-1)

The organization provides employees with the necessary training, tools, resources and information to support the discharge of their responsibilities. (PPL-4)

Suitable policies and procedures to support the development and management of human resources are established, maintained and communicated. (PPL-7)

2. The assessment of candidates is efficient and effective, and hiring managers, staffing advisors and HR assistants are adequately supported.

2.1 The assessment of candidates is efficient.

2.2 The assessment process is effective in determining candidate suitability.

2.3 Hiring managers, staffing advisors and HR assistants are adequately supported throughout the assessment process.

Statistics Canada's Staffing Governance Framework

Audit Criteria related to the Management Accountability Framework: A Tool for Internal Auditors

Human resource planning is aligned with strategic and business planning. (PPL-1)

The organization provides employees with the necessary training, tools, resources and information to support the discharge of their responsibilities. (PPL-4)

Suitable policies and procedures to support the development and management of human resources are established, maintained and communicated. (PPL-7)

3. The selection of candidates is efficient and effective, and hiring managers, staffing advisors and HR assistants are adequately supported.

3.1 The selection process is efficient.

3.2 The selection process is effective in facilitating the hiring manager's candidate selection decision.

3.3 Hiring managers, staffing advisors and HR assistants are adequately supported throughout the selection process.

Statistics Canada's Staffing Governance Framework

Audit Criteria related to the Management Accountability Framework: A Tool for Internal Auditors

Human resource planning is aligned with strategic and business planning. (PPL-1)

The organization provides employees with the necessary training, tools, resources and information to support the discharge of their responsibilities. (PPL-4)

Suitable policies and procedures to support the development and management of human resources are established, maintained and communicated. (PPL-7)

4. The staffing process is monitored to support its continuous improvement and ensure business needs are met.

4.1 Targets to monitor the efficiency and effectiveness of the staffing process are established, aligned with business needs and monitored.

4.2 Results of process monitoring are used to identify and address areas of weakness.

Statistics Canada's Staffing Governance Framework

Audit Criteria related to the Management Accountability Framework: A Tool for Internal Auditors

The oversight body / bodies request and receive sufficient, complete, timely and accurate information. (G-6)

Management has identified planned results linked to organizational objectives. (RP-1)

Management has identified appropriate performance measures linked to planned results. (RP-2)

Management monitors actual performance against planned results and adjusts course as needed. (RP-3)

The 2021 Census of Population revealed that 243,155 people reported the ability to speak an Indigenous language well enough to conduct a conversation. More than 70 distinct Indigenous languages were reported in the census.

Using census data, the Indigenous languages: Visualization tool provides key statistics on Indigenous languages such as the number of speakers, people with an Indigenous language as a mother tongue as well as people who acquired it as a second language. Data on home languages and silent speakers are also included.

In 2022, 80% of Inuit aged 15 and over in Nunavut reported that speaking and understanding Inuktut was very important to them.

In Nunavut, 90% of Inuit children aged 6 to 14 have been taught Inuktut at school.

In 2022, among Indigenous children aged 1 to 5 years, 49.3% of First Nations children living off reserve, 55.9% of Métis children and 36.2% of Inuit children were in child care. Among those in child care, roughly 6 in 10 First Nations and Métis children and 1 in 2 Inuit children were in centre-based child care as their main child care arrangement, and lower shares were in Indigenous-specific child care.

Among parents of Indigenous children in child care, 48.6% of parents of First Nations children living off reserve, 29.8% of Métis children and 64.2%E of Inuit children reported that their care arrangement provided an environment that encouraged learning about Indigenous traditional and cultural values and customs.

Gross domestic income earned by Indigenous people increased in 2023

Gross domestic income (GDI), also known as income-based gross domestic product, earned by Indigenous people (Indigenous GDI) reached $63.7 billion in 2023, up 6.1% from 2022. Indigenous GDI as a share of total Canadian GDI increased from 2.0% in 2012 to 2.3% in 2023.

Gross domestic income rose in every province and territory in 2023

Continuing a trend that began in 2021, Indigenous GDI grew in every province and territory in 2023.

Yukon (+10.2%) and Nova Scotia (+9.9%) saw the largest growth in Indigenous GDI in 2023. In both regions, growth in the public administration sector was a significant contributor to the increase.

Provincial and territorial shares of total Indigenous GDI in Canada remained relatively stable in 2023. Ontario ($15.2 billion; 23.9%) continued to account for the largest share of total Indigenous GDI in Canada, while Prince Edward Island ($0.1 billion; 0.2%) accounted for the smallest.

In 2023, the share of total provincial GDI earned by Indigenous people ranged from 1.2% in Prince Edward Island to 7.7% in Manitoba. In the territories, where Indigenous people make up a larger share of the population, Nunavut (27.6%) had the largest share of GDI attributable to Indigenous people, while Yukon (13.4%) had the smallest.

In 2023, jobs held by Indigenous people grew by 2.9% to reach nearly 918,000, representing 4.4% of all jobs in Canada.

