Total environmental taxes generated in Canada rose 7.8% year over year to $33.3 billion in 2022. The increase in total environmental taxes was attributable to higher energy taxes (+6.6%), which was driven by a growth in the carbon tax (+21.6%) from 2021 to 2022.

Environmental taxes are applied to products and on production processes to encourage consumers and producers to adopt more environmentally sustainable behaviours. To help reduce greenhouse gas emissions, the Government of Canada introduced the federal carbon tax in 2019, through the Greenhouse Gas Pollution Pricing Act. The federal carbon tax on fossil fuels—which is paid by fuel producers and distributors—increased from $40 per tonne in 2021 to $50 per tonne in 2022.

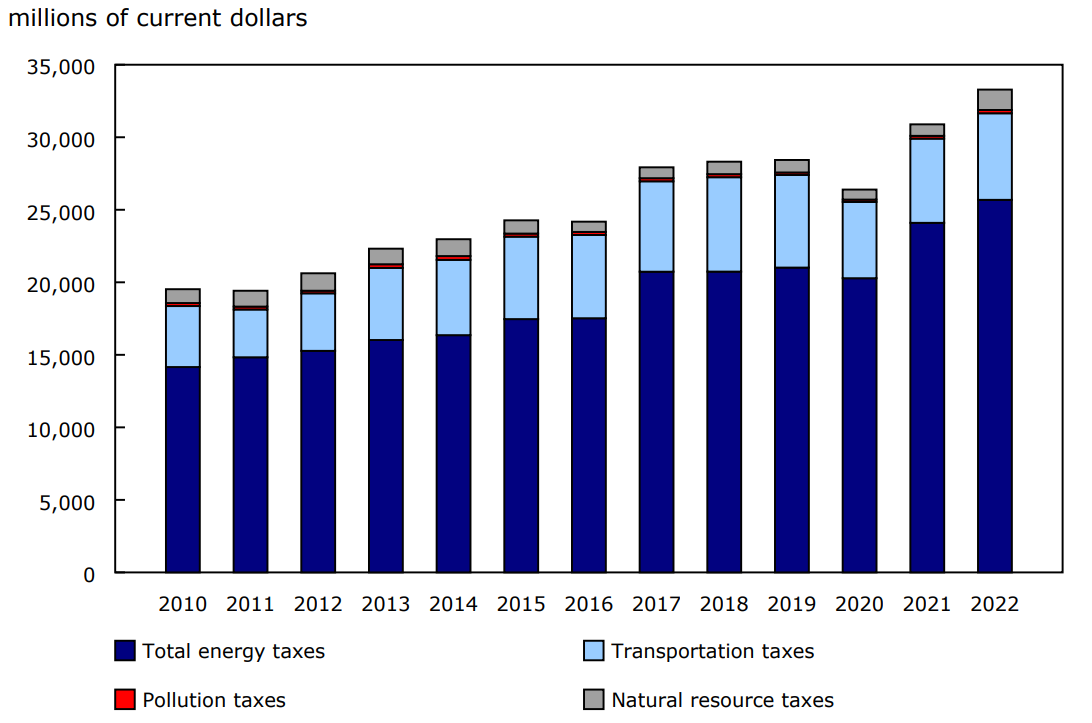

Chart 1: Composition of environmental taxes collected in Canada, by tax type

Description - Chart 1

Data table: Composition of environmental taxes collected in Canada, by tax type

Notes: Total energy taxes include taxes on energy and fuel for transport, carbon tax, and emission trading permits. The data series begins in 2010.

Source: Table 36-10-0678-01.

Energy taxes account for over three-quarters of environmental tax revenue

Energy taxes accounted for over three-quarters (77.2% in 2022) of total environmental taxes for the third consecutive year. The share of environmental taxes attributable to transportation taxes edged down 0.9 percentage points to 17.9%, while the share of natural resource taxes (+4.2%) and pollution taxes (+0.7%) increased from 2021 to 2022.

