On behalf of the Canadian Industry Partnership for Energy Conservation (CIPEC), I would like to thank you for responding to the 2023 Industrial Consumption of Energy (ICE) survey.

Energy efficiency plays a key role in Canada's efforts to reduce energy use and GHG emissions, while strengthening competitiveness and maximizing profits. Your participation in the ICE survey enables us to track industry's progress and help meet Canada's Pan-Canadian Framework objectives of clean growth and a low carbon economy. Specifically, the ICE data is used to help build the business case for funding and program renewals, monitor sector progress and celebrate industry's energy achievements.

Natural Resources Canada (NRCan) currently supports industrial organizations in improving their energy performance through program activities such as:

Energy management frameworks and cost-shared financial assistance;

Tools, guides and technical information; and

National and international networks.

In fact, as noted in the Government of Canada Budget 2022, the federal government proposed to provide $194 million over five years to NRCan to expand our current Industrial Energy Management Program. This could include support for ISO 50001 certification, energy managers, cohort-based training, audits, and energy efficiency-focused retrofits for key small-to-moderate projects that fill a gap in the federal suite of industrial programming.

We are currently designing the program with preliminary discussions with key stakeholders and anticipate providing more details on programming later this year.

NRCan also administers the ENERGY STAR for Industry program, which offers the ENERGY STAR Challenge to help reduce facility energy intensity by 10% within 5 years, and tools to measure, track and benchmark energy to reduce waste and save money for companies eligible through ENERGY STAR Certification.

NRCan and CIPEC can help you produce results and save costs. Contact us today to learn more about how we can support your organization in improving your energy performance.

Thank you again for your participation.

Sincerely,

Eric Gingras

Manager, Outreach and Engagement

Industrial Division, Natural Resources Canada

The Canadian international merchandise trade program

Introduction

The objective of this text is to provide a general overview of the balance of payments-basis data produced by the Canadian International Merchandise Trade (CIMT) Program, with special reference to concepts and definitions.

Conceptual framework

1. Objectives and coverage: The objective of balance of payments-basis CIMT statistics is to measure the change in economic transactions that involve merchandise trade between residents and non-residents. Information on imports and exports are inputs into the Macroeconomic Accounts, and are used in the formulation of trade and economic policies. Governments, importers, exporters, manufacturers and shipping companies use international merchandise trade statistics to:

monitor import penetration and export performance;

monitor commodity price and volume changes; and

examine transport implications.

2. Trade statistics (customs-basis/balance of payments-basis): Merchandise trade statistics are presented on two different bases: customs and balance of payments.

Statistics for Canada’s imports as well as exports to non-US destinations are compiled from Customs declarations filed with the Canada Border Services Agency (CBSA). Data for Canada’s exports to the United States are derived from the administrative import records of the United States Customs and Border Protection and exchanged under the terms of a memorandum of understanding between Canada and the United States. Statistics developed from these Customs administrative records are commonly referred to as customs-basis trade statistics.

Customs-basis data are adjusted to conform to the National Accounts concepts and definitions. The adjustments to derive balance of payments-basis trade data include adjustments related to trade definition, valuation and timing. The principal difference between the two trade concepts is that customs-basis merchandise trade statistics cover the physical movement of goods as they are reflected in Customs documents while balance of payments-basis data are intended to cover economic transactions that involve merchandise trade between residents and non-residents.

In addition, customs-basis export statistics may understate or incorrectly portray the destination of exports. Exports are incorrectly portrayed when the country of final destination is inaccurately reported on the Customs documentation. This occurs most frequently when goods are routed through an intermediary country before continuing on to their final destination. Statistics Canada does not have a direct measure of undercoverage, therefore a monthly estimated adjustment is included within balance of payments-basis data.

3. Valuation: For Customs purposes, imports are recorded at values established according to the provisions of the Customs Act, which reflects valuation methods based on the General Agreement on Tariffs and Trade (GATT) Valuation Code System. In general, the value for duty of imported goods must be equivalent to the transaction value or the price actually paid.

The transaction value of imported goods includes all transportation and associated costs incurred up to the point of direct shipment to Canada. Therefore, Canada's imports are valued Free on Board (FOB), place of direct shipment to Canada. It excludes freight and insurance costs in bringing the goods to Canada from the point of direct shipment.