The construction (+5,580 jobs) and health care and social assistance (+4,505 jobs) sectors contributed the most to the growth in jobs held by Indigenous people in 2023. Combined, these two sectors accounted for nearly one in four jobs held by Indigenous people (23.6%). Among sectors, utilities (+9.4%) and arts, entertainment and recreation (+8.6%) had the highest rates of growth. However, these sectors represent only 2.6% of jobs held by Indigenous people.

Higher representation and income for Indigenous employees in Indigenous-owned businesses

Across all sectors, regions and firm sizes, Indigenous-owned businesses employ a much higher share of Indigenous workers than non-Indigenous-owned businesses. For example, in the construction sector, Indigenous employees represented 24.8% of workers in Indigenous-owned businesses in 2022, compared with 4.3% in non-Indigenous-owned businesses.

In the manufacturing sector, Indigenous employees represented 16.0% of workers in Indigenous-owned businesses compared with 2.6% of those in non-Indigenous-owned businesses.

Indigenous employees also earned more in Indigenous-owned businesses in nearly every sector, with income gaps exceeding 25% in 8 of the 13 sectors.

CVs for Operating Revenue - 2022

Table summary

This table displays the results of CVs for Operating Revenue. The information is grouped by geography (appearing as row headers), percent, Lessors of residential buildings and dwellings (except social housing projects), Non-residential leasing and Real estate property managers (appearing as column headers).

Geography

CVs for operating revenue

percent

Lessors of residential buildings and dwellings (except social housing projects)

The NetSupport software is required for our organization to be able to provide an effective Quality Control Monitoring Program. It will enable supervisors to provide comprehensive feedback to data collection clerks on core competencies in areas that cannot otherwise be addressed via auditory observation alone. This assessment illustrates that the risks involved with using NetSupport are far outweighed by the crucial function it provides. The application is essential for providing the necessary training, support and coaching data collection clerks need to meet our high standards for data quality control.

Objective

A privacy impact assessment was conducted to determine if there were any privacy, confidentiality and security issues associated with using NetSupport for the Quality Control Monitoring Program, and if so, to make recommendations for their resolution or mitigation.

Description

Statistics Canada has a legislative mandate under the Statistics Act to collect survey information from respondents on various topics. To fulfill this mandate, the agency is responsible for the objectives of maintaining high standards for quality control and conducting effective performance management of employees. The current Quality Control Monitoring Program was established in the regional offices in pursuit of achieving these objectives, however the program is rendered ineffective by the absence of visual observation for telephone interviews.

The NetSupport software is a third-party application that will address the need to have visual observation during monitoring sessions of telephone interviews. For our usage, the application will allow a set of users (i.e., Data Collection Supervisors) to conduct visual observation of other users' desktop screens (i.e., data collection clerks) for the sole purpose of performance management and quality control. The software will enable supervisors to evaluate in real-time the data collection clerk's skills, ensure data quality and identify areas for improvement in the interviewing process. As a result, the quality and level of detail supervisors can provide to data collection clerks for their performance feedback is greatly enhanced. At no point will the information viewed via NetSupport be recorded, collected or saved by the software.

For privacy impacts related to NetSupport, measures are in place to ensure that the impacted parties are informed. Data collection clerks are made aware of the possibility of being observed via their collective agreement, the training they receive and the interview script they read. Respondents of Statistics Canada surveys are made aware of monitoring at the beginning of the interview via the standard statement in our survey scripts that indicates a supervisor may listen to the call for quality control purposes.

Although NetSupport will not be saving/recording information, users of the software will have access to view the respondent's personal information while it is visible on the data collection clerks' screen. This may contain personally identifiable information such as names, addresses, ages, and other demographical information, as well as responses to our survey questions. Given the confidential nature of this information, the use of NetSupport will be restricted to supervisors and managers who have taken the Oath of Secrecy. These employees receive training on how to handle and protect confidential information that is subject to the Privacy Act and the Statistics Act.

Our organization is taking the necessary precautions to limit the number of risks involved with using NetSupport for respondents and employees. For example, the use of NetSupport will be limited to observing work-related performance only and for limited durations (e.g., 20 minutes). The user settings for NetSupport will also be restricted so that features that go beyond the purposes of monitoring performance will be disabled (e.g., recording of audio or video) to ensure it meets our security procedures. Furthermore, permissions for user accounts will be standardized and aligned with internal security procedures.

Risk Area Identification and Categorization

The PIA identifies the level of potential risk (level 1 is the lowest level of potential risk and level 4 is the highest) associated with the following risk areas:

a) Type of program or activity

Risk scale

Administration of program or activity and services

2

b) Type of personal information involved and context

Only personal information, with no contextual sensitivities, collected directly from the individual or provided with the consent of the individual for disclosure under an authorized program.

1

c) Program or activity partners and private sector involvement

Within the institution (among one or more programs within the same institution)

1

d) Duration of the program or activity

Long-term program or activity.

3

e) Program population

The program's use of personal information for internal administrative purposes affects certain employees.

1

f) Personal information transmission

The personal information is used in a system that has connections to at least one other system.

2

g) Technology and privacy