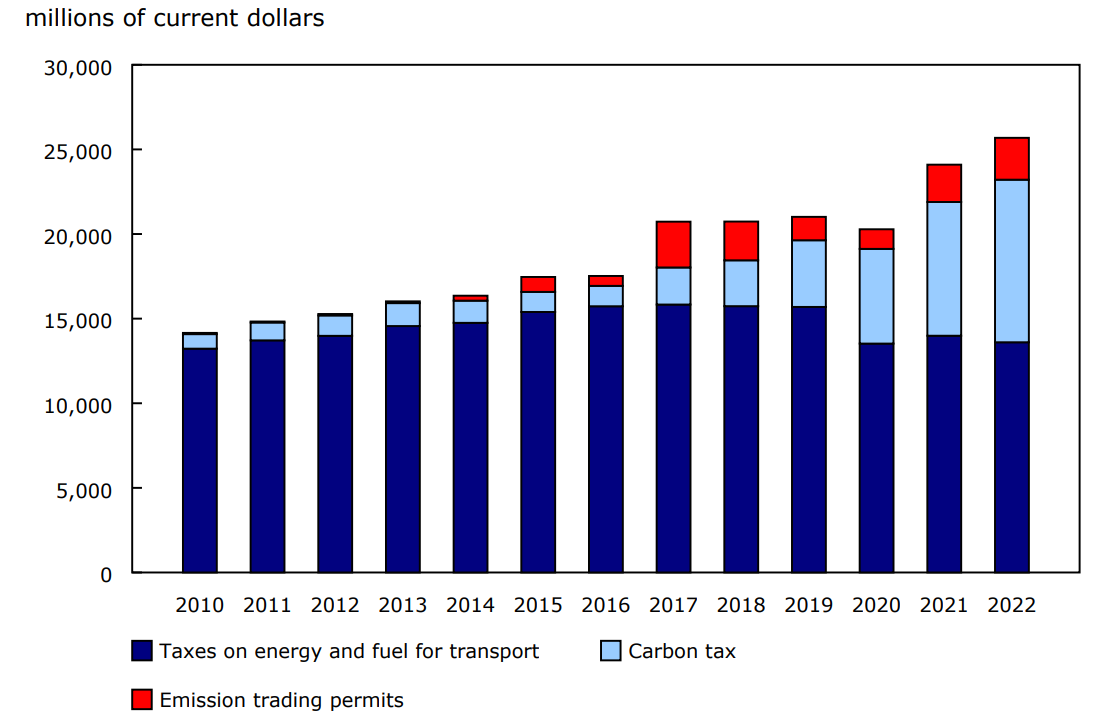

Within the energy tax category, the share of the carbon tax increased from 32.8% in 2021 to 37.4% in 2022, while the share of energy and fuel for transport decreased from 58.1% to 53.0%.

Chart 2: Composition of energy tax revenue in Canada

Description - Chart 2

Data table: Composition of energy tax revenue in Canada

Note: The data series begins in 2010.

Source: Table 36-10-0678-01.

The industry sector accounts for the largest share of environmental taxes, led by the truck transportation industry

The majority of environmental tax revenue in 2022 came from the industry sector, representing 57.0% ($19.0 billion) of all environmental taxes. Households followed, at 42.5% ($14.2 billion) of all environmental taxes paid, down 0.9 percentage points from 2021.

Within the industry sector, the truck transportation industry (17.9%) had the largest share of environmental taxes in 2022, followed by wholesale trade (3.7%) and electric power generation, transmission and distribution (2.9%).

Out of all the environmental taxes paid by the truck transportation industry, the share of taxes on energy and fuel for transport decreased from 63.5% in 2021 to 58.4% in 2022, while the share of the carbon tax increased from 36.3% to 41.4%.

Saskatchewan sees the largest growth in environmental taxes

Environmental taxes in Saskatchewan grew by 36.3% to $2.6 billion in 2022. This growth was partly attributable to natural resources tax revenue, which more than doubled from $454.5 million in 2021 to $969.5 million in 2022. This increase was partly due to higher hunting and fishing license fees.

Note to readers

The Environmental tax statistics (ETS) provides annual estimates of environmental taxes in current dollars at the national level and by province and territory for the 2022 reference year.

The ETS measures the revenue received by governments from environmental taxes paid by the industry sector (industries, government institutions and non-profit organizations) and households, as well as through gross fixed capital formation.

This product records transfers from businesses and households to governments and does not record any returns, such as the carbon tax rebate that is received by households in some provinces.

Environmental tax amounts are reported for four main categories: energy taxes, transportation taxes, pollution taxes and natural resource taxes. Energy taxes can also be broken down into three subcategories: taxes on energy and fuel for transport, the carbon tax, and emission trading permits.

The carbon tax is a tax charge placed on greenhouse gas emissions released mainly from burning fossil fuels. Taxes on greenhouse gas emissions other than carbon dioxide are also included. The household portion of the federal fuel charge was eliminated in April 2025. This change will be reflected in the data (under the carbon tax category) for the 2025 reference year.

This product records revenue captured, under the Greenhouse Gas Pollution Pricing Act, through the federal carbon pollution pricing system, which consists of two main parts: the fuel charge and the Output-Based Pricing System.

Emission trading permits enable government revenue to be recorded from the auctioning of emission permits (also known as "cap and trade"), which are treated as taxes on production in the national accounts.

Development of this product follows the United Nations System of Environmental-Economic Accounting 2012—Central Framework. For more information, see the page Canadian System of Environmental-Economic Accounts—Environmental tax statistics (ETS).

Results for the ETS are in line with Statistics Canada's environmental taxes submission to the International Monetary Fund. Discrepancies arise mainly from presenting the ETS estimates by calendar year rather than by fiscal year.

Definition

Environmental taxes: For the purpose of this product, environmentally related taxes are those in which the tax base is a physical unit (or a proxy of it) of something that has a proven, specific, negative impact on the environment (as per the United Nations definition).

Contact information

For more information, or to enquire about the concepts, methods or data quality of this release, contact us (toll-free 1-800-263-1136; 514-283-8300; infostats@statcan.gc.ca) or Media Relations (statcan.mediahotline-ligneinfomedias.statcan@statcan.gc.ca).