Exports are recorded at the value declared on Customs documents, which reflect the transaction value (i.e., actual selling price or, in the case of a non-arm's length transaction, the transfer price used for company accounting purposes). Canada's exports are valued at FOB port of exit from Canada, including domestic freight charges to that point but net of discounts and allowances.

4. Statistical period: In theory, the statistical period for balance of payments-basis trade statistics reflects the month during which change of ownership occurred. Since this can be difficult to determine, in practice, the statistical period for balance of payments-basis statistics reflects the month during which the goods cleared Customs. The closing of the statistical month for imports and exports is defined as the last calendar day of the month based on the date of clearance from Customs. Documents received too late for incorporation in the current month are assigned to the month the transaction took place and are published the following statistical month.

5. Trading partner attribution (country of origin/destination): On a custom basis, imports are attributed to the country of origin, that is the country in which the goods were grown, extracted or manufactured in accordance with the rules of origin administered by the CBSA. On a balance of payments-basis, imports are attributed to the country of export instead of the country of origin to reflect the change in ownership of the goods.

Both customs- and balance of payments-basis exports are attributed to the country that is the last known destination of the goods at the time of export.

6. Principal Trading Partners (PTPs): The list of PTPs is based on their annual share of total trade — merchandise imports plus exports — with Canada in 2012. The countries included in the list of PTPs are the following:

List of Canada's Principal Trading Partners

United States

European Union

Germany

Netherlands

France

Italy

Belgium

Spain

China

United Kingdom

Mexico

Japan

South Korea

Hong Kong

Brazil

Algeria

Norway

India

Switzerland

Saudi Arabia

Turkey

Taiwan

Peru

Australia

Iraq

Indonesia

Singapore

Russian Federation

Other OECD countries

All other countries

7. Legal framework: Import and export statistics with countries other than the United States are derived from information contained in administrative records collected by the CBSA under the Customs Act. Copies of these documents (or information therefrom) are sent to Statistics Canada in accordance with Section 25 of the Statistics Act. It follows that the disclosure of trade statistics is governed by both the Customs Act and the Statistics Act and is subject to the provisions of Section 17(2)(a) of the latter. Disclosure of statistics for trade with the United States is governed by a memorandum of understanding that provides for the exchange of detailed import statistics between Canada and the United States.

National Travel Survey: C.V.s for Visit-Expenditures by Duration of Visit, Main Trip Purpose and Country or Region of Expenditures, including expenditures at origin and those for air commercial transportation in Canada, in Thousands of Dollars (x 1,000)

Table summary

This table displays the results of C.V.s for Visit-Expenditures by Duration of Visit, Main Trip Purpose and Country or Region of Expenditures. The information is grouped by Duration of trip (appearing as row headers), Main Trip Purpose, Country or Region of Expenditures (Total, Canada, United States, Overseas) calculated using Visit-Expenditures in Thousands of Dollars (x 1,000) and c.v. as units of measure (appearing as column headers).

Duration of Visit

Main Trip Purpose

Country or Region of Expenditures

Total

Canada

United States

Overseas

$ '000

C.V.

$ '000

C.V.

$ '000

C.V.

$ '000

C.V.

Total Duration

Total Main Trip Purpose

29,516,569

A

17,667,891

A

7,025,194

B

4,823,483

A

Holiday, leisure or recreation

15,338,989

A

7,104,480

A

4,719,656

B

3,514,853

B

Visit friends or relatives

6,884,454

B

5,223,439

B

778,085

C

882,930

C

Personal conference, convention or trade show

376,755

C

295,838

C

62,360

D

18,557

E

Shopping, non-routine

1,116,452

B

910,278

B

206,173

C

..

Other personal reasons

1,533,226

B

1,296,436

B

156,143

E

80,648

E

Business conference, convention or trade show

2,073,216

B

1,163,162

C

702,405

C

207,648

D

Other business

2,193,476

C

1,674,258

C

400,371

E

118,847

E

Same-Day

Total Main Trip Purpose

6,363,851

B

5,876,598

B

445,198

C

42,054

E

Holiday, leisure or recreation

2,561,458

B

2,314,743

B

205,676

C

41,039

E

Visit friends or relatives

1,600,206

B

1,578,375

B

20,816

D

1,015

E

Personal conference, convention or trade show

90,914

D

85,485

D

5,430

E

..

Shopping, non-routine

932,121

B

781,764

C

150,357

D

..

Other personal reasons

661,385

B

648,003

B

13,382

D

..

Business conference, convention or trade show

123,972

E

79,123

C

44,849

E

..

Other business

393,795

C

389,106

C

4,689

E

..

Overnight

Total Main Trip Purpose

23,152,718

A

11,791,293

A

6,579,996

B

4,781,429

A

Holiday, leisure or recreation

12,777,531

A

4,789,737

B

4,513,980

B

3,473,814

B

Visit friends or relatives

5,284,248

B

3,645,064

B

757,270

C

881,915

C

Personal conference, convention or trade show

285,841

C

210,354

C

56,930

E

18,557

E

Shopping, non-routine

184,331

D

128,514

D

55,816

E

..

Other personal reasons

871,842

B

648,432

C

142,761

E

80,648

E

Business conference, convention or trade show

1,949,244

B

1,084,040

C

657,556

C

207,648

D

Other business

1,799,681

C

1,285,152

C

395,682

E

118,847

E

..

data not available

Estimates contained in this table have been assigned a letter to indicate their coefficient of variation (c.v.) (expressed as a percentage). The letter grades represent the following coefficients of variation:

A

c.v. between or equal to 0.00% and 5.00% and means Excellent.

B

c.v. between or equal to 5.01% and 15.00% and means Very good.

C

c.v. between or equal to 15.01% and 25.00% and means Good.

D

c.v. between or equal to 25.01% and 35.00% and means Acceptable.

E

c.v. greater than 35.00% and means Use with caution.

National Travel Survey: Response Rate - Q2 2023

Table summary

This table displays the results of Response Rate. The information is grouped by Province of residence (appearing as row headers), Unweighted and Weighted (appearing as column headers), calculated using percentage unit of measure (appearing as column headers).

National Travel Survey: C.V.s for Person-Trips by Duration of Trip, Main Trip Purpose and Country or Region of Trip Destination, Q2 2023

Table summary

This table displays the results of C.V.s for Person-Trips by Duration of Trip, Main Trip Purpose and Country or Region of Trip Destination. The information is grouped by Duration of trip (appearing as row headers), Main Trip Purpose, Country or Region of Trip Destination (Total, Canada, United States, Overseas) calculated using Person-Trips in Thousands (× 1,000) and C.V. as a units of measure (appearing as column headers).

Duration of Trip

Main Trip Purpose

Country or Region of Trip Destination

Total

Canada

United States

Overseas

Person-Trips (x 1,000)

C.V.

Person-Trips (x 1,000)

C.V.

Person-Trips (x 1,000)

C.V.

Person-Trips (x 1,000)

C.V.

Total Duration

Total Main Trip Purpose

78,269

A

70,155

A

6,147

A

1,968

A

Holiday, leisure or recreation

30,491

A

25,809

A

3,331

B

1,351

A

Visit friends or relatives

28,591

A

27,099

A

1,039

B

453

B

Personal conference, convention or trade show

1,395

E

1,217

E

172

D

6

E

Shopping, non-routine

4,918

B

4,234

B

683

C

..

Other personal reasons

6,088

B

5,818

B

232

C

38

E

Business conference, convention or trade show

1,995

B

1,531

B

383

C

80

D

Other business

4,791

B

4,446

B

306

E

40

D

Same-Day

Total Main Trip Purpose

49,682

A

47,413

A

2,269

B

..

Holiday, leisure or recreation

17,376

B

16,320

B

1,056

B

..

Visit friends or relatives

17,982

B

17,724

B

258

E

..

Personal conference, convention or trade show

872

E

836

E

36

E

..

Shopping, non-routine

4,585

B

3,943

B

642

C

..

Other personal reasons

4,833

B

4,686

B

147

D

..

Business conference, convention or trade show

641

C

613

C

28

E

..

Other business

3,393

B

3,291

B

102

E

..

Overnight

Total Main Trip Purpose

28,588

A

22,742

A

3,878

A

1,968

A

Holiday, leisure or recreation

13,115

A

9,489

A

2,276

B

1,351

A

Visit friends or relatives

10,609

A

9,376

A

781

B

453

B

Personal conference, convention or trade show

523

C

381

C

136

E

6

E

Shopping, non-routine

333

D

291

D

41

E

..

Other personal reasons

1,255

B

1,132

B

85

D

38

E

Business conference, convention or trade show

1,354

B

918

B

355

C

80

D

Other business

1,399

B

1,155

B

204

D

40

D

..

data not available

Estimates contained in this table have been assigned a letter to indicate their coefficient of variation (c.v.) (expressed as a percentage). The letter grades represent the following coefficients of variation:

A

c.v. between or equal to 0.00% and 5.00% and means Excellent.

B

c.v. between or equal to 5.01% and 15.00% and means Very good.

C

c.v. between or equal to 15.01% and 25.00% and means Good.

D

c.v. between or equal to 25.01% and 35.00% and means Acceptable.

E

c.v. greater than 35.00% and means Use with caution.

Statement outlining results, risks and significant changes in operations, personnel and program

A) Introduction

Statistics Canada's mandate

Statistics Canada ("the agency") is a member of the Innovation, Science and Industry portfolio.

Statistics Canada's role is to ensure that Canadians have access to a trusted source of statistics on Canada that meets their highest priority needs.

The agency's mandate derives primarily from the Statistics Act. The Act requires that the agency collects, compiles, analyzes and publishes statistical information on the economic, social, and general conditions of the country and its people. It also requires that Statistics Canada conduct the census of population and the census of agriculture every fifth year and protects the confidentiality of the information with which it is entrusted.

Statistics Canada also has a mandate to co-ordinate and lead the national statistical system. The agency is considered a leader, among statistical agencies around the world, in co–ordinating statistical activities to reduce duplication and reporting burden.

has been prepared by management, as required by Section 65.1 of the Financial Administration Act, and in the form and manner prescribed by Treasury Board of Canada Secretariat;

has not been subject to an external audit or review.

Statistics Canada has the authority to collect and spend revenue from other federal government departments and agencies, as well as from external clients, for statistical services and products.

Basis of presentation

This quarterly report has been prepared by management using an expenditure basis of accounting. The accompanying Statement of Authorities includes the agency’s spending authorities granted by Parliament and those used by the agency consistent with the Main Estimates for the 2023-2024 fiscal year. This quarterly report has been prepared using a special purpose financial reporting framework designed to meet financial information needs with respect to the use of spending authorities.

The authority of Parliament is required before moneys can be spent by the Government. Approvals are given in the form of annually approved limits through appropriation acts or through legislation in the form of statutory spending authority for specific purposes.

The agency uses the full accrual method of accounting to prepare and present its annual departmental financial statements that are part of the departmental results reporting process. However, the spending authorities voted by Parliament remain on an expenditure basis.

B) Highlights of fiscal quarter and fiscal year-to-date results

This section highlights the significant items that contributed to the net increase in resources available for the year, as well as actual expenditures for the quarter ended September 30.

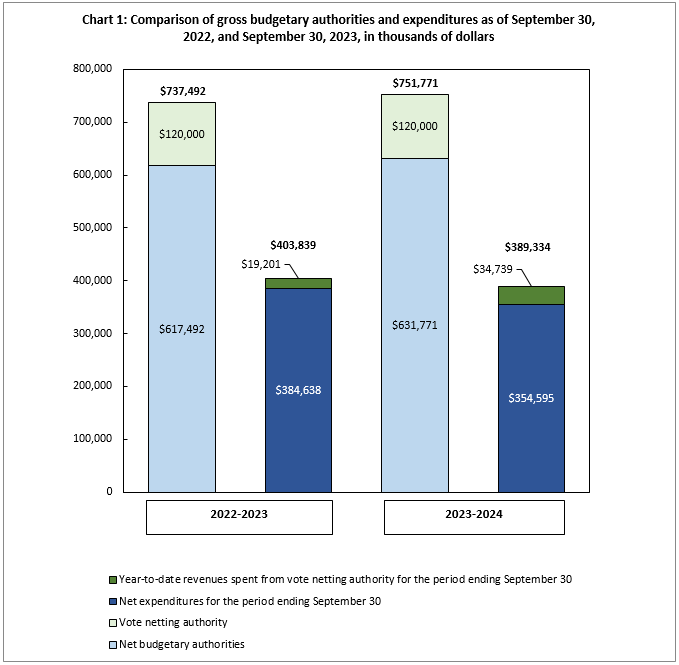

Description for Chart 1: Comparison of gross budgetary authorities and expenditures as of September 30, 2022, and September 30, 2023, in thousands of dollars

This bar graph shows Statistics Canada's budgetary authorities and expenditures, in thousands of dollars, as of September 30, 2022 and 2023:

As at September 30, 2022

Net budgetary authorities: $617,492

Vote netting authority: $120,000

Total authority: $737,492

Net expenditures for the period ending September 30: $384,638

Year-to-date revenues spent from vote netting authority for the period ending September 30: $19,201

Total expenditures: $403,839

As at September 30, 2023

Net budgetary authorities: $631,771

Vote netting authority: $120,000

Total authority: $751,771

Net expenditures for the period ending September 30: $354,595

Year-to-date revenues spent from vote netting authority for the period ending September 30: $34,739

Total expenditures: $389,334

Chart 1 outlines the gross budgetary authorities, which represent the resources available for use for the year as of September 30.

Significant changes to authorities

Total authorities available for 2023-24 have increased by $14.3 million, or 1.9%, from the previous year, from $737.5 million to $751.8 million (Chart 1). The net increase is mostly the result of the following:

An increase of $87.7 million for funding received to cover the initial planning phase and development activities related to the 2026 Census of Population and 2026 Census of Agriculture programs;

A decrease of $50.3 million for the 2021 Census of Population and 2021 Census of Agriculture programs due to cyclical nature of funding winding down;

A decrease of $28.9 million for the carry forward from the previous year. The agency leverages the operating budget carry-forward mechanism to manage the cyclical nature of program operations and investments in the agency’s strategic plan;

An increase of $1.3 million for salary increases related to the latest rounds of collective bargaining;

An increase of $17.1 million for various initiatives including Statistical Survey Operations Modernization, Dental Care for Canadians, Removing Barriers to Internal Trade, Building a World-Class Intellectual Property Regime and Taking More Action to Eliminate Plastic Waste;

A decrease of $12.2 million for various initiatives including Better Data for Better Outcomes, Strengthening Long-term Care and Supportive Care, Survey on the Official Language Minority Population, Supporting Access to Sexual and Reproductive Health Care Information and Services and Vision for a data-driven economy & society.

In addition to the appropriations allocated to the agency through the Main Estimates, Statistics Canada also has vote net authority within Vote 1, which entitles the agency to spend revenues collected from other federal government departments, agencies, and external clients to provide statistical services. The vote netting authority is stable at $120 million when comparing the second quarter of fiscal years 2022-2023 and 2023-2024.

Significant changes to expenditures

Year-to-date net expenditures recorded to the end of the second quarter decreased by $30 million, or 7.8% from the previous year, from $384.6 million to $354.6 million (see Table A: Variation in Departmental Expenditures by Standard Object).

Statistics Canada spent approximately 56.1% of its authorities by the end of the second quarter, compared with 62.3% in the same quarter of 2022-2023.

Table A: Variation in Departmental Expenditures by Standard Object (unaudited) This table displays the variance of departmental expenditures by standard object between fiscal 2022-2023 and 2023-2024. The variance is calculated for year to date expenditures as at the end of the second quarter. The row headers provide information by standard object. The column headers provide information in thousands of dollars and percentage variance for the year to date variation.

Departmental Expenditures Variation by Standard Object:

Q2 year-to-date variation between fiscal year

2022-2023 and 2023-2024

$'000

%

(01) Personnel

-12,098

-3.4

(02) Transportation and communications

418

5.7

(03) Information

-6

-0.2

(04) Professional and special services

884

4.6

(05) Rentals

-1,270

-8.5

(06) Repair and maintenance

-105

-39.6

(07) Utilities, materials and supplies

-101

-26.8

(08) Acquisition of land, buildings and works

8

-

(09) Acquisition of machinery and equipment

-1,654

-71.7

(10) Transfer payments

-

-

(12) Other subsidies and payments

-582

-45.1

Total gross budgetary expenditures

-14,506

-3.6

Less revenues netted against expenditures:

Revenues

15,538

80.9

Total net budgetary expenditures

-30,044

-7.8

Note: Explanations are provided for variances of more than $1 million.

Personnel: The decrease is mainly due to spendings for seasonal, casual, and student salaries, offset by salary price increases from the ratification of collective agreements.

Rentals: The decrease is mainly due to a one-time invoice for a software licence paid in the first quarter of 2022-2023.

Acquisition of machinery and equipment: The decrease is mainly due to the purchase of computers in the first quarter of 2022-2023.

Revenues: The increase is mainly due to a timing difference in invoicing compared to last year.

C) Significant changes to operations, personnel and programs

In 2023-24, the following changes in operations, personnel and program activities are underway:

The Census program is ramping down operations from the 2021 cycle and is in the planning phase for the 2026 Censuses of Population and Agriculture programs.

Budget 2023 announced funding for new initiatives, such as, the Canadian Dental Care program and the Official Languages Action Plan.

Budget 2023 announced a commitment to refocus government spending:

Budget 2023 proposes to reduce spending on consulting, other professional services, and travel by roughly 15 per cent starting in 2023-24. The government will focus on targeting these reductions on professional services, particularly management consulting.

Budget 2023 proposes to phase in a roughly 3 per cent reduction of eligible spending by departments and agencies by 2026-27.

Statistics Canada is committed to effective management of its programs and services. In anticipation of the announcement of pending reductions, Statistics Canada launched a review in 2022 to identify efficiencies and reductions to programs or services.

D) Risks and uncertainties

Statistics Canada is addressing the issues and corresponding uncertainties raised in this Quarterly Financial Report through ongoing monitoring activities on its corporate risks and mitigation measures captured in the 2023-24 Corporate Risk Profile and at the program level.

Statistics Canada continues to pursue and invest in modernizing business processes and tools to maintain its relevance and maximize the value it provides to Canadians. To address uncertainties, the agency is implementing the Census of Environment, the Quality of Life Framework for Canada, the Disaggregated Data Action Plan and several other initiatives focused on leveraging modern methods and recent investments in a modern infrastructure to meet the evolving needs of users and remain relevant as an agency. The agency is also remaining vigilant to cyber threats and continuously ensuring the security regarding handling and processing of its data while supporting the use of modern methods with a functional digital infrastructure.

Statistics Canada requires a skilled workforce to achieve its objectives; however, it is difficult to compete with other organizations in the data ecosystem and the current labour market situation. In addition, it is imperative to continue focusing on having an accessible, equitable and inclusive workforce. To address uncertainties, Statistics Canada will create partnerships with other government departments, international organizations, and IT Industry partners to find innovative ways to collaborate on bridging gaps in digital skills and IT human resource shortfalls. The agency will continue promoting a strong workplace culture, a healthy work-life balance, foster values and ethics and advance on the Equity, Diversity and Inclusion Action Plan. In addition, it will focus on existing employees and continue its effort to achieve greater diversity and inclusion across its workforce and promote and support accessibility through the Accessibility, Accommodation and Adaptive Computer Technology (AAACT) trainings, GC Accessibility Passport, and other resources on the StatCan Internal Communications Network (ICN).

Statistics Canada continues its collaboration with federal partners to access IT services and support to realize its modernization objectives and to achieve the agency’s priority to build and adopt a complete enabling infrastructure through the reduction of duplicative solutions, optimization of the Cloud infrastructure, automation of manual processes and shifting to open-source language. To address uncertainties, the agency is working closely with its federal partners, while adhering to the agency's notable financial planning management practices, integrated strategic planning framework as well as strengthening its financial stewardship.

Approval by senior officials

Approved by:

Anil Arora, Chief Statistician

Ottawa, Ontario

Signed on: November 20th, 2023

Kathleen Mitchell, Chief Financial Officer

Ottawa, Ontario

Signed on: November 14th, 2023

Appendix

Statement of Authorities (unaudited)

This table displays the departmental authorities for fiscal years 2022-2023 and 2023-2024. The row headers provide information by type of authority, Vote 105 – Net operating expenditures, Statutory authority and Total Budgetary authorities. The column headers provide information in thousands of dollars for Total available for use for the year ending March 31; used during the quarter ended September 30; and year to date used at quarter-end of both fiscal years.

Fiscal year 2023-2024

Fiscal year 2022–2023

Total available for use for the year ending March 31, 2024Table note *

Used during the quarter ended September 30, 2023

Year-to-date used at quarter-end

Total available for use for the year ending March 31, 2023Table note *

Used during the quarter ended September 30, 2022

Year-to-date used at quarter-end

in thousands of dollars

Vote 1 — Net operating expenditures

542,313

150,956

317,147

537,525

179,361

344,655

Statutory authority — Contribution to employee benefit plans

89,458

18,724

37,448

79,967

19,992

39,983

Total budgetary authorities

631,771

169,680

354,595

617,492

199,353

384,638

Table note *

Includes only Authorities available for use and granted by Parliament at quarter-end.

Departmental budgetary expenditures by Standard Object (unaudited)

This table displays the departmental authorities for fiscal years 2022-2023 and 2023-2024. The row headers provide information by type of authority, Vote 105 – Net operating expenditures, Statutory authority and Total Budgetary authorities. The column headers provide information in thousands of dollars for Total available for use for the year ending March 31; used during the quarter ended September 30; and year to date used at quarter-end of both fiscal years.

Fiscal year 2023-2024

Fiscal year 2022–2023

Planned expenditures for the year ending March 31, 2024

Expended during the quarter ended September 30, 2023

Year-to-date used at quarter-end

Planned expenditures for the year ending March 31, 2023

Expended during the quarter ended September 30, 2022

Supplementary information relating to the export of arms and ammunitions can be found on government websites such as Innovation, Science and Economic Development Canada's "Trade Data Online" and Statistics Canada's "Canadian International Merchandise Trade Web Application". These data are compiled and published based on the Harmonized System (HS) classification. This classification is overseen by the World Customs Organization for the purpose of establishing global commodity codes, with each product assigned a specific classification code. The HS codes support the compilation and uses of trade statistics.

The statistics for trade of commodities defined in Chapter 93 "Arms and ammunition; parts and accessories thereof" of the HS classification do not completely align with information for the export of conventional arms and ammunition as defined in the Export and Import Permits Act. As a result, the "Arms and Ammunitions" category of items does not in most cases reflect what is generally understood as conventional arms and ammunition. For example, goods such as flare guns used in oil and gas drilling, ammunition to frighten birds at airports, etc. may be listed under the "Arms and Ammunition" coding.

Other sources of information outside of Statistics Canada

Statistics relating to the export of military goods and technology, including conventional arms and ammunition, can be found in the reports on “Exports of Military Goods” published by Global Affairs Canada.

The Canadian Commercial Corporation also generates their own export data based on contracts between Canadian suppliers and military end-users. Again, these statistics may include items which are not strictly military in nature, such as storage containers.

The Canadian International Merchandise Trade (CIMT) Program of Statistics Canada produces monthly international merchandise trade values, price indices and volume indices on both a customs and balance of payments basis. These statistics are prepared under tight deadlines and depend primarily on large volumes of administrative records received from the Canadian Border Services Agency and the United States Customs and Border Protection Agency. In accordance with the agreement on the exchange of import data, Canadian and United States international merchandise trade data are released simultaneously by Statistics Canada and the United States Census Bureau approximately 35 days after the end of the reference month.

Factors influencing revisions include late receipt of Customs documentation, incorrect information on Customs forms, replacement of estimates with actual data, changes in classification of merchandise based on more current information, and changes to seasonal adjustment factors. In general, merchandise trade data are revised on an ongoing basis for each month of the current year.

Current year revisions are reflected in both the customs- and balance of payments-basis data. The previous year's customs-basis data are revised with the release of the January and February reference months as well as on a quarterly basis. The previous two years of customs-basis data are revised annually and are released in February with the December reference month. The previous year's balance of payments-basis data are revised with the release of the January, February, March and April reference months. Revisions to balance of payments-basis data for previous years are released annually in December with the October reference month.

Seasonal Adjustment

Seasonal adjustment of customs and balance of payments-basis values and price and volume indices is performed at an aggregated commodity grouping level of the North American Product Classification System (NAPCS). Customs and balance of payments-basis values are also seasonally adjusted at the principal trading partner level of geographical detail. Monthly fluctuations can occur as a result of weather patterns, number of trading days, roving holidays (such as Easter) and institutional factors, such as scheduled factory shutdowns. In order to isolate turning points or trends in the basic data, it is necessary to eliminate this effect of seasonal movement. To remove seasonal fluctuations from time series, Statistics Canada uses the SAS® X12 procedure (SAS Institute Inc., 2010) as well as an adaptation of the US Census Bureau X-12-ARIMA Seasonal Adjustment program (US Census Bureau, 2010). The seasonal adjustment process is applied following the Statistics Canada Quality Guidelines.

Revised data are available in the appropriate data tables and statistical products.

Reference

SAS Institute Inc. (2010), "The X12 Procedure", SAS 9.2 Documentation: SAS/ETS 9.22 User's Guide, Cary, NC: SAS Institute Inc.

US Census Bureau (2010), X-12-ARIMA Seasonal Adjustment Program, Version 0.3, Washington, DC.